Erdogan Risks a $163 Billion Bout of Market Nausea

(Bloomberg Opinion) -- Berat Albayrak, Turkey’s well-connected new treasury and finance minister, certainly can talk tough. He promised on Thursday to do whatever market conditions require to stop his country plunging further into financial crisis. But it’s hard to believe that any lessons have been learned from his father-in-law Recep Tayyip Erdogan taking on the markets – and losing.

Albayrak promises “a central bank that is effective like never before.” But how precisely? Saying that speculation about the central bank’s independence is “unacceptable” is hardly a promising start. Merely insisting that it is independent won’t quite cut it. Moody’s Investors Service doesn’t think so, as the ratings agency made plain on Thursday.

The vow by the president’s son-in-law to bring inflation down to single digits in the shortest time possible has to depend on raising interest rates aggressively. Yet that hardly marries with Erdogan’s remarks on Wednesday that rates will fall. They’ve been hiked 500 basis points since late April to try to shore up the currency. Erdogan may have been re-elected on June 24 with enhanced powers, but they don’t appear to extend to market logic.

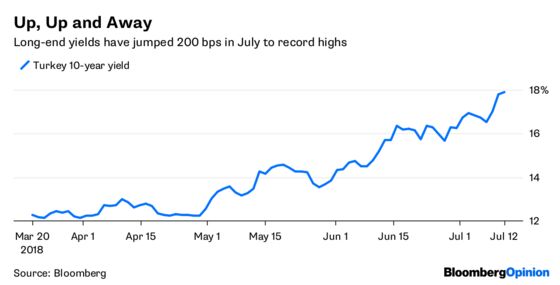

It’s dreamland economics to think that the new administration can lower interest rates and inflation, while boosting the lira. If the central bank is ordered to lower the benchmark one-week repurchase rate, it doesn’t mean that longer maturities will follow. Bond yields would move sharply higher, while the currency would plunge. The 10-year yield (at 18.85 percent) and the lira (at 4.97 to the dollar) hit new records on Erdogan’s remarks. While they’ve recovered modestly, the direction of travel is clear.

The next central bank meeting is on July 24 when we should see quite how independent it remains. Another 100 basis points of rate hikes would be needed to calm the markets. June’s 15.4 percent inflation is unlikely to be the top as the currency weakness and higher oil prices feed in.

And Erdogan’s interest rate remarks weren’t even the most troubling thing he said this week. That honor goes to his comment on private banks having to share the burden. It’s hard to determine precisely what this means but bank stocks sold off heavily as a result. The sector has fallen 25 percent this year.

His bank intervention raises the specter of capital controls, a scary concept for a country with such a large and growing current account deficit that relies so heavily on overseas funding. As of July 6, there were $162.75 billion of foreign currency deposits in the Turkish banking system.

If these could be held only in Turkish lira, it would have a devastating impact on confidence in the banking system. State control of banks is a slippery slope. No foreign lender will extend credit into a country when there’s evident risk that it might be impossible to extract. Turkish banks have been slow to roll over upcoming one-year foreign currency debt maturities with foreign banks.

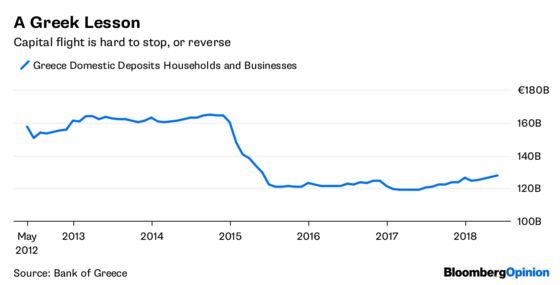

Capital flight, either offshore or into assets such as gold, is hard to stop once it gets going. A recent example is Greece, when fears of capital controls saw a sustained exodus of deposits that is yet to be substantially reversed.

Erdogan may believe he has control over all matters, but he’s not ruling a closed economy abundant in natural resources. Quite the reverse: Turkey is dependent on foreign markets. There are none so deaf as those that won’t listen. Time for another lesson from the markets.

To contact the editor responsible for this story: James Boxell at jboxell@bloomberg.net

©2018 Bloomberg L.P.