Powell Signals Prolonged Fed Pause as Inflation Lags, Risks Loom

The Fed’s signal that it will keep interest rates on hold for the full year reflects concerns that economic growth is slowing.

(Bloomberg) -- Federal Reserve Chairman Jerome Powell said interest rates could be on hold for “some time” as global risks weigh on the economic outlook and inflation remains muted.

“We don’t see data coming in that suggest that we should move in either direction. They suggest that we should remain patient and let the situation clarify itself over time,” he told a press conference Wednesday after officials slashed their projected interest-rate increases this year to zero from two. “It may be some time before the outlook for jobs and inflation calls clearly for a change in policy.”

Officials also decided to slow the drawdown of the U.S. central bank’s bond holdings starting in May, then end them in September. Together, the moves complete the Fed’s 2019 pivot away from policy tightening and toward a markedly cautious stance -- a sign that policy makers take risks to their outlook seriously even as the domestic economy chugs along.

Financial markets confirmed the dovish interpretation, with futures traders lifting the probability of the Fed cutting rates this year to almost one-in-two. The 10-year Treasury yield dropped to its lowest level in more than a year, while the dollar was poised for its biggest daily loss since January. Stocks retreated.

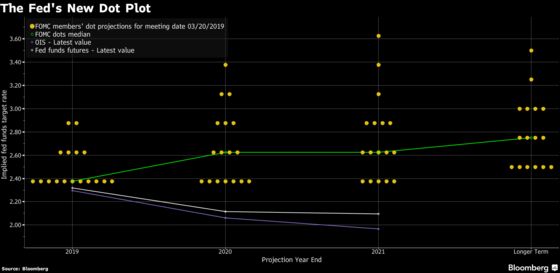

The unanimous decision held the target range of the federal funds rate at 2.25 percent to 2.5 percent. The Fed’s signal that it will keep rates on hold goes further than the one-hike forecast analysts had expected in a Bloomberg survey.

Read more: Bloomberg’s TOPLive blog on the Fed decision

Powell sounded the alarm on low inflation during his post-meeting press conference, calling weak global price pressures “one of the major challenges of our time.” He indicated that the continually plodding price gains leave the central bank room to proceed with caution.

“I don’t feel that we have kind of convincingly achieved our 2 percent mandate in a symmetrical way,” he said. “That gives us the ability to be patient, and not move until we see that our target goals are being achieved.”

The doubling-down on patience caught some Fed watchers by surprise.

“It was very dovish,’’ said Stephen Stanley, chief economist at Amherst Pierpont Securities LLC. “It suggests that the Fed has jumped to the conclusion that the weakening we have seen since the start of the year will be more fundamental and more persistent, rather than being temporary crosscurrents.”

In a separate statement Wednesday, the Fed said it would start slowing the shrinking of its balance sheet in May -- dropping the cap on monthly redemptions of Treasury securities from the current $30 billion to $15 billion -- and halt the drawdown altogether at the end of September. After that, the Fed will likely hold the size of the portfolio “roughly constant for a time,” which will allow reserve balances to gradually decline.

What Bloomberg’s Economists Say

“Policy makers appear to have cooled on the notion of any meaningful, lasting impact from last year’s tax reforms and instead project a return to trend growth, a stabilization of the unemployment rate and little pickup in price pressures. Amid this backdrop, they do not see much need to further normalize interest rates.”

-- Carl Riccadonna, Yelena Shulyatyeva and Tim Mahedy, U.S. economists

Click here to view full report

Beginning in October, the Fed will roll its maturing holdings of mortgage-backed securities into Treasuries, using a cap of $20 billion per month. The initial investment in new Treasury maturities will “roughly match the maturity composition of Treasury securities outstanding,” the Fed said. The central bank is still deliberating the longer-run composition of its portfolio and said “limited sales of agency MBS might be warranted in the longer run.”

Global Risks

While the central bank is very close to its twin goals of low and stable inflation and full employment, Powell cited risks from abroad including trade disputes, slowing growth in China and Europe, and possible spillovers from Britain’s exit from the European Union.

“The reason we’re on hold is that we think our policy rate is in a good place, and we think the economy is in a good place, and we’re watching carefully as we see these events evolve around the world and at home,” he said.

Read More: U.S. Federal Reserve’s Economic Projections (Table)

The Fed formally adopted its 2 percent inflation goal in 2012, and price gains have mostly come in on the low side since then.

Policy makers slightly lowered their expectations for inflation relative to their last set of economic projections. After 1.8 percent headline inflation in 2019, they see price gains of 2 percent on both the main and core indexes for the following two years, eliminating the overshoot they had previously projected.

They left their longer-run interest rate projection unchanged. While officials previously expected to overshoot that long-run level, roughly the one that neither stokes nor slows growth, they now see rates hovering below it at least through 2021.

“Patient means that we see no need to rush to judgment,” Powell said.

--With assistance from Kristy Scheuble, Richard Miller, Liz Capo McCormick, Christopher Condon, Craig Torres, Steve Matthews and Matthew Boesler.

To contact the reporters on this story: Jeanna Smialek in New York at jsmialek1@bloomberg.net;Matthew Boesler in Washington at mboesler1@bloomberg.net

To contact the editors responsible for this story: Brendan Murray at brmurray@bloomberg.net, Alister Bull, Scott Lanman

©2019 Bloomberg L.P.