Fed MBS Buying High on Agenda as Officials Begin Taper Talk

Economists surveyed by Bloomberg expect Fed to leave their support in place and be silent on taper timing in their statement.

(Bloomberg) -- Sign up for the New Economy Daily newsletter, follow us @economics and subscribe to our podcast.

Policy hawks at the Federal Reserve are setting their sights on scaling back the U.S. central bank’s massive intervention in the mortgage market as home prices soar. But the Fed leadership doesn’t sound convinced by arguments in favor of a hasty exit strategy.

The debate -- over whether to taper the Fed’s purchases of mortgage-backed securities faster than its buying of Treasury debt -- will probably be near the top of the agenda when officials gather July 27-28 to discuss next steps for policy.

Economists surveyed by Bloomberg expect them to leave their support in place and be silent on taper timing in their statement, released at 2 p.m. Washington time Wednesday. Pressure on Chair Jerome Powell to begin scaling back bond buying sooner rather than later has probably eased amid concern that spread of the coronavirus delta variant could sap the economic recovery.

Goldman Sachs Group Inc. economists lowered their forecast for U.S. gross domestic product growth in the final two quarters of 2021 by one percentage point to 8.5% and 5% respectively.

“It is increasingly clear that while mass vaccination has had a huge impact on service sector activity, it is unrealistic to expect virus fears to instantly disappear entirely,” economists led by Jan Hatzius wrote in a report to clients.

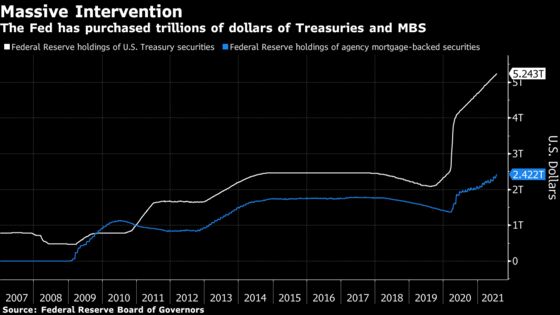

The central bank is holding interest rates near zero and currently buying $80 billion of Treasuries and $40 billion of agency MBS each month as part of the crisis-era bond-buying programs it relaunched last year at the onset of the pandemic. Economists expect it to begin scaling back purchases later this year, or early in 2022.

First, Fed officials must decide on when and how to begin doing so. A key question is whether to taper purchases of Treasuries and MBS at similar rates or, alternatively, prioritize reductions in purchases of MBS given the state of the housing market.

“The agenda for this next meeting is probably to start hashing out some of the logistics,” said Aneta Markowska, chief financial economist at Jefferies LLC in New York. “On timing, it’s still too early to make decisions, but I think the focus is going to be on those operational details.”

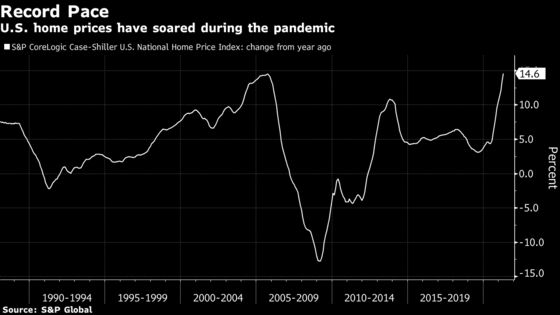

Unprecedented cash payments by the U.S. government to households, record-low mortgage rates and changing consumer preferences have conspired to fuel a pandemic boom in housing. The S&P CoreLogic Case-Shiller U.S. National Home Price Index rose 14.6% in the 12 months through April, according to the latest available numbers, marking the fastest pace of increase on record in data from 1988.

The surge is dividing the central bank’s policy-setting Federal Open Market Committee into two camps.

In one, “several participants saw benefits to reducing the pace of these purchases more quickly or earlier than Treasury purchases in light of valuation pressures in housing markets,” according to the record of the FOMC’s last policy meeting in mid-June.

“Several other participants, however, commented that reducing the pace of Treasury and MBS purchases commensurately was preferable because this approach would be well aligned with the committee’s previous communications or because purchases of Treasury securities and MBS both provide accommodation through their influence on broader financial conditions,” the meeting minutes said.

Fed-watchers are about evenly split on which path policy makers will choose, with slightly more than half expecting them to taper MBS purchases faster, according to results of a Bloomberg survey conducted July 16-21.

Fed Governor Christopher Waller and the presidents of the Boston, St. Louis, Kansas City and Dallas Fed banks -- Eric Rosengren, James Bullard, Esther George and Robert Kaplan -- have all suggested in recent public remarks that such a course of action may be appropriate.

“Right now the housing market is on fire. They don’t need any other unnecessary support so I would be all in favor of that,” Waller said in a June 29 Bloomberg TV interview of the proposal.

Fed Leadership

But some of the central bank’s top leaders -- including Powell -- don’t sound convinced. New York Fed President John Williams and Chicago Fed President Charles Evans have also emphasized in recent public comments that the central bank’s MBS purchases are not intended to support the housing market in particular.

“Mortgage-backed securities purchases really work a lot like Treasury purchases,” Powell told the House Financial Services Committee during a July 14 hearing. “They aren’t especially important in what’s happening with housing prices.”

Williams offered a similar view two days earlier, arguing while speaking with reporters that “both of them affect interest rates, therefore both of them affect the cost of housing.”

The thinking among Fed officials who favor a proportional tapering of Treasuries and MBS purchases goes like this, according to Markowska: The two securities are the most important assets in the U.S. financial system, and removing both of them from public portfolios through central-bank buying forces investors into other assets and drives down risk premiums across markets. That, in turn, reduces rates paid by mortgage borrowers.

MBS Impact

Evans lent support to that interpretation of the effects of the Fed’s MBS purchases as well, while speaking with reporters on July 15.

The MBS buying “has much larger effects throughout markets and the way markets are functioning,” he said, pointing to “fungibility with different types of liquidity and assets.”

But even if the hawks do get their way, it probably won’t have a big impact on house prices, Markowska said. With inventories so tight and builders facing temporary constraints on new construction related to availability of labor and materials, demand has already cooled from earlier in the year.

“The only way to relieve the pressure is for home builders to just create more supply,” she said. “That’s really not something that the Fed can do a whole lot about.”

©2021 Bloomberg L.P.