For Big Banks, Lower Rates Could Mean the End of Profit Blowouts

For Big Banks, Lower Rates Could Mean the End of Profit Blowouts

(Bloomberg) -- Will the pain from lower interest rates match all the angst about bank earnings?

Investors will find out next week, when the biggest U.S. banks report second-quarter results. Falling interest rates have sparked concern that net interest income -- the money banks make from customers’ loan payments minus what they pay depositors -- will suffer. NII accounts for more than half of the biggest lenders’ revenue.

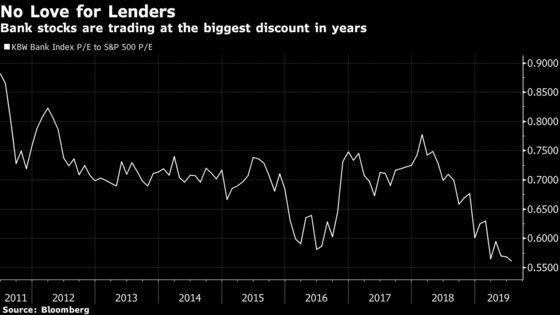

With long-term rates falling all year and a cut to the Federal Reserve’s benchmark likely this month, some investors in bank stocks aren’t waiting around to assess the fallout. Banks stocks have fallen in the past 12 months while most other industries gained, leaving them by one measure at the biggest discount to the broader market in more than a decade.

“There was a big drop in long-term rates, and that will have a big impact on revenues in the second quarter, with long-term effects,” Brian Kleinhanzl, an analyst at Keefe, Bruyette & Woods Inc., said in an interview.

Last quarter, Wells Fargo & Co. lowered its net-interest-income forecast for the full year to a decline, pushing the stock down. Bank of America Corp.’s shares also fell when it said NII would rise half as much as it did last year. Investors will be keen to see what happens to guidance when results get released.

Here’s what else to watch next week, when Citigroup Inc. kicks off earnings on Monday:

Capital Markets

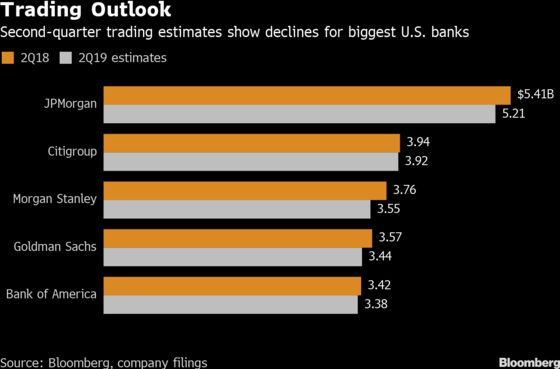

Executives across Wall Street have already warned of a trading drop in the second quarter on a challenging macro environment. Markets swung in the quarter on the changing interest-rate outlook, trade tensions and geopolitical events from Brexit to Iran.

Trading revenue for the industry is expected to show a drop of 3% for the second quarter, to $19.1 billion, based on estimates compiled by Bloomberg MODL. That’s a smaller decline than forecast by several banks in recent months, suggesting the final weeks of the quarter might have brightened for trading desks.

Analysts are expecting lower capital-markets results across the board in the second quarter. Investment-banking fees could be down 21% from a year earlier, Susan Katzke, an analyst at Credit Suisse Group AG, wrote in note earlier this month. Fees from initial public offerings and debt underwriting were probably the only bright spots, rising 7% and 4% respectively, according to Katzke.

Mortgages

One benefit of lower rates: more refinancing. Second-quarter applications to refinance home loans were up more than 40% from a year earlier to a level not seen since 2016, according to the Mortgage Bankers Association. Fee income from the mortgage business could help counter lower net interest income in the second quarter.

But the party may not last. “We’re at the point where we’re experiencing refi burnout,” Eli Salzmann, a portfolio manager for Neuberger Berman whose fund has stakes in JPMorgan Chase & Co. and Wells Fargo, said Wednesday on Bloomberg Television. “Many people who could refi already refied.”

Credit Quality

The current U.S. economic expansion just became the longest on record. Banks are benefiting from “conservative underwriting standards and a strong economy,” Gerard Cassidy, an analyst at RBC Capital Markets, wrote in a note at the end of June. Analysts expect credit quality to remain strong in the second quarter, but will be watching for any signs of a more challenging environment.

Three of the four largest lenders increased provisions in the first quarter to cover consumer-loan losses, with Wells Fargo more than tripling the amount it set aside. In Bank of America’s consumer unit, charge-offs climbed to $925 million, the highest since 2013. Credit losses at Citigroup’s giant credit-card business jumped 9% from a year earlier.

“We saw a lot of one-offs happen in the first quarter that the banks said were not geographic or sector-specific,” said Kleinhanzl at KBW. “We’ll watch to see if it repeats itself.”

Cost Guidance

Banks posted record earnings last year as they benefited from strong retail-banking results, more deals and tax cuts, all of which allowed them to spend more on investments. The tougher revenue environment and falling interest rates mean there’s a new emphasis on cutting expenses, Richard Ramsden, an analyst at Goldman Sachs Group Inc., wrote in a note this week.

To contact the reporters on this story: Hannah Levitt in New York at hlevitt@bloomberg.net;Elizabeth Rembert in New York at erembert@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Steve Dickson, Daniel Taub

©2019 Bloomberg L.P.