Fed’s Plan to Tackle Funding Crunch Faces Test in Auction Slate

Fed’s Plan to Tackle Funding Crunch Faces Test in Auction Slate

(Bloomberg) -- The Treasury’s next round of auctions starting Monday is set to serve as the first test of whether the Federal Reserve’s steps to tackle the funding crunch have been sufficient.

After a tumultuous few days in which funding costs spiked to record levels, calm returned to this vital corner of the financial markets following the New York Fed’s announcement Friday of a series of overnight and term operations for the next three weeks.

“The Fed just reminded the market that they have complete control over the front-end if and when they want it,” said BMO Capital Markets strategist Jon Hill. “Given the volatility we saw this week, they want to ensure quarter-end goes as smoothly as possible.”

But before quarter-end, the market will have to absorb more than $200 billion of bill and note auctions this week, starting with Monday’s three- and six-month debt. Amid volatility in the repo market, bill auctions met a poor reception Thursday, a sign of investors’ skepticism that the Fed’s action to that point would prove effective.

On Friday, the New York Fed said it will conduct overnight repurchase agreement operations daily until Oct. 10. This Monday’s operation will be for as much as $75 billion, while the actions thereafter will be for at least that amount. Separately, it will also conduct three 14-day term operations for an aggregate amount of at least $30 billion on Sept. 24, Sept. 26 and Sept. 27, according to a statement.

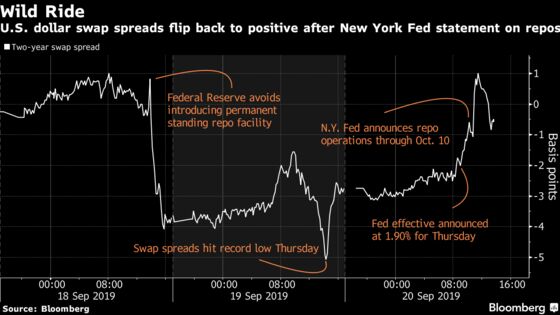

There were immediate signs of easing concerns. Swap spreads widened, showing that worries over dealers’ financing costs were ebbing.

“This is a more concerted effort to ensure confidence in the market that the Fed will do what is necessary to quell serious volatility in the repo market and consequently the policy rate,” said Jonathan Cohn, strategist at Credit Suisse. “The market reaction shows it has had a significant positive reaction, with the sharp widening of the two-year swap spread.”

The announcement of the operations going forward followed the New York Fed’s four straight days of overnight liquidity injections as it sought to ease the funding stress that had rippled through markets in previous days.

Surges in the repo rate normally occur only at quarter-end and sometimes month-end. This mid-month jump was attributed to a confluence of events that knocked cash reserves in the banking system out of balance with the volume of securities on dealer balance sheets: a corporate tax payment date, settlement of last week’s Treasury auctions, and last week’s bond-market sell-off, in which investors sold securities back to dealers.

The New York Fed injected $75 billion Friday through an overnight repo operation. That followed actions of the same size on Wednesday and Thursday, and $53.2 billion on Tuesday, with each of these prior agreements rolling off the morning after they’re completed.

Temporary Add

The measures, commonplace in pre-financial crisis times, temporarily add cash, with the Fed taking government securities as collateral.

The latest addition of liquidity follows the Federal Open Market Committee’s move Wednesday to reduce the interest rate on excess reserves, or IOER, by more than their main interest rate -- all attempts to quell money-market stresses.

The moves calmed the funding market, with repo rates declining to more normal levels after soaring to 10% Tuesday, four times last week’s levels. Overnight general collateral repurchase agreement rates remained steady Friday, trading around 1.9%, according to ICAP.

A parade of Fed officials will appear next week, starting with New York Fed President John Williams on Monday. Chairman Jerome Powell said Wednesday that he was confident the New York Fed’s actions would contain funding problems. Former New York Fed President William Dudley echoed that view in an editorial published Friday.

The Fed effective on Thursday was 1.9% -- within the central bank’s target rate range of 1.75% to 2%. That compares to 2.25% on Wednesday, and 2.3% Tuesday -- when it busted above the top of the Fed’s previous target band, before policy makers lowered borrowing costs on Wednesday.

What to Watch Next Week

- The Fed is flooding the zone:

- Sept. 23: Williams speaks at the New York Fed’s annual U.S. Treasury Market Conference; San Francisco Fed’s Mary Daly and St. Louis Fed’s James Bullard also have appearances

- Sept. 25: Chicago Fed’s Charles Evans; Kansas City Fed’s Esther George; Dallas Fed’s Robert Kaplan

- Sept. 26: Kaplan; Bullard ; Vice Chairman Richard Clarida and Daly at event in San Francisco; Minneapolis Fed’s Neel Kashkari; Richmond Fed’s Thomas Barkin

- Sept. 27: Fed Vice Chairman for Supervision Randal Quarles; Philadelphia Fed’s Patrick Harker

- Here are some of the highlights of the economic calendar

- Sept. 23: Chicago Fed activity index; Markit U.S. PMI

- Sept. 24: Home price indexes; Richmond Fed manufacturing index; Conference Board consumer confidence

- Sept. 25: MBA mortgage applications; new home sales

- Sept. 26: GDP; personal consumption; trade balance; retail, wholesale inventories; initial jobless claims; Bloomberg consumer comfort; pending home sales; Kansas City Fed manufacturing

- Sept. 27: Personal income, spending; PCE deflator; durable goods orders; University of Michigan sentiment

- On the auction block

- Sept. 23: $45 billion 3-month bills, $42 billion 6-month bills

- Sept. 24: $40 billion 2-year notes

- Sept. 25: $18 billion 2-year floating-rate notes reopening; $41 billion 5-year notes

- Sept. 26: 4- and 8-week bills; $32 billion 7-year notes

--With assistance from Edward Bolingbroke and Emily Barrett.

To contact the reporters on this story: Alexandra Harris in New York at aharris48@bloomberg.net;Liz Capo McCormick in New York at emccormick7@bloomberg.net

To contact the editors responsible for this story: Benjamin Purvis at bpurvis@bloomberg.net, Debarati Roy, Mark Tannenbaum

©2019 Bloomberg L.P.