Euro-Area Prospects Tentatively Pick Up as German Orders Rebound

A gauge for business climate in the region showed a surprise improvement, manufacturing contracted less than initially reported.

(Bloomberg) --

Economic prospects for the euro area brightened slightly going into the fourth quarter, with strengthening private-sector momentum and an unexpectedly sharp gain in German factory orders suggesting a growth pickup ahead.

Since the 19-nation economy proved more resilient than anticipated in the third quarter to a barrage of risks ranging from trade tensions to Brexit, data have suggested the worst of its slowdown may finally be past. A gauge for business climate in the region showed a surprise improvement, manufacturing contracted less than initially reported in October and services activity accelerated somewhat faster.

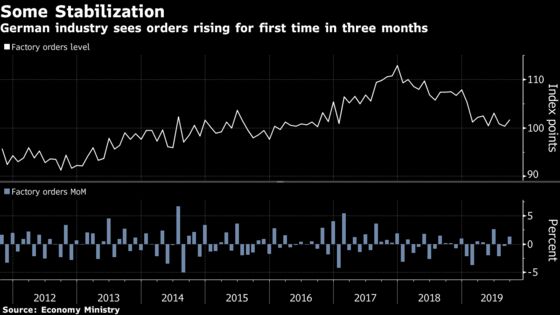

Germany’s Economy Ministry expressed cautious optimism that a 1.3% monthly increase in demand for German manufacturing goods and returning confidence “could signal a bottoming out of orders.”

But it’s much too soon to sound to sound the all-clear. The September report came with a somber reminder that demand was still down 5.4% from the previous year. The country probably went into a technical recession during the last quarter, and the labor market started to deteriorate.

What Bloomberg’s Economists Say

“Evidence corroborates the view that a floor is being reached. The business surveys have begun to stabilize after a precipitous decline this year. We therefore expect the economy to tread water in the fourth quarter before growth resumes at a slow pace in the first.”

--Jamie Rush. Read the GERMANY REACT

In Spain, industrial production contracted sharply in September, with a gauge for the whole private sector indicating weaker growth.

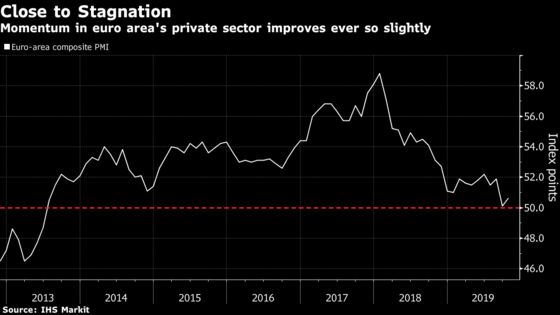

A composite Purchasing Managers’ Index for the euro area edged up to 50.6 in October, better than the flash reading of 50.2. Yet it still signaled a rate of growth that was among the weakest in six and a half years.

Exports slid for a 13th successive month with a rate of decline among the sharpest on record. That highlights how much is at stake for the region as the U.S. and China try to resolve a trade dispute that has taken its toll on global growth.

Falling order books in the region suggest that the “risks are currently tilted toward contraction in the fourth quarter,” said Chris Williamson, chief business economist at IHS Markit. “Worryingly, what little growth was seen in October was supported by firms eating into previously placed work.”

The continued frailty puts further pressure on governments to step up fiscal spending, a message pushed by former ECB President Mario Draghi before his term ended last week and expected to be continued by his successor Christine Lagarde. The central bank announced a contentious new monetary-stimulus package in September in an attempt to revive growth and inflation.

Yet governments have been reluctant, with Germany’s administration indicating that the situation has to deteriorate before significant aid will be unlocked. Finance Minister Olaf Scholz has said the economic situation doesn’t require a rushed fiscal response.

It’s a position shared by the government’s council of economic advisers, even as they warn the country is walking a tight line as an industrial recession threatens to drag down the broader economy. In its annual assessment of the economy, the group cut its growth forecasts for this year and next.

| Read more... |

|---|

|

--With assistance from Simbarashe Gumbo and Mark Evans.

To contact the reporter on this story: Yuko Takeo in Tokyo at ytakeo2@bloomberg.net

To contact the editors responsible for this story: Paul Gordon at pgordon6@bloomberg.net, Jana Randow

©2019 Bloomberg L.P.