Fed Fires Warning Shot at Wall Street's Riskier Loan Deals

Fed Fires Warning Shot at Wall Street's Riskier Loan Deals

(Bloomberg) -- In the Trump era, Wall Street banks have been testing the limits of what they can get away with in piling risky loans onto highly indebted companies. They may have finally crossed a line.

A top Federal Reserve official fired a rare public warning Wednesday, saying that banks appear to be chasing increasingly dangerous deals and forgoing protections against borrowers going bust.

“There may be a material loosening of terms and weaknesses in risk management,” Todd Vermilyea, the Fed’s head of risk surveillance and data, told bankers at a conference in New York. “Some institutions could be taking on risk without the appropriate mitigating controls.”

The warnings come after watchdogs have spent most of the year expressing confidence about the health of the $1.3 trillion market for leveraged loans. They acknowledged that some firms were putting together transactions that were risky by the standards of just a few years ago, but said it was happening outside the tightly regulated banking sector, thus mitigating threats to the financial system.

For now, the Fed might not be doing much more than waving caution flags. Federal regulators have made clear in recent months that banks aren’t likely to face punishments for financing risky loans.

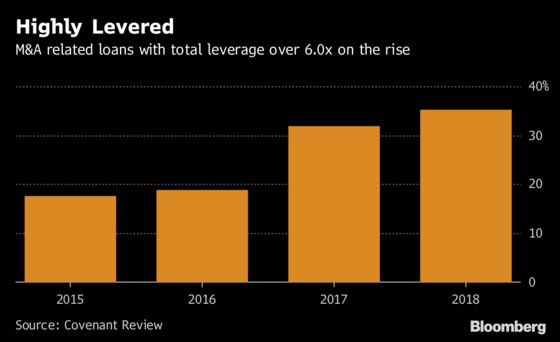

Higher Leverage

What changed? Deals like one from September in which underwriters including Citigroup Inc., Morgan Stanley and Goldman Sachs Group Inc. joined KKR Capital Markets in arranging $6.7 billion of loans and bonds in the buyout of Envision Healthcare Corp.

That saddled Envision with a debt load that was around seven times a measure of its earnings, a level well above the six times limit that regulators offered as guidance for banks in 2013. More and more loans are leaving borrowers with debt above that limit.

Loosening regulation of Wall Street has been a central theme in Washington under President Donald Trump. On leveraged lending, the industry got an assist last year when regulators had to step back from the 2013 guidelines, which had driven a number of transactions to nonbank lenders.

At the prodding of Republicans in Congress, the Government Accountability Office reviewed the guidance and determined that the Fed and other agencies had overstepped their authority and needed congressional approval for it to be a rule.

Following the decision, Comptroller of the Currency Joseph Otting said banks could do as much leveraged lending as they wanted provided they had sufficient capital to offset the risks, and it doesn’t impair their soundness. Just last week, Otting said the banking industry had “really kind of stayed on the rails” and that private-equity firms were doing the riskiest leveraged lending.

‘Dumb Things’

“There is a case to be made that if a bank knows what it is doing, understands the risks, and is holding appropriate capital, they should be able to take the risks they want to take,” said Tim Clark, a former senior supervisor at the Fed who helped manage the central bank’s stress testing of the largest banks after the 2008 financial crisis.

“But as we learned during the crisis, it’s hard to overstate the capacity of banks to do dumb things, especially when there is a lot of money to be made from trying to keep the party going,” he added.

Vermilyea’s remarks indicate the Fed isn’t as comfortable as Otting with the state of the market. The Fed official cited three particular areas of concern:

- A proliferation of loans with weak covenants, which are meant to protect creditors if borrowers run into trouble.

- Terms known as incremental facilities that layer additional debt onto an existing loan.

- Loan adjustments known as “add-backs” that make borrowers’ profits appear better, which could overstate their ability to repay loans.

So-called covenant-lite loans, which were once rare, now make up about 80 percent of the market. Incremental facilities are being added to loans at a record pace this year. Companies are making ever-rosier earnings assumptions, which allow them to heap on more debt. About 38 percent of the earnings figures used to calculate leverage in acquisition-linked loans this year were made of add-backs, according to research firm Covenant Review. That’s up from 10 percent in the first quarter of 2015.

Despite Vermilyea’s warnings, there may not be a hammer behind it. Agency heads appointed by Trump, including Fed Chairman Jerome Powell, have said they won’t use their 2013 guidance to justify sanctions against banks.

The regulatory environment can be likened to having a speed limit “but no police enforcing it,” said Anat Admati, finance and economics professor at Stanford University Graduate School of Business.

--With assistance from Lara Wieczezynski and Larry Reibstein.

To contact the reporters on this story: Lisa Lee in New York at llee299@bloomberg.net;Jesse Hamilton in Washington at jhamilton33@bloomberg.net;Sally Bakewell in New York at sbakewell1@bloomberg.net;Craig Torres in Washington at ctorres3@bloomberg.net

To contact the editors responsible for this story: Jesse Westbrook at jwestbrook1@bloomberg.net, ;Nikolaj Gammeltoft at ngammeltoft@bloomberg.net, Dan Wilchins

©2018 Bloomberg L.P.