Five Key Takeaways From the Biggest U.S. Banks' Earnings Reports

Five Key Takeaways From the Biggest U.S. Banks' Earnings Reports

(Bloomberg) -- As earnings season for the biggest U.S. banks wrapped up on Tuesday, the benefits to Wall Street of rising interest rates and a healthy economy became clear.

Major U.S. lenders including JPMorgan Chase & Co., Morgan Stanley and Bank of America Corp. reported increases in net interest income, even as trading businesses saw more mixed results. And while rate hikes can result in consumer defaults, Wells Fargo & Co. and Citigroup Inc. said their costs for bad loans are actually falling -- one benefit of a strong economy. Still, executives pointed to trade conflicts and other political uncertainties that could cause trouble down the road.

Here are five key takeaways:

Bump in Net Interest Income

The Federal Reserve’s rate hikes helped boost net interest income, the difference between how much banks make lending money and the amount they pay depositors. NII hit records at JPMorgan and Wells Fargo, while at Bank of America it rose 6 percent to its highest level since 2011. At Morgan Stanley, the measure jumped 20 percent from the same period last year. Net interest margins climbed at the lenders even as they passed on some higher rates to depositors.

JPMorgan CEO Jamie Dimon said people should be prepared for interest rates to go higher. “We need that,” particularly when the economy is strong, he said.

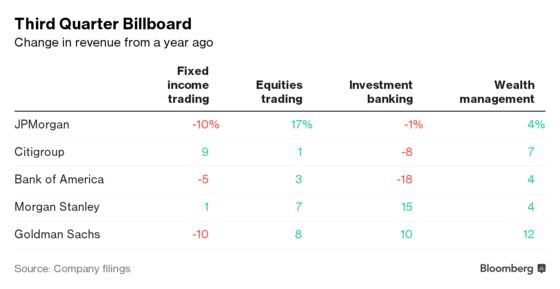

Equities Versus Fixed-Income Trading

Banks saw positive results for equities trading, while fixed-income trading revenue generally declined. JPMorgan’s trading revenue of $4.4 billion was helped by a 17 percent jump in equity trading, while its fixed-income trading revenue fell short of analysts’ estimates. Equities revenue at Goldman Sachs Group Inc. was up 8 percent to $1.79 billion, topping estimates of $1.73 billion, as fixed-income revenue slumped 10 percent.

The outlier was Citigroup, which post a surprise gain on fixed-income trading. The bank said that resulted from the elevated client activity it saw around the Federal Reserve’s rate hike in late September.

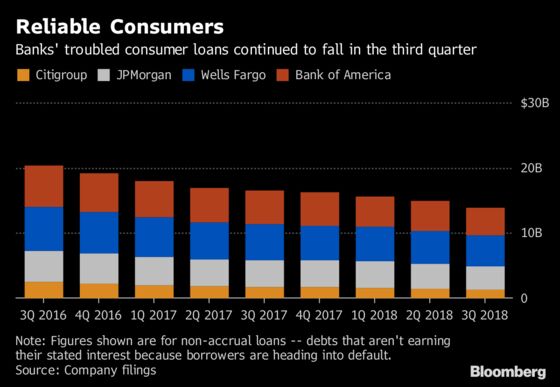

Consumer Credit Quality

Usually, consumers carrying too much debt start to default as interest rates rise, but this quarter banks reported that their costs for bad loans are falling. Wells Fargo and Citigroup both cut the amounts they set aside for consumer loan losses by at least 13 percent, and JPMorgan’s provision for bad loans was half a billion dollars less than analysts estimated.

“It’s a combination of people being more disciplined and banks better managing their balance sheets,” said Mark Doctoroff, co-head of Mitsubishi UFJ Financial Group Inc.’s financial institutions group. “It’s much harder now to get a consumer loan.”

Investment-Banking Standouts

Morgan Stanley and Goldman both saw surges in their investment-banking businesses, leading to better-than-expected profits as peers slumped. Investment-banking revenue was up 15 percent at Morgan Stanley and 10 percent at Goldman. JPMorgan, Citigroup and Bank of America Corp. posted declines.

Morgan Stanley Chief Financial Officer Jonathan Pruzan said the firm’s gains came from “strengthening relationships, gaining share and the global footprint working.”

Related: Morgan Stanley, Goldman soar past rivals with dealmaking

At Goldman, dealmakers delivered a pleasant surprise for new Chief Executive Officer David Solomon, who spent a decade leading the investment-banking division. The firm’s investment-banking revenue of $1.98 billion surpassed the average analyst estimate of $1.75 billion. Both Goldman and Morgan Stanley got a boost from an increase in initial public offerings, while their debt-underwriting units were able to withstand a slowdown better than their peers.

Caution on Macro Risk

Wall Street leaders voiced concern about the potential harm to the economy from geopolitical uncertainties. Trade tensions between the U.S. and China may challenge some key areas of growth, Pruzan said, and IPO activity in Asia could fall “pretty dramatically” after strong equity underwriting in the region earlier in the year.

Dimon, meanwhile, pointed to myriad challenges that could take a toll on U.S. and global growth: escalating trade skirmishes, rates rising faster than expected, Brexit, Italian sovereign-debt problems, rising tensions with Saudi Arabia and higher mortgage rates.

“There’s eight or nine things out there,” he said on a call with journalists. “In general, those things don’t necessarily derail the U.S. economy, but they are all out there. No one should be surprised if it happens down the road.”

--With assistance from Sonali Basak, Sridhar Natarajan, Michelle F. Davis, Jenny Surane, Katherine Chiglinsky and Hannah Levitt.

To contact the reporter on this story: Claire Ballentine in New York at cballentine@bloomberg.net

To contact the editors responsible for this story: Michael J. Moore at mmoore55@bloomberg.net, Daniel Taub, Dan Reichl

©2018 Bloomberg L.P.