For Battered Junk Bond Market, an Old Risk Grows Louder Each Day

For Battered Junk Bond Market, an Old Risk Grows Louder Each Day

(Bloomberg) -- Investors have long been sounding the alarm: An unprecedented number of companies had loaded up on cheap debt that left them hanging, just barely, onto investment-grade credit ratings. A weak business cycle, they said, could push those companies into junk territory.

Now, that warning is moving closer than ever to reality. The double blow of a global pandemic and plunging oil prices is tipping the economy into recession. That is making the lowest tier of investment-grade companies vulnerable to downgrades to high-yield status -- a designation that could drive up their borrowing costs and set off a wave of selling from investors who aren’t permitted to hold such low-quality debt.

Most at risk are debt-laden companies highly exposed to the economy, such as Ford Motor Co., Petroleos Mexicanos and Occidental Petroleum Corp. In all, they hold roughly $868 billion of debt that is just one level above speculative grade, meaning they have at least one BBB- or equivalent rating.

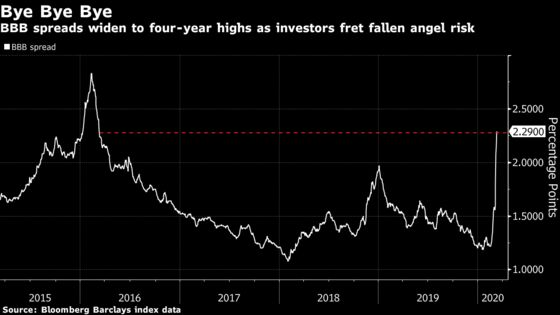

The wall of worry that hangs over BBB debt is helping to fuel an exodus from the corporate-bond market. A record $7.27 billion was yanked from investment-grade bond funds in the past week, on top of $4.8 billion pulled in the prior week.

Billions of dollars of fallen-angel debt pouring into the market is the last thing that junk bond investors need as they try to navigate what’s been three straight weeks of brutal losses. That additional supply would threaten to further depress prices and drive up junk yields that have soared to 7.26 percentage points over Treasuries. In mid-February, that gap was just 3.31 percentage points.

“There are a number of issuers priced for perfection,” said Jonathan Terry, an investment-grade portfolio manager at Wells Fargo Asset Management. “Any slippage in earnings is going to put them closer to that edge.”

That slippage is already taking place. The wobbly economy has prompted companies to draw on credit lines, cut profit outlooks, or withdraw forecasts entirely, as the disease threatens their supply chains, demand or both. It’s also rippled through credit markets, sparking selloffs reminiscent of when Lehman Brothers collapsed.

A drop in earnings will make debt that much more onerous, boosting leverage ratios to the point that credit raters may have to take action. While many companies can cut their dividend or sell assets to free up cash, not everyone has those options, and for those who do, it still may not be enough to stave off downgrades.

“There will be companies across industries where it’s too late for them,” said Tom Murphy, head of investment-grade credit at Columbia Threadneedle Investments.

Occidental, Ford

That’s not to say that all of the nearly $3 trillion worth of BBB debt will fall to high yield. For many investors and strategists, they’re squarely concerned with that $868 billion pile of debt sitting perilously in the lowest rung of investment grade.

Within that universe, companies like Occidental Petroleum are already feeling the pressure. The oil producer, which has recently seen some of its bonds trade at less than 70 cents on the dollar, cut its dividend for the first time in 30 years to conserve cash, yet analysts are still skeptical about its ability to reduce debt.

Ford, with one junk rating already, may get another sooner than expected as the virus hurts demand for cars, according to research firm CreditSights. Either company would instantly become the largest high-yield issuer if its debt left investment-grade indexes.

Several smaller issuers are at risk, too. S&P Global Ratings said it may cut Royal Caribbean Cruises Ltd. to junk amid increasing travel fears, and Moody’s Investors Service may downgrade it as well. The cost to protect debt of Macy’s Inc., which already has one high-yield rating, and Kohl’s Corp. hit record highs Thursday.

Some $270 billion of BBB debt already trades at speculative-grade levels, according to Bloomberg Intelligence. That’s roughly 9% of the entire rating tier. More than a third of all BBBs may fall to high yield, according to Credit Benchmark, while UBS Group AG strategists led by Matthew Mish say as much as $140 billion could cross over the line this year alone, largely due to the stress in energy.

‘Debt Diet’

Investors have been calling for this rude awakening for awhile. And, in fact, many companies took such warnings to heart and made 2019 the year of the “debt diet,” marked by some of the largest issuers, like AT&T Inc. and Verizon Communications Inc., getting their balance sheets in order.

But most companies don’t have enough cash on hand to absorb a decline in earnings, “implying job cuts may come faster and deeper than they have in previous economic downturns, excluding the financial crisis,” BMO strategist Daniel Belton said in a report Wednesday. Moreover, a big hit to corporate earnings will “awaken anxieties” even about those companies that are already in the process of deleveraging, said Citigroup Inc. strategist Daniel Sorid.

Some analysts are more sanguine, viewing today’s BBB market as less exposed to changes in the economy, said Dave Brown, head of global investment-grade credit at Neuberger Berman. Such industries as food and beverage, cable media, telecom and utilities tend to be fairly stable regardless of the economic backdrop, and arguably would be in higher demand if people are confined to their homes.

“We don’t expect there to be a large fallen-angel problem this year unless there is a change in growth in the economy,” Brown said on a podcast Wednesday, noting that he’s optimistic for a rebound in the second half of the year.

So far that’s true, with Kraft Heinz Co. the only material one to date. But the growth picture has changed, even if temporarily. That’s creating severe pricing distortions and blowing out the gap between bids to buy and offers to sell securities, making traders’ jobs that much more difficult.

“We’re having trouble finding buyers on the other side, and that’s the beginning of the concern,” said Kevin Giddis, chief fixed-income strategist at Raymond James. “The red flags are starting to go up as we grow concerned about credit in general.”

--With assistance from Olivia Raimonde and Adam Cataldo.

To contact the reporter on this story: Molly Smith in New York at msmith604@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Larry Reibstein, Boris Korby

©2020 Bloomberg L.P.