Ferraris, BMWs Hold the Keys to Rally Ignition: Taking Stock

Ferraris, BMWs Hold the Keys to Rally Ignition: Taking Stock

(Bloomberg) -- Though U.S.-China talks are set to resume today in Washington (higher level talks don’t begin until Thursday), trade issues with another major partner, Europe, should instead be on your radar.

European automakers are broadly lower, with Fiat Chrysler ADRs trading down 1.3% in the pre-market after German Chancellor Merkel fired a preemtive salvo against the prospect of further tariffs, which President Trump may consider after the Commerce Department report was issued over the weekend, discussing whether or not autos posed a national security threat.

The trade issues above, together with a cacophony of Fed speak and FOMC minutes should keep investors on their toes in the holiday-shortened week, given the pace of earnings slowing materially. A partial trade deal has been "increasingly" priced into the equity market, according to Bank of America Merrill Lynch analysts in a note to client last week, meaning any development should be carefully parsed as to whether it truly advances the narrative toward a total deal. The strategists saw the prospect of upside near 5-10% assuming such a deal is completed, and highlight that given the situation for the U.S. President domestically, these trade talks "necessitate a win." Equities that are expected to remain volatile and remain in focus will be those with a high proportion of China sales and imported materials.

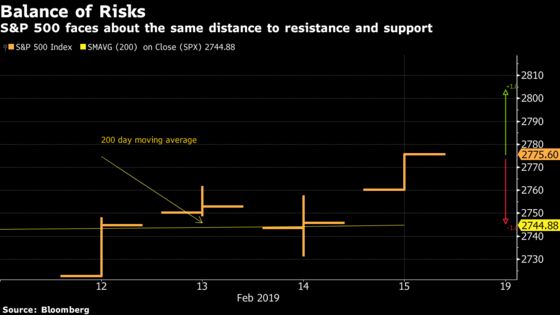

Coin Flip

We are poised to open sandwiched between two key technicals, approximately 1% to the upside (which some strategists say is critical in the 2,800-2,815 range) and 1% to the downside (the 200-DMA). Does that mean its 50/50 which we hit first? The bias has clearly been to the upside this year (6 of the first 7 weeks of the year have closed higher), though the week brings potential catalysts (Mester later this morning and the FOMC tomorrow) that could lessen that Fed "pivot" just enough to erase some of those gains. With Walmart (0.6% of the S&P) results blowing out expectations, we may now seem tilted to the upside. General Mills, which counts Walmart as its largest customer, according to data compiled by Bloomberg, is due to present at the CAGNY conference later today, another major event that warrants your attention through this week.

But if the major indices don’t suit your fancy, it might be worth watching the small caps. Barclays strategist Venu Krisha has been pounding the table on the segment for weeks now, last week even highlighting the expectation that they would outperform large caps through 2019. He acknowledges, however, that the Russell 2000 is approaching their target, but nevertheless finds the "idiosyncratic headwinds" that have impacted small caps are dissipating. This column two weeks ago discussed the small cap bounce, which Krisha says is no "head fake." They still had lagged the S&P from their pre-selloff levels.

Sectors in Focus Today

- Housing exposed names as furniture, home decor and security as TILE, TTS, LZB and ALLE (just missed on forecasts) report results

- ADRs in European banks (DB, BCS, CS) after HSBC’s profit results miss

- Car makers after EU threatened to retaliate if the U.S. imposed tariffs on vehicles deemed a security threat

- Auto parts companies (ORLY, AZO, GPC) after Advance Auto disappointed and JPMorgan initiated ratings on the auto dealer space (LAD, CPI, ABG, PAG, AN)

- Marijuana stocks (CGC, ITHUF, CURLF, MMNFF, ACRGF, GTBIF etc) after Barron’s expressed caution on their levels of risk considering it remains illegal in the U.S.

- Student loan players like SLM, NNI after Navient rejected a bid at $12.50/shr (NAVI trades a discount to peers, according to Bloomberg data)

Your 87-Hour ICYMI

Berenberg analysts speculated that LVMH and Diageo could look at making a bid for Pernod Ricard; Navient rejected an offer from Canyon Capital/Platinum Equity at $12.50/shr in cash; Canada PM Justin Trudeau’s top aid Butts resigned, citing allegations Butts pressured a justice official in an SNC Lavalin matter; Germany banned the short sales in shares of the recent short-seller target Wirecard until April 18; China is seeking to build a solar power station in Space; Founder of Baring Vostok Capital Partners, American Michael Calvey, was detained in Moscow related to a commercial dispute; American Vice President Pence called for EU Nations to leave the Iran deal; former Deputy FBI Director Andrew McCabe’s interview on 60 minutes prompted responses from President Trump and Senator Lindsey Graham, who vowed to open an investigation into the details discussed; Trump also tweet responded to SNL’s latest skit (again) in between those on Venezuela and McCabe, asking how networks get away with it; Bryson Dechambeau holed out three times in his opening rounds at the Genesis which was ultimately won by JB Holmes who was under criticism for slow play; OKC Thunder’s rookie Hamidou Diallo called out Shaq during his Slam Dunk contest win at the All Star Game (Brooklyn Nets’ Joe Harris beat Steph Curry for the 3-point shooter title); the Daytona 500 encountered a huge delay after a 20+ car accident occurred with 10 laps to go.

Notes from the Sell Side

Checks on Weight Watchers International indicate that the weight management company’s daily active users (via app usage) are continuing to contract, JPMorgan analysts led by Christina Braithwaite write in a downgrade to underweight from neutral. This comes after a January downgrade by the same analysts, who note that the trends have worsened since then, while reviews have been "increasingly negative." Shares are indicated to open lower by nearly 7%.

PG&E Corp. shares, the California a utility embroiled in multiple wildfire lawsuits and a pending bankruptcy, are up nearly 9% after Citi raised its rating to a buy/high risk rating, citing the potential for "timely legislative" action. Analyst Praful Mehta cites recent public comments from the Governor and the prospects that legislation could be passed in the near term that could cap wildfire risk. The shares offer a "great" entry point with an upcoming catalyst, the analyst wrote.

Tick-by-Tick Guide to Today’s Actionable Events

- CAGNY conference

- 8:00am -- MDT earnings, WMT earnings call; GIS at CAGNY conference

- 8:50am -- Fed’s Mester on the economic outlook and monetary policy

- 9:00am -- RIG earnings call; JNJ at CAGNY conference

- 10:00am -- Feb NAHB Housing Market index

- 11:00am -- SYY, TSN at CAGNY conference

- 12:00pm -- CLR earnings call; ALLK, JEC investor day

- 1:00pm -- MDLZ at CAGNY conference

- 4:00pm -- PFGC at CAGNY conference

- 4:10pm -- HLF earnings

- 5:30pm -- HLF earnings call

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.