Fed Minutes Show Debate Emerges on When to Halt Rate Cuts

Fed Minutes Show Debate Emerges on When to Halt Policy Easing

(Bloomberg) -- Explore what’s moving the global economy in the new season of the Stephanomics podcast. Subscribe via Pocket Cast or iTunes.

Federal Reserve officials began debating how far their current interest-rate cutting campaign should extend, even as they agreed to lower rates in response to growing risks to the U.S. economy.

“Participants generally judged that downside risks to the outlook for economic activity had increased somewhat since their July meeting, particularly those stemming from trade policy uncertainty and conditions abroad,” minutes of the Sept. 17-18 Federal Open Market Committee meeting, released Wednesday in Washington, said.

In discussing policy beyond the September session, however, several officials made a push for the FOMC’s statement to signal the limits of the policy easing that Chairman Jerome Powell characterized in July as a “mid-cycle adjustment.”

“Several participants suggested that the committee’s post-meeting statement should provide more clarity about when the recalibration of the level of the policy rate in response to trade uncertainty would likely come to an end,” the minutes said.

“A possible base case for the Oct. 30 meeting is that the Fed will cut rates another 25 basis points, but then add language to the statement to signal that the bar for additional cuts is getting higher,” Roberto Perli, a partner at Cornerstone Macro LLC in Washington, wrote in a note to clients. “That would also be a way to address the obvious divisions inside the committee about the desirability and extent of future rate cuts.”

Michael Feroli, chief U.S. economist at JPMorgan Chase & Co. in New York, was more skeptical that Fed officials might soon put down such a marker.

“Between October and December you’re going to have two jobs reports, some Brexit developments, a lot of things can happen,” he said. “I don’t know that a day after October they want to put things on a pre-set course.”

At their September meeting, the FOMC lowered rates by a quarter percentage point for the second time this year. Powell described the move as providing insurance against risks threatening the economic outlook.

Rate Path

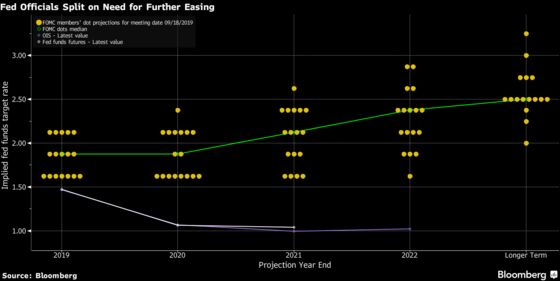

Projections on the best future path for rates, also released after that meeting, showed policy makers were divided. Five thought it was a mistake to cut rates, five agreed with the reduction and thought that would be enough this year, and seven favored another decrease by December.

The minutes again reflected concern over slowing global growth and uncertainty created by President Donald Trump’s trade disputes.

Participants showed increased concern about such risks, as well as geopolitical threats, judging that related uncertainty would continue to affect business investment spending.

“Several participants mentioned that uncertainties in the business outlook and sustained weak investment could eventually lead to slower hiring, which, in turn, could damp the growth of income and consumption,” the record of the gathering said.

Officials agreed consumer spending was increasing at a strong pace and household spending was likely to hold up, while several said the housing sector was starting to rebound as mortgage rates fell.

Nonetheless, several also noted that statistical models designed to gauge the probability of a recession over the medium term had increased notably in recent months.

Soft Data

Economic data released since the meeting has been soft. Closely watched reports on manufacturing, services and payrolls all came in weaker than expected, though hiring was still enough to push the U.S. jobless rate down to a half-century low of 3.5%.

Powell sounded non-committal Tuesday on the need for another cut in October, describing the economic outlook as “favorable” but threatened by risks connected to trade and slowing global growth.

“The next FOMC meeting is several weeks away, and we will be carefully monitoring incoming information,” he said in Denver. “We will act as appropriate to support continued growth, a strong job market, and inflation moving back to our symmetric 2% objective.”

The FOMC also discussed recent turmoil in overnight money markets, where a sudden lender shortage caused rates to spike higher, and briefly pushed the benchmark federal funds rate above the Fed’s target range.

Permanent Fix

The strain forced the Fed to intervene with temporary injections of liquidity for the first time in a decade to tamp down rates. The committee discussed a more permanent version of that program.

“Several participants suggested that such a discussion could benefit from also considering the merits of introducing a standing repurchase agreement facility as part of the framework for implementing monetary policy,” the minutes said.

Critics linked the turmoil with the reduction in the size of the Fed’s balance sheet, which they said left the system with insufficient bank reserves to cushion the market from periods of higher cash demand or lower supply.

Powell said Tuesday the central bank will resume growing its balance sheet via new asset purchases, probably Treasury bills, to insure a sufficient quantity of reserves. He also stressed the move was to solve “technical issues” and shouldn’t be confused with crisis-era large-scale bond buying, also called quantitative easing, designed to stimulate the economy.

--With assistance from Kristy Scheuble.

To contact the reporter on this story: Christopher Condon in Washington at ccondon4@bloomberg.net

To contact the editors responsible for this story: Margaret Collins at mcollins45@bloomberg.net, Jeff Kearns, Alister Bull

©2019 Bloomberg L.P.