(Bloomberg Opinion) -- The most telling line in a new activist letter urging Exxon Mobil Corp. to embrace environmental sustainability has nothing to do with sustainability:

Whatever the level of future [oil and gas] demand growth may be, ExxonMobil has no obligation to spend aggressively if doing so is likely to deliver suboptimal returns.

Engine No. 1 LLC, the new fund targeting Exxon, has the backing of the California State Teachers’ Retirement System, with stakes adding up to about 0.2% of the market cap. So this is like a speedboat taking on a supertanker. What makes it noteworthy is that Exxon effectively fashioned the weapons the activist is now brandishing against it.

“Discipline” is almost a cliche when it comes to talking about Exxon. Or it was, anyway. As I wrote here last week, while Exxon's operational excellence remains solid, a series of strategic missteps capped off by an upcoming multi-billion dollar write-down have undermined the company’s reputation for judicious spending. And that has destroyed its long-standing premium to other oil majors. The supertanker has taken on water.

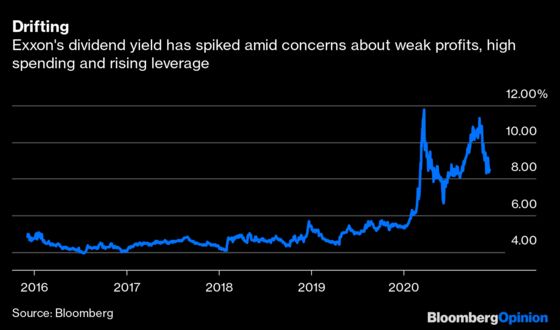

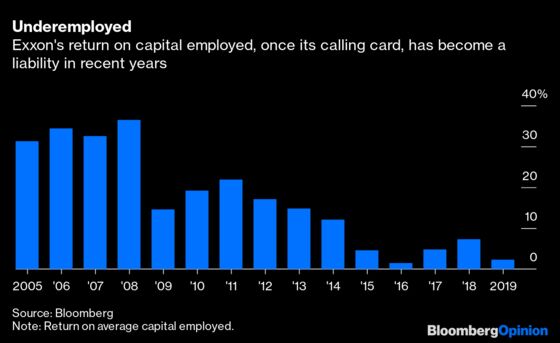

That’s why the activist leads off not with a diatribe about emissions or melting ice-caps, but something more prosaic: weak shareholder returns, falling return on capital employed, rising debt and indifference to the stock. These are likely to resonate with fund managers because they are focused on (a) the stock’s performance and (b) exactly the sort of thing Exxon used to boast about in better times. Return on capital employed, in particular, owes much of its prominence in oil-major analysis to Exxon’s proselytizing on Wall Street in the 1980s and ‘90s .

Despite those dismal numbers, and falling stock price, Exxon persisted with a high-spending strategy to develop new oil and gas assets until the Covid-19 crisis forced cutbacks. Explicit in the strategy is Exxon’s position that peak-oil demand concerns are overblown. Implicit is the need for higher oil prices in the near term to shore up the company’s return metrics and all-important dividend. Hence, Engine No. 1's line about Exxon not being obligated to spend aggressively, peak demand or no, hits home.

The fact the activist led with this straightforward jab speaks to the difficulty inherent to landing the other punch: namely, getting Exxon to look beyond oil and gas. The argument here is essentially one about the potential for stranded assets, with Exxon’s terminal value pressured by weaker long-term oil demand than the company factors in now. The upcoming asset write-down, centered on Exxon’s North American shale strategy, is a powerful counterargument against Exxon simply knowing best.

It is notable that the letter mentions BP Plc’s nascent pivot toward renewable energy, but as an example to avoid rather than emulate (BP’s stock has performed even worse than Exxon’s this year). Rather than demanding Exxon immediately start buying up solar farms, Engine No. 1 calls for a strategic rethink to determine what energy transition strategies might make sense for a company with this much expertise and resources, backed up with new board members with relevant experience.

Even if the target is notable, in activism terms, these are baby steps — necessarily so when we’re talking about Exxon — designed to nudge bigger players to act. At the beginning of this year, BlackRock Inc.’s Larry Fink caused a stir with a letter warning capital markets will shift faster than many expect when it comes to climate change, and that companies should plan accordingly. As I wrote at the time, when it comes to the oil sector, reforming the pay incentives and benchmarking that have long encouraged growth over returns would go a long way in terms of restoring investors’ interest — and simultaneously help address the environmental excesses associated with undisciplined spending. In this sense, Engine No. 1’s gambit is as much a test for Fink as it is for Big Oil. And regardless of how this campaign fares, it should not be lost that Exxon’s own stumbles, and on familiar ground rather than sunlit uplands, created the opening.

See chapter two of "Private Empire: Exxon Mobil and American Power" by Steve Coll (Penguin Random House, 2013).

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2020 Bloomberg L.P.