Fed Looks Likely to Consider Faster Drawdown in Asset Purchases

Fed Looks Likely to Consider Faster Drawdown in Asset Purchases

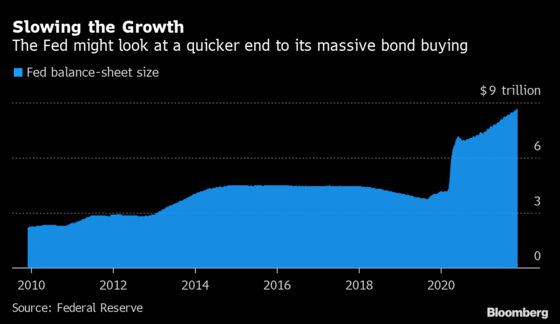

(Bloomberg) -- The Federal Reserve looks on course to consider a more rapid drawdown of its mammoth bond-buying program just weeks after it instituted a plan to scale the purchases back in a methodical manner.

A trio of policy makers -- Vice Chairman Richard Clarida, Governor Christopher Waller and St. Louis Federal Reserve Bank President James Bullard -- signaled this week that the topic of a faster taper might be on the table when the Federal Open Market Committee meets Dec. 14-15.

“I’ll be looking closely at the data that we get between now and the December meeting,” Clarida said Friday. “It may well be appropriate at that meeting to have a discussion about increasing the pace at which we are reducing” our asset purchases.

He told a San Francisco Fed conference that the U.S. economy is in a “very strong position” and that there is an “upside risk to inflation.”

A faster reduction in the so-called quantitative easing program would give policy makers an earlier opportunity to lift interest rates from near zero should they deem that necessary to keep the economy from overheating. Officials have vouchsafed a reluctance to raise rates and tighten credit at the same time they’re pumping money into the economy though bond buying.

It was just over two weeks ago that the FOMC announced it would start slowing its $120 billion of monthly asset purchases at a steady pace that puts it on track to finish the process by mid-2022.

But the economic data released since then have surprised in a hawkish direction, said JPMorgan Chase & Co. Chief U.S. Economist Michael Feroli.

Consumer prices skyrocketed by 6.2% in October from a year earlier, led by cars, food, gasoline, electricity and fuel oil.

| Read more: |

|---|

|

The jobs market also surprised to the upside. Nonfarm payrolls increased by 531,000 last month after September’s 312,000 gain, while the unemployment rate fell to 4.6% from 4.8%.

“The risk of accelerating the taper at the December meeting has risen,” said Brett Ryan, senior U.S. economist at Deutsche Bank Securities Inc. “The latest inflation data has caused policy makers to reevaluate their inflation outlook and the December discussion will certainly be more in depth on tapering.”

Feroli, for his part, doubts that the Fed will opt to speed up the reduction in its asset purchases, though he said it could be persuaded to do so by unexpectedly outsized gains in payrolls in the months ahead.

Stephen Stanley, chief economist at Amherst Pierpont Securities LLC, agrees that a December taper decision is unlikely. Unlike Feroli, though, he sees the Fed eventually deciding to speed up the drawdown, perhaps at its meeting in late January.

“They’re open to the possibility that they’re going to need to kick the normalization process into a faster gear,” he said.

Barkin, Kashkari

Not all policy makers are pushing for speedier action. Richmond Fed President Thomas Barkin said the central bank can be “patient” in assessing the taper and “it’s very helpful for us to have a few more months to evaluate.” Minneapolis Fed President Neel Kashkari said, “We shouldn’t overreact to what is likely going to be a temporary factor.”

After the Fed announced the start of its pullback earlier this month, Chair Jerome Powell suggested that the central bank would give investors a head-up before deciding to change the speed of the drawdown.

“We wouldn’t want to surprise markets,” he told reporters on Nov. 3. “We’ll say, ‘In light of this factor or these factors, we are considering doing this,’ and then we would either do it or not do it.”

Any discussion about quantitative easing in December could be complicated by a coming changing of the guard at the Fed board. Clarida’s tenure as a board member is up on Jan. 31, while Randal Quarles, the vice chair of supervision, has said he will leave the Fed by the end of the year.

More importantly, Powell’s four-year term as Fed chair ends in February. President Joe Biden has yet to decide whether to nominate Powell for another term, or tap Fed Governor Lael Brainard to replace him. A decision could come next week.

Little Difference

Many Fed watchers say there’s little difference between Powell and Brainard when it comes to monetary policy, though on the margin Brainard is considered slightly more dovish and inclined to stick with an ultra-easy policy for longer.

The Fed has had difficulty calibrating its asset-purchase programs going all the way back to when it first instituted them in 2008 during the financial crisis. In 2013, for instance, then-Chairman Ben Bernanke triggered a surge in long-term interest rates with the mere suggestion that the Fed might begin to scale back its bond buying -- the so-called taper tantrum.

The anomaly this time is that, by continuing to buy assets, albeit at a reduced rate, the Fed is pumping money into the economy at the same time that inflation is climbing at a pace well above its 2% target.

“It is pretty remarkable” that the central bank is still adding monetary stimulus when consumer prices are rising by more than 6%, former New York Fed President William Dudley told Bloomberg Television on Nov. 15.

“There is a case to be made for accelerating the taper,” said Dudley, an opinion columnist for Bloomberg, a senior adviser to Bloomberg Economics and a senior research scholar at Princeton University.

©2021 Bloomberg L.P.