(Bloomberg Opinion) -- Almost exactly nine months ago, Fed Governor Lael Brainard gave a speech titled “Navigating Monetary Policy as Headwinds Shift to Tailwinds.” Her gist was that the Federal Reserve needed to “be ready to adjust the path of policy” with the prevailing winds.

Now the winds are shifting again, perhaps sooner than she or her colleagues anticipated. Adjusting Fed policy in response — in particular, by ending or delaying its steady interest-rate increases — would be entirely consistent not only with Brainard’s speech but also with the data-dependent framework that Fed officials have repeatedly outlined over the past year.

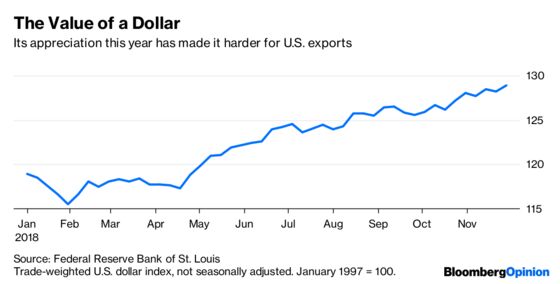

Let’s consider how each of the factors Brainard mentioned last March have changed. First, there is the international picture. Brainard noted that the International Monetary Fund had just raised its forecast of global growth and that major currencies were appreciating against the dollar. A rise in prices for imports was a real possibility.

In the following months, however, growth abroad has been consistently disappointing. Investor expectations of growth in the Euro area are now as low as they’ve been since the 2012 European debt crisis, and the IMF is warning that the U.S. will not be able to escape the effect. Consequently, the dollar has appreciated significantly since March and could appreciate further.

Second, Brainard explained that higher oil prices were contributing to higher investment spending in the U.S. The so-called accelerator effect has been particularly strong in the U.S. oil industry. Over the last few years, capital expenditure in the U.S. has been more closely associated with oil prices than with any other factor.

When Brainard spoke, both the price of oil and capital expenditure in the industry were rising. Expenditures have since stalled out as the oil rally has slowed, and it’s a safe bet that they will be falling over the next few months in response to oil’s recent collapse.

Third, Brainard mentioned higher stock prices and implicitly their tendency to increase both consumer and business spending.

Evaluating whether stocks are “too high” is always a tricky business. What is clear, however, is that major indexes around the world have fallen significantly over the past few months and are continuing to fall, and have been accompanied by a fall in bond yields. This suggests retrenchment on the part of households and businesses.

Last, Brainard mentioned how tax reform would boost the economy. That boost was significant, and has kept the U.S. from faltering as much as Europe in the last few quarters. But the boost from tax reform will fade next year, and the U.S. will be as exposed as the rest of the world.

All the factors that would have counted as tailwinds at the beginning of the year are now becoming headwinds. It’s utterly consistent for the Fed to adjust policy in view of these changing conditions. By responding to symmetrically to the risks in the economy, the Fed should give investors increased faith in its commitment to sound monetary policy — and, in the long run, enhance its credibility.

To contact the editor responsible for this story: Michael Newman at mnewman43@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Karl W. Smith is a senior fellow at the Niskanen Center and founder of the blog Modeled Behavior.

©2018 Bloomberg L.P.