Mortgage Industry Roars to Record Year, Courtesy of the Fed

Mortgage Industry Roars to Best Year Ever, Courtesy of the Fed

(Bloomberg) -- The Federal Reserve has handed U.S. mortgage lenders their best year ever. Nobody knows that better than Shant Banosian, the industry’s first billion-dollar salesman.

By his own count, the loan officer is personally set to originate a staggering $1.5 billion of home loans by year’s end from his office outside of Boston, a record in a year of records for the mortgage business.

Set alight by the Fed’s low interest rates and bond purchases, the mortgage industry is on fire. Lenders this year are projected to originate $4.1 trillion of loans, eclipsing the 2003 high, thanks mostly to borrowers refinancing to reduce their house payments, according to Fannie Mae.

With profit margins the widest on record, mortgage lenders are on a hiring spree and taking advantage of the pandemic housing boom to raise money from investors. At least nine have either gone public this year, such as Rocket Cos., or are planning to do so in coming months.

But like all booms, this one won’t last forever. By next year, mortgage volumes could decline by a third as refinancings drop, according to a Fannie Mae forecast. Even if rates stay flat, the number of homeowners motivated to lock in savings will decline.

“Today’s market is like riding a giant rollercoaster -- the higher it goes, the more dramatic the decline,” said Jim Cameron, senior partner with STRATMOR Group, a mortgage advisory firm based in Greenwood Village, Colorado. “You could argue, when you know the rates will eventually turn and you’ll lay a bunch of people off, why hire? But quite frankly, the profits are there now.”

Recruiting Fight

For now, the industry is adding staff to handle all the business. Recruiters are in an all-out “firefight,” Cameron said. Firms are offering signing bonuses to steal underwriters and processors from competitors or giving retention payments to keep them from leaving.

Lenders increased their headcount by 25% in July and 40% in August on an annualized basis, according to Bank of America researchers. Figures from the Bureau of Labor Statistics suggest there are now more than 100,000 mortgage brokers in the U.S., the first time it’s cracked six figures since 2007.

Banosian, who runs a branch for Chicago-based Guaranteed Rate, increased his staff by half to 40, just to keep up with the flood of applications from buyers upgrading to bigger suburban homes or saving a bundle by refinancing. Nationally, the company is advertising more than 400 open positions on its website.

“I presume rates will remain low next year,” Banosian, 40, said in an interview, alone in his 4,000-square-foot office in Waltham, Massachusetts, while his employees work remotely. “We’re planning to staff up.”

$1 Billion

Last year, Banosian originated a record $916 million in mortgages, according to Scotsman Guide, which began producing its rankings in 2009. This year, he says he reached $1 billion in September. He expects to make 3,000 loans this year under his name, totaling at least $1.5 billion. And he plans to expand to other states.

Guild Holdings, which focuses on providing mortgages to homebuyers, sold shares to the public in October and wants to expand its business in Florida, the northeast and across the center of the country, Guild Chief Executive Officer Mary Ann McGarry said in an interview. And they’re staffing up quickly.

United Wholesale Mortgage, the nation’s largest lender for mortgages initially handled by brokers, now employs more than 7,000 people, up by about 40% from last year. NewDayUSA, a mortgage lender that focuses on veterans, has nearly doubled its workforce since March with plans to grow even more in the coming months, CEO and founder Rob Posner said in an interview.

Big Margins

While mortgage rates have never been this low, they could be lower. Most loans are sold and then packaged into bonds. The Fed has bought more than $1.3 trillion in mortgage bonds since March, driving up prices and enabling lenders to sell their loans at a hefty premium. Lenders say that to avoid being overrun with business they’ve kept rates elevated, padding profits.

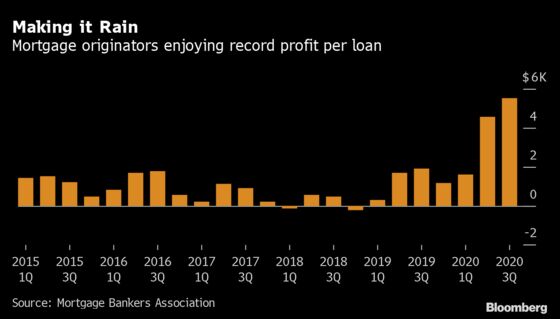

The average lender originated $1.34 billion of mortgages in the third quarters, up 33% from the prior three months and as much as a typical company would produce in a year, said Marina Walsh, vice president of industry analysis at MBA. The profit-per-loan in the third quarter hit a record $5,535, up 22% from three months earlier, the Mortgage Bankers Association said Thursday.

Different Story

Next year may tell a different story, depending on the pandemic. A successfully deployed vaccine might bring back a semblance of normality to the economy. If employment recovers, that could push more people in the housing market. But if rates climb, even slightly, that could snuff out the refinancing boom.

“By any stretch it will be a good year,” said Doug Duncan, chief economist at Fannie Mae.”This year is just out of the park.”

Fannie Mae, which projects borrowing costs to remain flat, said mortgage volumes for home purchases will grow by about 4% next year. That won’t make up for an expected plunge in refinanced loans to $1.1 trillion next year from $2.6 trillion in 2020.

So far, lenders haven’t run out of consumers who can refinance. There are still nearly 20 million homeowners out there who could shave about $300 on average off their monthly mortgage payment at today’s rates, according to Black Knight Inc.”

But if refinancings drop as predicted, lenders will be looking to homebuyers to make up the difference. And that will depend on the strength of a housing market that has been running hot, pushing prices out of reach for some Americans.

“The Fed has delivered a windfall to the mortgage industry,” LendingTree Chief Economist Tendayi Kapfidze said. “But demand from borrowers is going to be less. The low hanging fruit is gone.”

©2020 Bloomberg L.P.