Emerson Avoids an Activist Fight But Not the Gloom

(Bloomberg Opinion) -- Emerson Electric Co. may have dodged a proxy fight, but it can’t avoid an earnings slump.

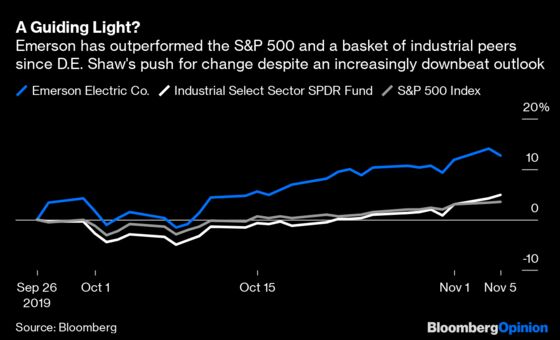

The maker of air-conditioner components and automation equipment said Tuesday that it would add the former chief executive officer of Flowserve Corp. to its board and pledged to complete a review of its operations by February. The moves are meant to be a balm for activist investor D.E. Shaw & Co., which has called for more aggressive cost cuts, corporate governance improvements and a breakup. A lack of tangible commitments and deadlines in Emerson’s agreement to consider the activist’s recommendations likely contributed to a notably feisty letter from D.E. Shaw last month that blasted what it described as a bloated budget, including a corporate aviation department with no fewer than eight jets, a helicopter and its own intern.

Emerson’s new board member, Mark Blinn, was CEO of Flowserve from 2009 to 2017. He’s not a household name, and Flowserve underperformed the S&P 500 Index during his tenure, but he was one of four candidates D.E. Shaw recommended, according to Bloomberg News. As such, the activist said Tuesday that it would back the company’s slate. According to D.E. Shaw, Emerson has also committed to reviewing how it pays its executives and will seek shareholder approval to amend its charter so that directors are elected annually. There was no update on those corporate jets in the earnings materials released Tuesday morning, although a conference call is scheduled for later this afternoon.

Emerson’s concessions to D.E. Shaw are wise; it’s not in a position to pick a fight now. Also on Tuesday, the company released disappointing guidance for its 2020 fiscal year and predicted the coming U.S. presidential election, continued trade tensions and increased restructuring by manufacturers would leave investment decisions stalled. “We are planning for a challenging economic environment,” CEO David Farr said in the news release. This was a notably more downbeat outlook on the economy than other industrial companies have given this earnings season and contrasts with Parker-Hannifin Corp.’s prediction last week that its own sales slump would bottom out in the middle of its 2020 fiscal year.

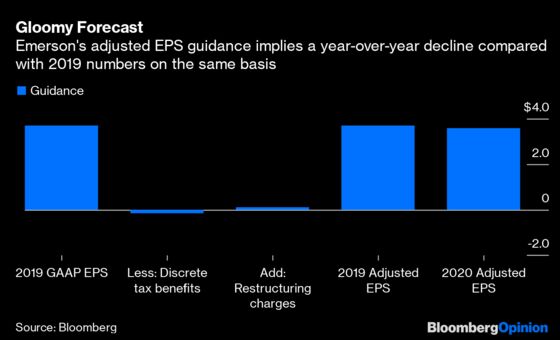

Emerson’s guidance for $3.48 to $3.72 in adjusted earnings per share implies a decline compared with last year’s numbers on the same basis. Sales may slump as much as 2%, excluding the impact of currency swings and M&A. With numbers like that, Emerson’s goal of achieving $4.50 in EPS by 2021 would be a significant stretch. Emerson said it will “reset” its long-term guidance as part of its February update. What’s troubling is that Emerson’s 2020 outlook doesn’t appear to reflect many benefits from the $95 million it spent cutting costs over the past year to adjust its operations to the downturn, Gordon Haskett analyst John Inch wrote in a report on Tuesday.

That’s key because cost cuts sit at the crux of D.E. Shaw’s argument for a higher stock price. Analysts have pushed back on D.E. Shaw’s estimate of more than $1 billion in excess costs at Emerson, noting that some of the activist investor’s margin comparisons are unfair because many of the company’s rivals strip out restructuring, pension expenses and other expenses. In response, Emerson provided additional details about its pension and stock compensation costs for its most recent results. But it also moved to an adjusted earnings outlook after previously giving its forecast on a GAAP basis except in certain circumstances. The company says this is because 2020 restructuring actions will be determined as part of the board’s review and the guidance will be updated in February to reflect that. Let’s hope that’s true and that D.E. Shaw’s push doesn’t have the unfortunate side effect of yet another industrial company becoming addicted to earnings adjustments.

To contact the editor responsible for this story: Daniel Niemi at dniemi1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.