Feeling Risky? WeWork’s 15% Bonds Would Be for Bravest of Brave

Feeling Bold? WeWork’s 15% Bonds Would Be for Bravest of Brave

(Bloomberg) -- JPMorgan Chase & Co. bankers have what might be one of the least enviable jobs on the Street today: convincing credit investors to lend to WeWork in a debt deal that practically redefines risky.

The office-sharing company is weighing a potential $5 billion debt package that could include some $2 billion of pay-in-kind bonds with a yield an eye-popping 15%, Bloomberg reported Monday.

Lending to WeWork is so potentially dicey that one junk-bond investor, Diamond Hill Capital Management’s John McClain, said anybody brave enough to do it would “be taking on substantial career risk.”

The $2 billion payment-in-kind deal is one of the largest such debt offerings in the U.S., and places WeWork in the same unwanted company as distressed oil drillers, coal miners and department stores. Existing bondholders reacted harshly, sending WeWork’s notes due in 2025 to their lowest price in history.

Confidentiality Agreements

Some 60 firms have signed confidentiality agreements to examine the potential transaction, an unusually wide net for this type of deal. They include investors ranging from some of the world’s largest asset managers to credit hedge funds with expertise in distressed investing, according to people familiar with the matter.

Payment-in-kind notes, known as PIKs in industry parlance, are among the riskiest types of high-yield debt financing. That’s because they give issuers the option to pay interest on debt with more debt. In buying PIK deals, investors are effectively betting that a cash-strapped company will be able to make good on a ballooning debt obligation when it matures.

PIK debt has historically been favored by the likes of struggling energy companies and firms exiting bankruptcy. Department store chain Neiman Marcus Group issued $550 million in debt this year, while Aston Martin Lagonda Global Holdings did $150 million, but both of those deals were far smaller than what WeWork is considering.

WeWork’s $2 billion PIK note, if it happens, would surpass in size once-bankrupt telecommunications company Oi SA‘s $1.7 billion offering last year.

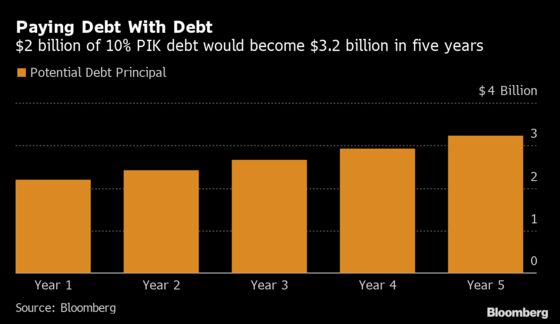

While terms remain under discussion, the potential WeWork PIK could pay 5% interest in cash and 10% interest in debt that would accumulate and become due at maturity.

That means that a $2 billion obligation with a 10% payment-in-kind option would grow to $2.7 billion after three years and $3.2 billion after five.

The market’s initial reaction wasn’t encouraging. WeWork’s bonds due in 2025 plunged to the lowest price on record Tuesday morning in New York to yield more than 13% before retracing some of those losses. The new debt could come with a coupon nearly twice as high as the junk bonds the company sold less than 18 months ago.

“If they are talking about doing a PIK note at a yield of 15%, the existing unsecureds have to reprice,” McClain said.

Existing debt investors point out that the company bleeds cash and lacks a clear path to profitability. WeWork put off an initial public offering last month when investors spurned the deal.

The company risks running out of cash as soon as next month, making the work of JPMorgan’s bankers more urgent. WeWork’s leaders hope to turn around the venture with emergency borrowing, even if it’s expensive, rather than see early backers’ equity and influence diminished in a rescue by SoftBank, its largest shareholder. The financing would require SoftBank to contribute some $1.5 billion of funding next year.

Equity Warrants

The $2 billion of unsecured debt may carry a sweetener: equity warrants designed so that investors could boost their return to around 30% -- if the company gets to a $20 billion valuation. That’s a hefty payout for debt investors at a time when even the riskiest-rated junk bonds yield an average of 11.1%.

Even so, any type of debt package could be difficult to sell to investors, according to Bloomberg Intelligence analyst Arnold Kakuda.

“There may be little appetite for more junk bonds from a restructuring, cash-burning business that withdrew its IPO filing,” Kakuda wrote in a note Monday.

Vicki Bryan, chief executive officer of Bond Angle, a high-yield credit research company, said in a note Tuesday that the potential 15% coupon might not be enough compensation given WeWork’s risks. She recommends that prospective investors push for a yield of 18% or more on a bond in the five to seven-year range.

“After all, WeWork’s credit metrics remain off the chart ugly,” Bryan said in the note.

--With assistance from Lisa Lee, Katherine Doherty, Davide Scigliuzzo and Natalie Harrison.

To contact the reporter on this story: Claire Boston in New York at cboston6@bloomberg.net

To contact the editors responsible for this story: Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Larry Reibstein, Adam Cataldo

©2019 Bloomberg L.P.