Enjoying the IG Credit Rally? Good. Now Comes the Hard Part

Enjoying the IG Credit Rally? Good. Now Comes the Hard Part

(Bloomberg) -- Enjoy the current investment-grade credit rally because it may not last for long, according to some forecasters who foresee a bumpy ride in the back half of 2019.

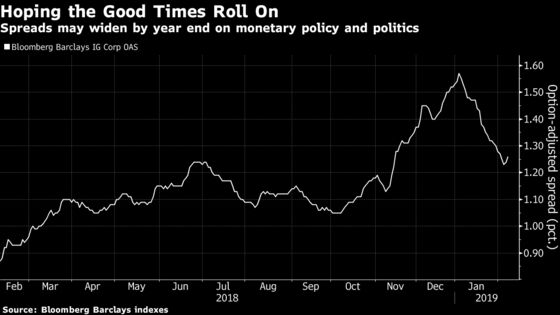

While the Bloomberg Barclays US Aggregate Corporate Average Index badly lagged U.S. Treasuries during the last two months of 2018 by 2.26 percent, it staged a robust turnaround during January, outperforming by 1.83 percent, its best month since March 2016. The good times may prove fleeting.

For starters, David Lafferty, Chief Market Strategist at Natixis Investment Managers, a firm with $1.1 trillion assets under management across asset classes, estimates the Bloomberg Barclays US Aggregate Corporate Average Index option-adjusted spread could reach levels as high as 175 basis points by year-end from its current 126.

One would need to go back to March 2016 for the last time OAS was that high. Spreads subsequently tightened as commodity prices rallied and China’s monetary and fiscal stimulus efforts helped mute concerns over slowing growth. Similar growth concerns have arisen of late, and that may push OAS wider as the year progresses. "An environment of heightened credit ’concern’, but not ’crisis’," will help credit spreads get there, says Lafferty.

Voya Investment Management’s Chief Investment Officer of Fixed Income Matt Toms agrees spread widening is in the cards and forecasts a gradual widening in the second half with OAS drifting toward 150 basis points by year end. "You need to be paid more in investment grade credit" to account for downside risk, he said.

Toms says the market is trying to find its proper level to account for geopolitical and economic risk. At current spreads, the tightening potential is largely played out. Should a rally continue, "We would begin to look at the market as being a little bit tighter than it needs to be and we would look to reduce exposure." he adds.

Some investors still forecast more rate hikes are coming, with one by mid-year and the possibility of another one in the back half of 2019. An impending recession and election cycle are weighing heavily on the Federal Reserve, according to Michael Terwilliger, Portfolio Manager of Resource Financial Fund Management.

"The Fed has a pretty tremendous incentive to try to push rates higher while the economy is strong and while jobs are being created in order to give themselves a monetary tool over the next downturn," says Terwilliger. As the central bank wishes to protect its independence, it has an incentive to avoid rate hikes in an election year to avoid the appearance that it is taking sides politically, he added.

"Political uncertainty is positioned to grow as you enter the full swing of the US election cycle," says Toms, who believes the risk to consumer confidence, which has been resilient thus far, will only increase as the 2020 presidential election nears. He predicts a hike in the third or fourth quarter with the potential for another after that.

QE Moves Out, Volatility Moves In

"Volatility is here to stay," says Lazard Asset Management Managing Director Yvette Klevan, who is responsible for the firm’s global fixed income portfolio. As some investors point to the ongoing list of geopolitical uncertainties fueling volatility, Klevan adds that it is the result of being in a world post quantitative easing. "I think that QE dampened volatility and now you’re getting the opposite of that," she said in an interview.

"As we move later into the year, I expect spread volatility to return," Lafferty adds, predicting the chances for a 2020 US recession to be as high as 40 percent.

Toms warns of a slowing growth environment, not a recession, that will lean on consumer confidence as the year progresses making added risk in the second half of the year not only a possibility, but "underappreciated." Terwillinger echoes the sentiment, but points to interest rates as the main source of risk saying it is "massively underestimated" by the market.

Others are taking a more optimistic view of the future, though, with some investors saying any widening will be short lived.

Krishna Memani, Chief Investment Officer and Head of Fixed Income at OppenheimerFunds, expects OAS to bottom out around 100 basis points by year end. This would still be above the half-a-decade low of 85 basis points seen in February 2018, according to data compiled by Bloomberg News. "Given the likelihood that growth and policy uncertainty will linger, we think it is unrealistic to expect it to tighten back to its previous tights."

Thomas Murphy, Head of Investment Grade Credit at Columbia Threadneedle Investments, expects spreads to end the first half of 2019 at current levels, but also expects the second half of the year to see bumps on the road.

"With the possibility of good news coming from US trade talks and a US economy that seems to be slowing gracefully, my expectation is we will end the year around current spread levels," says Murphy.

To contact the reporter on this story: Kriti Gupta in New York at kgupta129@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Allan Lopez, Christopher Maloney

©2019 Bloomberg L.P.