EU’s Green Bonds Set to Preempt Rules That Will Govern Them

EU Green Bonds Set to Preempt the Rules That Will Govern Them

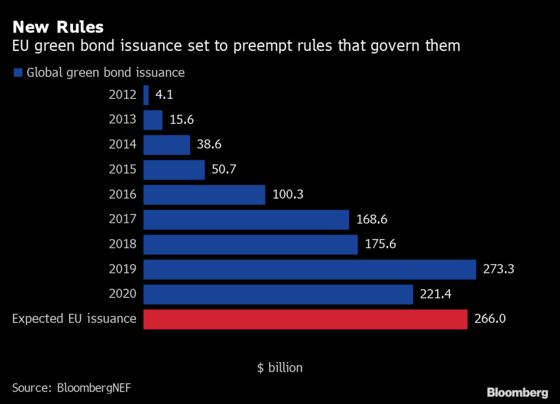

(Bloomberg) -- The European Union’s rush to finance its recovery from the pandemic means its first-ever green bonds may come before the standards meant to regulate them.

Until the bloc applies its so-called taxonomy for about 225 billion euros ($266 billion) worth of green debt and projects, the EU expects to use guidelines from the International Capital Markets Association and a second party when sales begin next year, said a senior European Commission official, who asked not to be identified because the information isn’t public. Those existing rules are less stringent than the EU’s draft standards.

“If we don’t seriously move towards taxonomy now, then you miss your chance and you’ll have a credibility problem,” said Bas Eickhout, a Dutch Green member of the European parliament. “You have the danger of greenwashing,” especially when recent plans from some countries “already read like business as usual.”

Member states are already starting to submit their budget plans for next year, with nearly a third of the bloc’s pandemic funds due to be financed by the green debt. The issue underscores the challenges the EU faces between getting recovery money to virus-ravaged economies quickly and becoming carbon neutral by 2050.

And given that the EU bonds and standards are slated to become global benchmarks for a rapidly-expanding $1 trillion market, without the taxonomy in place, there’s a risk of so-called greenwashing -- where environmental benefits are exaggerated or misrepresented.

The EU hopes to provide clarity in coming weeks on how expenditure will be linked to bond issuance under its Recovery and Resilience regulation, the European Commission official said. A spokesperson from the Commission declined to comment when reached by telephone.

The proposed green bond rules will require the debt to follow the EU’s taxonomy, as well as other criteria. The latest round of consultations concluded last month, and some expect decisions on next steps to be made by the Commission by the end of the year.

NatWest Markets Plc’s Imogen Bachra and Giles Gale see the EU’s green debt standard being applied to the bonds in the third quarter next year, while the EU has said issuance is due to start in the second quarter. Judging by last month’s blockbuster social bond sale, which also followed guidelines set by the ICMA and another party, demand for the triple A-rated bonds is expected to be high.

Gold Standard

The EU’s green bond rules will be “basically a gold standard for the market,” said Trisha Taneja, head of ESG advisory at Deutsche Bank AG. “The first step for the market to move towards the standard is to set the standard, and right now, there’s no clarity.”

The draft of the EU’s green bond standards goes further than those from the ICMA. The rules include more rigor and accountability from issuers, stricter definitions of what constitutes a green project, and would make reporting on the environmental impact compulsory, according to Maia Godemer, a research analyst for green and sustainable finance at BloombergNEF.

The latter element has been a criticism of existing debt as investors lack the ability to judge the results of what their money is being spent on.

| Read More |

|---|

|

Some argue that the EU issuing green bonds under different principles to its own -- at least in the short term -- wouldn’t necessarily damage the market, especially since its issuance is likely to span several years.

“I see that there’s a timeline issue, but overall, long term, it’s better to have a good strategy and implementation than to hurry to gain a quarter or two,” said Aila Aho, executive adviser for sustainability at Nordea Bank Abp, who was on the EU Commission’s Technical Expert Group for Sustainable Finance.

Mishmash of Rules

But without the EU’s standards, investors are faced with a mishmash of guidelines on disclosure and transparency, leaving loopholes for less-than-ideal use of the cash. There have been almost $40 billion worth of greenwashing incidents as of September, where assets have financed ineligible projects, according to definitions from the Climate Bonds Initiative -- a non-profit which created the first green bond standard in 2010.

While this may be more of a problem for emerging markets than Europe, where Sweden’s debut notes were rated as “dark green” by research provider CICERO, the bloc is still trying to wean itself off coal power. Dutch investor NN Investment Partners ditched its holdings of green bonds from Poland, citing an unclear climate policy by the EU’s most coal-reliant nation.

Ideally, the EU “should wait till the green bond standard is valid,” said Sylvain de Bus, deputy head of global bonds at asset manager Candriam, adding doing so beforehand wouldn’t be “optimal.” Asked whether he would still buy the assets, he said he would wait to “see when they issue the first green bond where we will stand in terms of the taxonomy.”

©2020 Bloomberg L.P.