Europe’s Frothy Junk Bond Deals Ring Alarm Bells for Investors

Europe’s Frothy Junk Bond Deals Ring Alarm Bells for Investors

(Bloomberg) -- Europe’s junk bond market is showing signs of froth as companies take advantage of demand to increase borrowing and weaken investor protections.

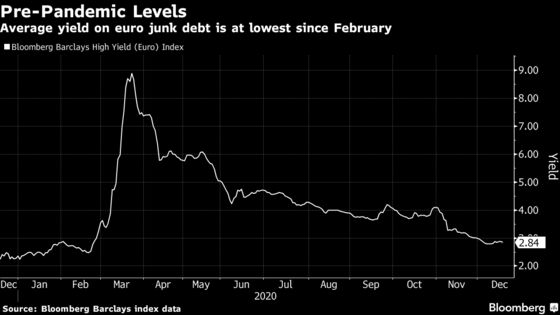

Companies have sold 5.5 billion euros ($6.7 billion) of high-yield notes so far this month, 68% more than all of last December, according to data compiled by Bloomberg. Central bank purchases have contributed to demand, driving average borrowing costs to the lowest since February, Bloomberg Barclays index data show.

French supermarket chain Casino Guichard-Perrachon SA, Italian machinery maker Industria Macchine Automatiche SpA and luxury British carmaker Jaguar Land Rover Plc are among companies that increased the size of their deals this month. While nothing in Europe has gone as far as Blackstone Group Inc.’s limit on investor voting power in a U.S. transaction last month, bond buyers are concerned it’s a slippery slope.

“It’s difficult for investors to push back on risky covenants,” said Mark Benbow, a fund manager at Aegon Asset Management in Edinburgh. “There is insatiable demand for high yield right now.”

This week, budget hotel chain Travelodge and debt collector Lowell, which both struggled through the pandemic, placed bonds privately. Travelodge’s 9% notes were priced at 96% of face value.

Casino upsized and tightened pricing on its first bond sale in a year, without securing the notes with assets as in its previous deal. Analysts at research firm Lucror Analytics described the transaction as opportunistic and said they have “mixed views on the documentation” because it lacks guarantees and has looser clauses than the retailer’s secured bonds.

The documentation includes a “strong covenant package,” which investors didn’t push back on during the roadshow, according to a Casino spokesperson.

IMA upsized a bond deal last week that analysts said was particularly aggressive. While borrower-friendly documentation is typical for debt-funded leveraged buyouts, IMA’s deal included several “non-standard” provisions: the call protection period was an unusually short two years and owners will be able to transfer value from the company, even in the case of a default.

Jaguar also increased two bond deals in as many months, seizing the opportunity to raise cash just days before the Brexit transition period ends.

Growing Fears

Investors are also concerned that private equity firms will bring aggressive new U.S. bond terms to Europe, as they have in the past.

In a $1.2 billion bond offering to fund its buyout of Ancestry.com Inc. last month, Blackstone limited any single investor’s voting power to 20% of outstanding notes. That could make it harder for holders to push back on any attempt to change terms or to declare events of default, such as for missed interest payments.

Investor lobby group European Leveraged Finance Association spoke out against the provision, calling it “an inappropriate curtailment of investor rights” and “an attack on the very foundational principles that have come to define modern capital markets.”

Even so, buyers demanded more than $8 billion of Ancestry’s bonds, allowing it to lower yields.

A spokesperson for Blackstone declined to comment on its terms.

“Once the door opens to this sort of thing you can effectively bring down the cap to anything you want,” said Aegon’s Benbow, referring to the potential for similar terms to crop up in future deals.

Last year, Blackstone brought U.S. language to its buyout of U.K. theme park operator Merlin Entertainments, preventing investors with ‘net short positions’ from voting on amendments, waivers or default notices.

“There aren’t many covenants that disappear once they’ve successfully made it into that first deal,” said George Curtis, a credit analyst at TwentyFour Asset Management in London. “After the first deal happens, the banks start to call certain covenants market-standard pretty quickly.”

©2020 Bloomberg L.P.