FAANGs Pushed on a String and Guess What Happened?: Taking Stock

FAANGs Pushed on a String and Guess What Happened?: Taking Stock

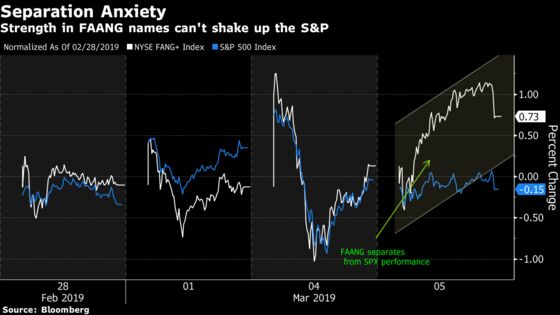

(Bloomberg) -- Lost in the narrative of the direction-less S&P has been the participation of a group of stocks that used to drive the bus. They got back in the driver’s seat Tuesday, to no avail.

The NYFANG index outperformed the greater market, while the Communications services sector, which includes some of the largest FAANG names (with the exception of the also rising Amazon), almost single-handedly prevented the S&P from doubling its losses on the day. This happened even as a high-profile investor in Dan Niles came out publicly to shoot down on one of the FAANG constituents, Netflix, on CNBC amid a dearth of new news. But even their hefty market weights weren’t enough to push the market higher. The OECD out cutting the global growth outlook this morning (just a few months from the last time they trimmed forecasts) isn’t helping the prospects for today either (and some cautious trade commentary from the China Commerce minister), with futures off 5 handles.

The strategists, too, are apathetic on the rudderless ship. JPMorgan’s Dubravko Lakos-Bujas wrote in a note earlier in the week that the S&P valuations are "less compelling" than they were in early 2019, and now are closer to their historical average. Janney called it a "market stall," while they’re closely watching the small cap Russell 2000 (which has led the S&P this year) for a break of 1600 to confirm progress within the other benchmarks. In my view, the ECB rate decision Thursday and the nonfarm payrolls report on Friday can’t come soon enough. ADP data later this morning could provide a jolt, while the Beige Book commentary (some of the freshest contextual info the Federal Reserve can provide) this afternoon can firm up the outlook in recent weeks from the FOMC’s latest growth forecasts.

How about a 230% Return?

There are returns out there, and if the Communication Services (which was the second worst performer in the S&P over the past month) example above is any guide, money is sloshing around, though not enough to generate momentum in any particular direction. Pseudo-cult name The Trade Desk has not suffered from this ailment given its more than 200 percent return over the past year. The advertising technology player’s second analyst day as a publicly traded entity is due later today, and its status as a top 5 performer in the Nasdaq over the past 10 months should warrant some attention. It has come off its highs set last week and recently reported results, so most of the commentary should revolve around furthering that narrative. RBC analysts earlier this week laid out their top 10 questions, which revolve around Connected TV, expansion in China, and profitability trends, to name a few.

CRAZY POPS

And similar to the above, single stocks still exhibit opportunities, like when tobacco names such as Altria and Philip Morris spiked (and the rest of biotech fell) on the reports the FDA commissioner was due to resign (a vocal opponent of e-cigarettes and vaping while a general supporter of faster drug approvals).

GE shares went crazy during the JPMorgan conference, when the CEO surprised the market with a negative free cash flow forecast in the industrials segment. Gordon Haskett analysts were quick to raise the prospects that the industrial conglomerate runs the risk of debt rating cuts.

And then there were the homebuilders, which, despite bucking much of the flat to downward trend of the past couple sessions, succumbed to weaker home sales data which pointed to falling home prices. Housing stocks like LEN, PHM and suppliers like LOW, MHK underperformed. Building products firm Quanex however, reported better than expected results late Tuesday.

Teen-y Moves

For the success that Target and Kohl’s emulated early Tuesday, Ross Stores and Urban Outfitters failed to deliver in the post-market -- on both excitement (both are likely to hand a win over to the straddle buyers if the moves hold) and performance (ROST missed on comps while URBN’s forecasts appeared light). KeyBanc wrote that URBN "saw weakening 4Q trends," similar to other retailers, though they are unclear as to the cause.

Today also brings results from a discounter (though Dollar Tree is a different animal than ROST) and more teen apparel names. American Eagle results might bring more fireworks, due post-market today with options implying a 10% move around earnings. Abercrombie and Fitch is due shortly, with larger than normal volatility expected there as well. Dollar Tree’s results are a bit complicated coming off fresh activist investor interest from Starboard. Wells Fargo analysts expect "fundamental weakness" and risk surrounding its 2019 guidance, but will mostly be focusing on whether there are hints of adjusting price structures or its plan for Family Dollar.

Sectors in Focus Today

- Chinese tech names (CTRP, HUYA, IQ, YY) after QTT gave up its substantial regular session gains in the post market following its results

- Auto parts, transmission and after-market suppliers (CON GY, EO FP, BWA, ADNT, LEA) after Germany’s Schaeffler AG announced job cuts, abandoned earnings targets, citing a challenging auto business and global growth

- Semiconductor names like ADI, CY, ON, MXIM after MCHP narrowed its guidance, citing in-line business conditions (read: things aren’t getting worse for the segment that had been plagued earlier in earnings season from slowdown worries); Citi "still" believes this quarter marks the bottom

- Retail following TGT and KSS blow out results and ROST’s disappointment post market

- Risk, consulting and insurance names (AJG, MMC) after Aon confirms it is not pursuing a deal with Willis Tower

Notes From the Sell Side

A four-day slaughter in Intelsat was enough to bring out the bulls and the bargain hunters. Raymond James upgraded the stock to market perform, writing that while it still had “many questions” about a plan to allow satellite companies to sell their spectrum in the C-band, shares “more appropriately reflect” the company’s prospects. Separately, Cowen affirmed its outperform rating (and $50 price target -- nearly triple Tuesday’s close), arguing that “the fundamental picture around a potential spectrum monetization event has not materially changed,” even if “risks and uncertainties remain.” Pre-market volume was light, but the bid/ask implies Intelsat could halt its recent downtrend.

Electric-vehicle maker NIO Inc. which lowered its shipment forecasts for both 2019 and 2020 was also cut to underperform at BofAML this morning . The move was partially related to Tesla’s recent price-cut announcement, which analyst Ming Hsun Lee expects will intensify competition, but the firm also cited a refinancing risk. “If there is a slowdown in volume sales growth, NIO will need more cash to finance its working capital and capex plan,” BofAML wrote, pushing back its timeline for when free cash flow will turn positive by a year to 2023.

Tick-by-Tick Guide to Today’s Actionable Events

- GTHX investor day

- JPMorgan Aviation, transportation and industrials conference (KSU, UNP, ECL)

- Citi Global Property CEO conference (TIER, HCP, UDR, REG, IRM)

- 7:00am -- MBA Mortgage Applications

- 7:30am -- DLTR earnings

- 8:00am -- MRNA earnings call; XOM investor day

- 8:15am -- Feb ADP Employment Change

- 8:30am -- Dec Trade Balance

- 8:30am -- ANF, BJ earnings call; EL investor day

- 9:00am -- DLTR earnings call

- 10:00am -- Bank of Canada Rate decision

- 10:00am -- BF/B earnings call

- 12:00pm -- Fed’s Williams speaks to the Economic Club of New York; Fed’s Mester participates in a moderated discussion

- 1:00pm -- TTD investor day

- 1:15pm -- Fed’s Williams visits Puerto Rico

- 1:30pm -- QLYS investor day

- 2:00pm -- U.S. Federal Reserve Releases Beige Book

- 4:00pm -- AEO earnings

- 4:15pm -- AEO earnings call

--With assistance from Ryan Vlastelica.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.