Five Things to Watch in European Tech, Media and Telecom in 2019

Here’s a look at some of next year’s biggest themes for investors in European technology, media and telecommunications stocks.

(Bloomberg) -- Here’s a look at some of next year’s biggest themes for investors in European technology, media and telecommunications stocks -- including a flashpoint for the U.S.-China trade war and rejuvenated consolidation hopes boosting an industry long shunned by the market.

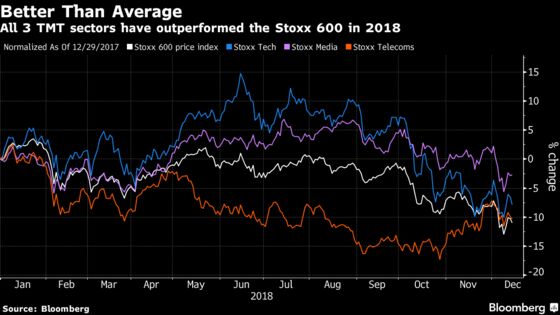

All three sectors have fared better than the regional benchmark during this year’s stock rout, media stocks being one of the best-performing groups in the Stoxx 600 Index with just a 2.6 percent decline, technology falling 7.4 percent and telecoms mounting a late comeback to pare losses to 9.7 percent. The Stoxx 600 is down 11 percent on the year.

5G Networks

Nokia Oyj and Ericsson AB -- among 2018’s best-performing European technology stocks -- could be on track for an effective duopoly next year in the Western markets for 5G equipment.

Their main rival, Huawei Technologies Co., is running into growing opposition from governments worried that its systems could be used by Chinese intelligence, just as countries around the world are planning the next generation of communications networks. Huawei says it’s willing to spend and do whatever needed to convince officials it can be trusted.

This battle will continue to make headlines well into next year, to the benefit of the Nordic rivals. “The U.S. and her allies are now doing everything they can to cut the heart of the Chinese technology IP revolution,” Neil Campling, an analyst at Mirabaud, wrote in a report this month. “This, 5G, is going to be the epicenter of a bloody IP battle war between China and the U.S. in 2019 -- the 2018 tariffs could seem like a drop in the ocean compared to this.”

Telecom Deals

Telecommunications stocks, among the worst performers in Europe in the first nine months of the year, have rallied during the year-end sell-off. Their high dividend yields, cheap valuation and increased merger prospects made the sector that much more attractive after three lean years.

A favorable ruling by European competition authorities on a merger in the Netherlands has encouraged investors that “2019 will kick off with fueled expectations of M&A,” Guy Peddy, an analyst at Macquarie, wrote in a note on Dec. 12. But it would be irrational to assume that the telecom business will be healthier, he said.

“We like telcos right now because they’re cheap relative to the market but also because I think we’re at a real moment of change,” Hugh Cuthbert, co-manager of SVM All Europe SRI Fund, said by phone. “The industry should start to converge together, particularly in Europe, in order to take advantage of scale” as carriers look to buy new 5G equipment.

Cuthbert owns Orange SA shares, which he sees as a beneficiary from mergers in the French market, even if it wouldn’t directly participate in a deal.

Consolidation has been an on-and-off topic for years in France, while in Italy, speculation of a potential split of Telecom Italia SpA’s network unit remains rife. The U.K. may see its share of movement with a long-awaited listing of Telefonica SA’s O2 unit, reportedly delayed until after Brexit, and Vodafone Group Plc pursuing its deal to buy almost a third of Liberty Global Plc.

Falling Chips

Investors riding the wave of semiconductor stocks during the age of smartphone proliferation have painfully crashed into the shore this year. Some of last year’s best stocks are this year’s worst, and may have more declines ahead of them. AMS AG, which makes sensors used for the facial recognition capabilities of Apple Inc.’s flagship iPhones, has slumped 75 percent after tripling in value in 2017.

That came as the trade dispute between the U.S. and China ramped up over the summer, with both sides implementing tariffs on exports. Combine this with worries that the semiconductor cycle has peaked, historically inflated valuations and recent outlook cuts across the industry, and it’s no surprise semis have come tumbling down so quickly.

“If you supply Apple and you’re cheap, I’m not that interested,” Carlos Moreno, co-manager of the Miton European Opportunities fund, said in a phone interview.

It’s not all doom and gloom for 2019 however, as the rout has made stocks that are less exposed to Apple or cyclical trends more attractive. Moreno bought equipment maker ASML Holding NV in October and owns two other semi-exposed stocks: vacuum valve maker VAT Group AG and Lem Holding SA, which supplies electrical components to the chip industry.

Moreno said he likes unique businesses with high or dominant market share, and is happy to pay up for them.

Ad Clouds Clearing?

Stocks reliant on advertising struggled in 2018, despite a year that saw a number of events boosting growth, including the Winter Olympics and the World Cup. U.K. advertising company WPP Plc failed to halt last year’s plunge and is down by more than a third, German broadcaster ProSiebenSat.1 Media SE has declined 44 percent and ITV Plc has dropped 22 percent.

The struggle is partly a result of clients cutting back on ad spending and going straight to online firms or consultants increasingly encroaching on traditional advertising companies’ turf. Digital advertising will solidify its position as the world’s biggest ad platform in 2019 with $285 billion, topping TV for the third year in a row, according to forecasts by Magna Global.

Ad agencies in 2019 will be “unable to shake off multiple threats that are contributing to an increasingly negative narrative,” Bloomberg Intelligence analysts Paul Sweeney and Geetha Ranganathan write. “Deep-pocketed, non-traditional buyers, including consultancies, are expected to be active in M&A as they look to beef up their capabilities.”

Ad companies are trying to convince investors of their staying power. WPP’s shares gained last week after Chief Executive Officer Mark Read announced a plan aimed at simplifying the company and returning it to growth, similar to the turnaround under way at Publicis Groupe SA.

Payment Stocks

This has been a very good year for fintech. Adyen NV provided one of the year’s hottest public listings, Wirecard AG supplanted Commerzbank AG in the German DAX Index and a number of takeovers delivered some added spice to the sector. The main question is whether the payment companies’ lofty growth expectations are now priced in or whether there’s more to come.

“It’s difficult to see what the incremental good news is that the market doesn’t know about, so we like them,” SVM’s Cuthbert said. “We just see other stocks with better value right now.”

Investors who got in at the initial public offering price of Adyen have nearly doubled their money in the Dutch payment processor, which counts Uber Technologies Inc. and Airbnb Inc. among its clients. Adyen is set to overtake Worldpay Inc as the largest online payment-service provider next year or in 2020 at the latest, Exane analysts forecast in September.

The analysts estimate e-commerce is set to grow about 10 percent annually over the next few years, and provides an addressable market of about $1.8 trillion, excluding the combined 30 percent controlled by Amazon Inc. and that belonging to the less-accessible Chinese market.

All of this has forced banks to pay closer attention. On Tuesday, we’ll take a look at five things to watch for in European financial stocks, including a further exploration on how traditional industry players are preparing for the rise of fintech.

To contact the reporters on this story: Kasper Viita in London at kviita1@bloomberg.net;Kit Rees in London at krees1@bloomberg.net

To contact the editors responsible for this story: Celeste Perri at cperri@bloomberg.net, Phil Serafino, Jon Menon

©2018 Bloomberg L.P.