Wall Street’s ESG Loans Charge Corporate America Little for Missed Goals

Banks and borrowers are rushing to add sustainability targets to loans, yet for many deals the incentives are all but meaningless.

(Bloomberg) -- When American Campus Communities Inc. announced the signing of a $1 billion sustainability-linked credit line in May, its executives decided to take a victory lap.

For the first time, they said, the company was tying its borrowing costs to targets ranging from improved energy efficiency to workforce and boardroom diversity. The largest owner of college apartments in the U.S. even put out a press release touting its commitment to environmental, social and governance goals.

What the statement didn’t say was that the financial incentives embedded in the loan were largely meaningless. American Campus Communities faced no extra cost for failing to achieve its ESG targets, and would save only one one-hundredth of a percentage point in interest — a mere $100 a year for every $1 million drawn — if it met all of its goals.

And this, it turns out, is hardly the exception in the ESG loan business.

A Bloomberg analysis of over 70 sustainability-linked revolving credit lines and term loans arranged in the U.S. since 2018 shows that more than a quarter contain similar provisions: no penalty for falling short of stated goals, and only a minuscule discount if targets are met. Other companies that have widely publicized similar arrangements, including JetBlue Airways Corp. and Prudential Financial Inc., declined to disclose details of their loans.

As corporate America grapples with growing scrutiny of its ESG efforts, firms are increasingly turning to Wall Street to help burnish their credentials. Yet critics say more and more companies are presenting overly polished images of both their commitments and results. The findings suggest that while bank loans offer corporations one of the easiest avenues to access ESG financing, the path is also one of the least ambitious.

“It’s just disingenuous,” said Peter Schwab, a portfolio manager at Impax Asset Management, one of the largest money managers dedicated to sustainable investments. “There is really no material financial impact. I don’t know why some companies even bother.”

American Campus Communities attributed the terms of its deal to the firm being an “early adopter” in the sustainability-linked loan market, and said its public comments ensure the company is held to account by lenders and shareholders for its ESG commitments.

“Ultimately it’s really lender driven,” Ryan Dennison, the firm’s senior vice president for capital markets and investor relations, said of the pricing adjustments the company secured. “We could either do nothing, or we could do something and express some of our ESG goals and work toward those.”

Sustainability-linked loans aren’t to be confused with so-called green bonds that have swept global finance in recent years — and which face significant skepticism in their own right.

For one, the loans don’t restrict what companies can do with the funds. Instead, lenders agree to tie interest rates to certain ESG metrics. Corporations, in theory, stand to benefit from lower borrowing costs if they meet their goals, and face penalties if they fall short.

Banks also tend to keep revolving credit facilities on their balance sheets rather than distribute the risk to investors. Companies can tap them as needed, though they often leave them undrawn for years.

Paltry Penalties

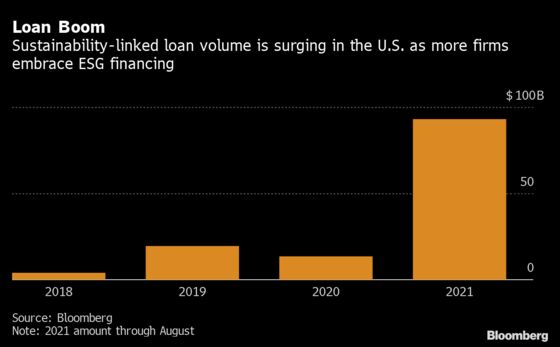

It’s a relatively novel form of financing, especially in the U.S. About $93 billion of sustainability-linked loans have priced this year, or seven times the $13 billion arranged in all of 2020. Still, it’s only a fraction of the nearly $1.5 trillion of loans syndicated in the U.S. year-to-date, according to data compiled by Bloomberg.

Some industry watchers expect economic incentives to get more aggressive as the market develops. And to be sure, certain firms use them as part of a wider array of tools to help achieve (and convey to investors) their environmental and social objectives.

But in other cases, sustainability-linked loans have seemingly become a way for companies to tout their ESG bona fides while risking the absolute bare minimum, potentially adding to concerns about so-called greenwashing that have emerged in other areas of sustainable finance and attracted scrutiny from regulators.

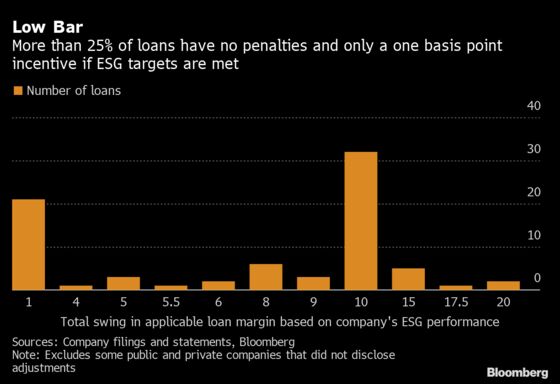

Bloomberg used public filings and information obtained from companies to analyze 77 revolving credit facilities and term loans that included sustainability adjustments.

About 40% of the borrowers agreed to pay a penalty of five basis points if they failed to meet their targets in exchange for a five basis point discount if they achieved their goals -- a total swing of 10 basis points.

A pair of borrowers, Millicom International Cellular SA and Diana Shipping Inc., set the adjustments at 10 basis points in either direction.

For more on sustainable finance:

At the opposite end of the spectrum, more than a quarter of firms had incentives that amounted to a single basis point if they drew their revolvers, like American Campus Communities did. When credit lines remain untapped, sustainability adjustments either don't apply or amount to one basis point at most.

“Most of the pricing adjustments upward or downward are tiny,” George Serafeim, a professor at Harvard Business School who focuses on corporate performance and social impact, said via email. “It seems to me more a symbolic gesture rather than a serious effort to price and embed in the contract climate risk.”

Almost all members of this one-basis-point club are real estate investment trusts, or vehicles that own large property portfolios and distribute most of the income they generate as dividends. Among them are multibillion-dollar companies such as Simon Property Group Inc., one of the largest shopping mall landlords in the U.S., and Welltower Inc., one of the biggest owners of senior living facilities.

Many REITs are likely choosing such provisions simply because it’s what their peers have done, said Nathan Cooper, a partner at Hogan Lovells who helps arrange sustainability-linked loans.

“It’s a formula that is already out there and vetted by the banks and doesn’t pose any downside risk to the REIT,” Cooper said via email. “You are seeing now companies and banks being a little more conservative with the pricing adjustments and being wary of the downside pricing risk on a new concept.”

Simon Property Group didn’t respond to requests seeking comment, while a representative for Welltower declined to comment.

While the financial impact may not be meaningful for companies, there is a reputational risk if goals aren’t met, according to Arthur Krebbers, head of sustainable finance at NatWest Markets in London.

“It's too narrow to view those loans purely through a direct pricing-incentive lens,” Krebbers said. “What they're much more concerned about is the wider reputation and market impact if they have to reveal they didn't meet a core sustainability target they set out.”

Bankers’ Dilemma

For lenders including Bank of America Corp., JPMorgan Chase & Co. and BNP Paribas SA, the three largest global underwriters in the market, getting companies on board is a delicate balancing act.

Some bankers who work in ESG financing said that while their institutions want to encourage clients to become better corporate citizens, there is only so much of their bottom line they are willing to sacrifice. Credit lines are often money-losing products banks offer to companies in order to cement relationships and attract more lucrative business down the line.

But therein lies a fundamental dilemma, observers say.

Banks are reluctant to provide too big of a discount to borrowers that meet targets out of concern the loans will become overly burdensome. If penalties are too steep, on the other hand, they risk pushing customers away.

Better incentives can be found in the sustainability-linked bond market, where money managers with specific mandates to invest in ESG debt typically exact heavier punishments from companies that miss their targets. Penalties for bonds typically range between 25 basis points and a full percentage point depending on the issuer, market experts say.

Advocates for stricter standards across the industry say another critical issue is to ensure that the goals set by companies are ambitious and require firms to stretch from their current path.

American Campus Communities listed three main ESG objectives when it closed on its revolver four months ago. In addition to energy efficiency improvements, it sought 30% representation from women, racial or ethnic minorities, and members of the LGBTQ+ community on its board, and targeted 70% for its workforce.

But as of the end of 2020, the Austin, Texas-based firm had already met its two diversity targets, according to its annual ESG report.

Impax’s Schwab said that ideally corporations would commit to material improvements in their metrics and steep penalties if they fail to achieve them.

“We are extremely supportive of companies that are measuring and setting goals,” he said. “Companies are starting to get a bit more serious, but that’s not enough.”

©2021 Bloomberg L.P.