Europe's Traders Throw in the Towel in Race With Wall Street

Europe's Banks Say Goodbye to Trading Dreams as U.S. Pulls Away

(Bloomberg) -- Europe’s investment banks are dropping out of the race for trading dominance.

A decade after the financial crisis, firms that had spent years pursuing the U.S. heavyweights are cutting jobs and allocating less capital to the business of trading securities. They’re all but throwing in the towel on a key piece of investment banking after yet another year in which their trading divisions failed to keep up with their American rivals.

“The battle is lost” for Europe’s investment banks, Jean-Pierre Mustier, a former derivatives trader who now runs UniCredit SpA, said last month in Brussels. “Commercial banking is the new derivative.”

As financial results for last year pour in, they show trading declined across the board at the large European firms, even as their U.S. rivals recorded gains. Deutsche Bank AG just posted the weakest trading result since the height of the financial crisis. At Credit Suisse Group AG, losses last quarter capped declines across equities and bonds. Even the French banks that until recently had singled out trading for growth are pulling capital and slashing jobs.

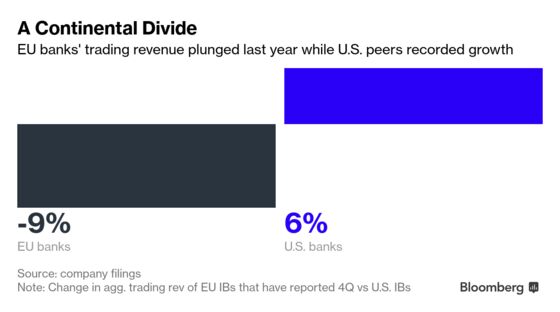

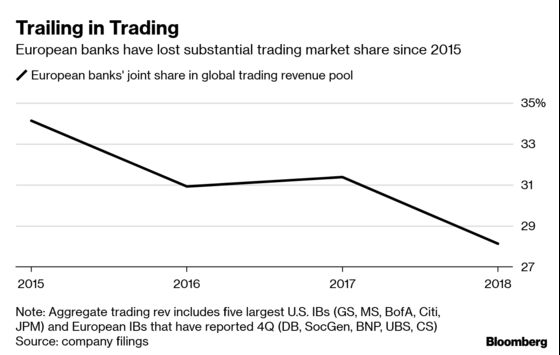

All told, the European firms saw their main trading businesses contract by more than 9 percent last year, and by more than a fifth compared with 2015, according to company filings. At the U.S. banks, trading revenue increased.

Europe’s bankers have complained for some time that structural disadvantages, such as new regulations, the lack of a single capital market and of a true banking union, are to blame for their decline, and Brexit is only making matters worse. Adding to those obstacles, Europe’s banks are still suffering from negative benchmark interest rates, which squeeze profitability in traditional corporate and retail banking.

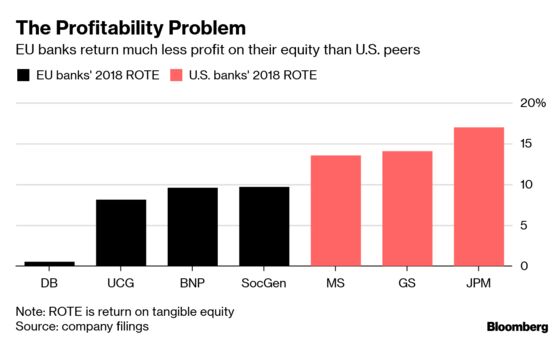

Wall Street, by contrast, just closed out its most profitable year ever, with the six biggest banks reporting more than $111 billion of profit for 2018. They’re buoyed by Republican tax cuts, rising interest rates, a surge in dealmaking and a retail banking boom. That’s allowing U.S. firms to invest in new technology to cement their advantage, including in trading.

For the Europeans, last year’s trading disaster caps a long retreat. Among the first to throw in the towel was UBS Group AG, which shut its Stamford, Connecticut, trading floor, one of the largest in the world, as part of a pivot to wealth management. Deutsche Bank and Credit Suisse held on to their large trading business longer, only to scale them back over the past few years.

With thousands of jobs gone, Europe’s trading units are now struggling to compete in the remaining areas. Deutsche Bank just posted its eighth consecutive quarter of declining revenue, led by its core fixed-income trading business. Chief Executive Officer Christian Sewing, who last year abandoned ambitions to be a top global securities firm, has yet to deliver on a promised to restore growth.

At Credit Suisse, a larger-than-expected loss of 193 million francs ($191 million) in the Global Markets business in the fourth quarter overshadowed the end of CEO Tidjane Thiam’s three-year turnaround plan. Thiam has cut back trading, winding down areas such as distressed debt after heavy losses, while emphasizing wealth management and the business in Asia.

Even firms bullish on their trading units until recently, such as BNP Paribas SA and Societe Generale SA, have announced steep cuts and lowered their profitability targets on the back of fourth-quarter results. BNP traders were flummoxed by market moves and a series of U.S. trades that lost millions. Natixis SA reported a 97 percent slump at its trading unit, after it suffered losses tied to esoteric stock trades in South Korea.

Jes Staley, who has bet his strategy on refocusing and bolstering the investment bank as CEO of Barclays Plc, was among the few Europeans outperfoming his U.S. peers in the third quarter, when fixed income trading jumped 10 percent. But several analysts have reduced expectations for that business in the fourth quarter, with Deutsche Bank’s David Lock now predicting a 15 percent decline. Barclays is scheduled to report earnings next week.

“The area where we have posted more disappointing results is the capital markets,” Frederic Oudea, Societe Generale’s CEO, said last week in explaining the planned cuts at his bank. There’s been “a change versus what we had in mind 12 to 15 months ago, in many aspects -- financial environment, economic environment, but also the regulatory framework.”

With an economic slowdown in the cards -- the EU Commission recently cut the bloc’s 2019 growth outlook --Europe’s loss in investment banking market share could be just the beginning.

“We see a moderate slowdown this year in overall sales and trading,” said Michael Rohr, senior credit officer for banks at Moody’s Investors Service. “The U.S. banks are better positioned in this scenario because they are more profitable and therefore have more money to invest. They also tend to be better at technology adoption.”

Mustier, who ran the first equity derivatives trading business at Societe Generale before joining UniCredit, is telling his new hires to focus on areas where European firms are better positioned. He has pledged to build a leading pan-European lender with a simplified structure, and has already exceeded plans for costs and asset quality.

“I created a very large derivative business when I was young,” said Mustier. “Today, I advise the new joiners of the bank to work on transaction banking and export finance.”

--With assistance from Fabio Benedetti-Valentini, Alexander Weber, Stefania Spezzati, Jan-Henrik Förster and Donal Griffin.

To contact the reporter on this story: Steven Arons in Frankfurt at sarons@bloomberg.net

To contact the editors responsible for this story: Dale Crofts at dcrofts@bloomberg.net, Christian Baumgaertel, Ross Larsen

©2019 Bloomberg L.P.