TV Lawyer, Ex-Israeli Commando Forge a $33 Billion SPAC Deal

Florida Lawyer, Ex-Paratrooper Forge a $33 Billion SPAC Deal

(Bloomberg) -- John H. Ruiz is on no one’s list of Wall Street big shots.

Over the years the Miami lawyer has hosted a Spanish language cable-TV show, owned a high school sport website and worked on class-action lawsuits. At one point, his luxury cigarette boat was repossessed, according to a published report — an episode Ruiz has called a misunderstanding.

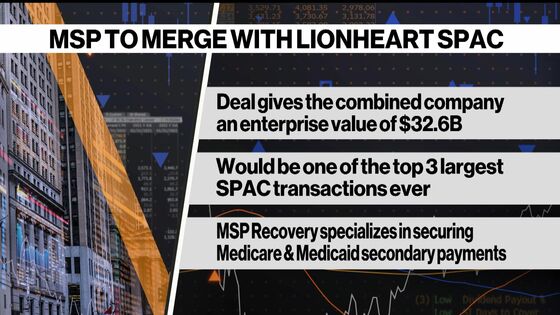

Yet today Ruiz is on the cusp of a $23 billion fortune as his MSP Recovery enters into a merger with Lionheart Acquisition Corporation II, a $230 million special purpose acquisition company founded by a former member of an Israel Defense Forces elite combat unit who spent most of his career in real estate.

If the deal is completed, it will go down as one of the most unusual SPAC transactions yet. Aside from the disparate backgrounds of its principals, the company forecasts zero revenue this year, there are none of the traditional co-investors participating and three of Lionheart’s directors have resigned in recent months. And at a $32.6 billion valuation, it’s the second-biggest proposed SPAC transaction after Grab Holdings’ $40 billion merger scheduled for later this year.

SPAC Fortunes

SPACs have become synonymous with enormous fortunes seemingly created overnight, such as the $11.3 billion stake Mat Ishbia realized when his mortgage company was taken public. But other fortunes have faded just as fast. Nikola Corp.’s Trevor Milton saw his net worth peak at almost $10 billion, according to the Bloomberg Billionaires Index, before allegations of fraud tanked the stock and forced him out of leadership at the company.

The frenzied dealmaking has also drawn the attention of regulators, who have zeroed in on the sometimes dubious business practices and questionable disclosures of merging firms, as well as the misalignment of interests between the people selling SPACs and those buying them. The Securities and Exchange Commission took the rare step this week of sanctioning a SPAC and its merger target — a space-cargo firm — for misleading investors.

The choice of MSP Recovery, a health-care payments recovery firm, comes despite Lionheart saying in its prospectus and website that it was looking for an acquisition in the real estate sector, which is where founder Ophir Sternberg spent most of his career.

After emigrating from Israel in 1993 and a stint in New York, Sternberg bought and sold real estate in South Florida for most of the past decade. But he spotted an opportunity in the red-hot world of SPACs, and in December led the combination of restaurant chain BurgerFi International Inc. with Opes Acquisition Corp.

BurgerFi shares closed Tuesday at $10.66, just above the $10 offering price of the SPAC that it merged with. For the year, they’re down 22%.

BurgerFi’s $100 million deal is set to be dwarfed by Lionheart’s combination with MSP. Sternberg took Lionheart Acquistion Corporation II public last August.

‘Deal Done’

“Most SPACs ask for a 24 months before they throw in the towel and have to redeem,” Sternberg told Bloomberg News at the time. “I told my investors at the IPO level that I was very confident that we could get a deal done within a shorter time frame, so I took the lifespan down to 18 months.”

That put added pressure on Lionheart to find a deal quickly, even as it competed against a greater number of SPACs chasing a limited number of potential targets. If no agreement is reached before 18 months, Sternberg and his team earn nothing from the SPAC.

Leading up to the MSP transaction, three directors on Lionheart’s five-person board resigned. One of them, Trevor Barran, who was also the firm’s chief operating officer, left last week, just days before the deal was announced on Monday. A fourth died in June.

“Lionheart brought in new board of director members to eliminate any potential or perceived conflicts of interest, better align the board’s collective expertise with MSP’s business, and to have a total of four independent directors, one more than required,” a spokesperson for Lionheart said in a statement.

MSP Recovery describes itself as a pioneer in obtaining reimbursements for Medicare and other health-care claims that should have been covered by other parties. The Coral Gables, Florida-based firm looks through records and identifies potentially erroneous payments using complex data analysis techniques. MSP said it owns nearly $50 billion in billed claims from its clients.

‘Humongous Flaw’

“The scalability of this business is beyond any business that exists,” said Ruiz, MSP’s founder and chief executive officer. “There’s a humongous flaw in the data capturing of medical claims and the insurance processing of those claims. This is a disruptive process that we’ve created and we’re changing the way that it’s done.”

If MSP is able to collect a payment, it typically shares half the money with the claim assignor, such as an insurance company that paid a wrong amount, and then pays lawyers 40% of the balance. MSP keeps what’s left.

A law firm owned by Ruiz and MSP’s chief legal officer will the exclusive lead counsel for MSP, meaning it stands to receive 20% of all recovered payments, according to a filing.

MSP calls the total amount recovered (before paying out the assignor and lawyers) gross revenue, and expects to take in about $3.1 billion in 2023. In an investor presentation, the company argued that its 10.5-times multiple against that revenue was in-line with prominent private equity firms it identified as peers, including Blackstone Group Inc., Brookfield Asset Management, Ares Management Corp. and KKR & Co.

It forecasts net revenue for that year of $963 million, and net income of $632 million. By 2026, it expects gross revenues of $23.8 billion.

Valuation Questions

Lionheart is putting as much as $160 million into MSP, depending on shareholder redemptions, in exchange for about 0.7% of the merged company. Unlike most SPAC deals, there’s no private investment in public equity, or PIPE, being injected alongside the SPAC.

That may be partly due to questions over valuation. Hedge fund Marshall Wace, an existing Lionheart investor, discussed participating in a PIPE at a valuation closer to $10 billion, according to a person with knowledge of the matter, who asked not to be identified discussing confidential information.

“A wide range of valuations, which didn’t include the entire scope of what’s included in the company now, were discussed at a very preliminary stage nearly six months ago,” Ruiz said.

A spokesperson for Marshall Wace declined to comment.

Shareholders who don’t redeem prior to the business combination are being offered at least 35 additional warrants allowing them to purchase shares at an $11.50 strike price. When those warrants are exercised, MSP’s founders — principally Ruiz — will sell their shares back to MSP at the strike price, meaning that on a net basis no new stock is issued. More than a billion such warrants will be dispersed.

Transaction Costs

Ruiz has agreed to sell a large portion of his shares at 15% above their $10 value implied by the transaction, limiting his upside. Ruiz says it was part of the cost of getting the deal done.

Lionheart’s sponsor, controlled by Sternberg, will get about $60 million of shares, according to an investor presentation. Transaction costs, including banker fees, will eat up $70 million or about 30% of the cash Lionheart raised from investors last year. The remaining cash will be used to fund operations and growth. MSP anticipates $37 million in expenses this year on no revenue.

“In the big scheme of things, it’s really de minimis,” Ruiz said, referring to the fees. “If I had to put a number on it, there’s more than 200, 300 people working on this deal.”

Of all the players, Ruiz stands to gain the most. His 70% stake in the firm is worth close to $23 billion at the combination price. MSP and Lionheart executives will be allowed to sell 10% of their shares as soon as the transaction is completed, with the remainder subject to a six-month lock up.

It should be enough to buy as many cigarette boats as Ruiz wants. In fact, in May, he bought Cigarette Racing Team — the company, not the boat. His partner on the deal? None other than Sternberg.

©2021 Bloomberg L.P.