Five Views on How Hard It Was to Trade Stock in Monday Meltdown

It’s a perennial villain, bad liquidity.

(Bloomberg) -- It’s a perennial villain, bad liquidity. Veteran traders have been warning that a breakdown in the stock market’s ease-of-use would one day have dire consequences for pricing. So how easy was it to do business Monday, during the worst sell-off in two years?

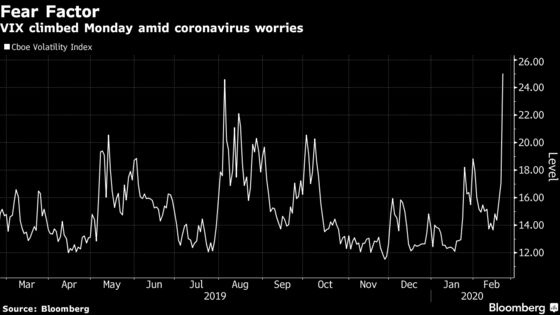

First the numbers. More than 10.5 billion shares worth $563 billion changed hands in the session, illustrating the extreme efficiency with which computers buy and sell. But high volume is not the same thing as high liquidity. Measures of share turbulence surged, with the Cboe Volatility Index climbing 8 points to 25. Volatility and the role played by electronic market makers are determinants in how easy stocks are to trade. It logically gets harder when prices bounce around.

Read More: Breakdown In Liquidity Is Exacerbating Today’s Equity Melt

Here’s what five market pros said they saw:

Max Gokhman, the head of asset allocation for Pacific Life Fund Advisors:

“We traded some equity futures today which, to be fair, are generally very liquid and we didn’t see any issues. And I have not heard from any of the brokers about liquidity issues on their ends. Not too worried about liquidity so far -- there are plenty of investors who still want to buy, and of course ones who are selling as more negative news comes out. From talking to folks on various desks this morning it seems like the balance was tilted to defensives/puts/selling today, but nothing that would create a liquidity crunch.”

Delores Rubin, a senior equity trader at Deutsche Bank Wealth Management:

“My flow is not going to be indicative of those on the institutional side and of course algos play a big role in the quick movements, as we saw in the last five minutes of the day,” she said. “Liquidity is not an issue. The market is also very orderly. It opened in-line with global equities. ... I suspect there are still a good number of investors itching to put more money to work, but are trying to determine if we have more worry ahead and either wait or pull the trigger. As we closed at the lows, there is obviously a good amount of concern as to how prolonged of an effect this outbreak will have.”

Joseph Saluzzi, Themis Trading LLC partner and co-head of equity trading:

“Liquidity as defined by some would be, ‘Can I sell my whole piece here,’ and if that’s the definition, then there were definitely liquidity issues. Nobody’s going to step up and buy in front of a freight train. Buyers were likely being very pricey and picking spots, which is prudent. But, people need to realize that there really is no buffer supplied by diverse limit orders of any size. Most orders are chopped into smaller orders and sliced out by algos all day now.”

Chris Harvey, the head of equity strategy at Wells Fargo Securities, wrote in a note Monday:

“On our Equity desk, we are not seeing panic-selling. In actuality, the desk is better to buy. Derivative traders are busy and the action is varied with some hedging and some monetizing hedges. Conversations with Rates players indicate the focus is on convexity hedging and the worry is yield movements have the potential to be very fluid.”

Frank Ingarra, head trader at Greenwich, Connecticut-based NorthCoast Asset Management LLC:

“We were not active at all today. We wanted to wait and see what happens, use logic and see how the market digests the news. It was obvious going into Monday that we’d get a sell-off, and we didn’t want to move on yesterday’s news. We want to see how the decline affects valuations and technicals to see how invested we should be, and it takes some time to get through. There wasn’t anything extraordinary in terms of client activity. Advisers were on the phones and doing regular calls, but that’s about it. I didn’t feel any panic, didn’t hear any panic. We’re still about 75% invested.”

--With assistance from Elena Popina.

To contact the reporters on this story: Vildana Hajric in New York at vhajric1@bloomberg.net;Sarah Ponczek in New York at sponczek2@bloomberg.net

To contact the editors responsible for this story: Jeremy Herron at jherron8@bloomberg.net, Chris Nagi, Richard Richtmyer

©2020 Bloomberg L.P.