Emerging-Market Dud Turkey Wins Favor as a Top Trade for 2019

AllianceBernstein, NWI pick Turkish debt as top 2019 trade.

(Bloomberg) -- A currency crisis, credit-rating downgrades and U.S. sanctions wreaked havoc on Turkish markets this year. Yet that turmoil has set the stage for one of next year’s most attractive trades in the developing world, according to AllianceBernstein and NWI Management.

Shamaila Khan, AllianceBernstein’s director of emerging-market debt, and Hari Hariharan, chief executive officer at NWI Management, both picked Turkish bonds as their top trade idea for 2019 during a panel discussion Thursday at the Emerging Markets Traders Association’s annual meeting in New York. Khan said she favored lira-denominated notes, while Hariharan preferred Turkish dollar bonds, especially in the banking industry.

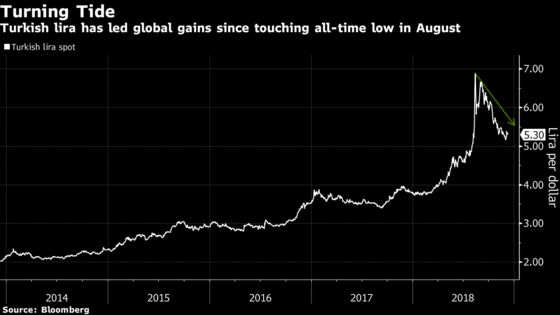

There are some signs the tide has begun to turn. Since slumping to an all-time low in August, the lira has rallied 30 percent, more than any other major currency tracked by Bloomberg. Still, higher interest rates have crippled some Turkish companies and Moody’s Investors Service expects the economy to shrink through 2019’s first half.

"The last time, two months ago, I had the same trade and people almost killed me on the panel," Khan said.

Two other investors on Thursday’s panel had different ideas. Jim Barrineau, the New York-based head of emerging-market debt at Schroders, said he recommends a basket of short-duration non-investment grade bonds from developing nations.

"Hold it and go to sleep, and you’ll outperform virtually every other asset class," he said.

The fourth panelist, BlackRock Inc. portfolio manager Pablo Goldberg, said he expects emerging-market debt to look more attractive next year compared with U.S. high-yield notes as U.S. growth slows.

Here’s what else they had to say:

Khan

- "I could see China going the same way as the USMCA"

- "The technical cleanup should help EM next year. U.S. institutions are under-allocated to EM"

- "Brazil’s post-election euphoria may not be different than South Africa or Mexico, but it should be. The government wants to do the right thing"

- In Brazil, "the honeymoon may end, but the marriage will last."

Hariharan

- "I’m bullish EM, but we need the non-dedicated base of investors to come back. We need the big bond funds to return"

- "I’m almost raging bullish on trade. Skepticism on the 90-day break is unwarranted"

- "I don’t see the yuan falling to 7.5 or 8 per dollar. It will be stable"

- "There are so many names above 7 percent yield, from Turkey to the national oil company in Bahrain. That’s a fabulous value proposition"

- "I’m bullish Brazil, but this is a classic pump and dump. Brazilians are long all local assets. Those who piled in before the vote are now sitting pregnant waiting for foreigners to come buy. The Ibovespa is probably the most over-owned index in the world. A cleansing must happen"

Barrineau

- "The dollar is key. In April 2018, we got crushed. Now, a Democratic House win means no fiscal stimulus package"

- "Powell seems like he doesn’t want to hike until something breaks"

- "The value proposition for EM is pretty compelling"

- "I don’t expect a hard landing in China or for it to be a growth engine"

- "EM and DM are just starting to reach equilibrium after the VIX flat-lined for a long time"

- "Petrobras at 6.8 percent yields doesn’t get my heart racing. Neither does the Brazilian real. And body language from the Bolsonaro administration doesn’t suggest that they’ll slay Congress and push something through. There are better places to invest"

To contact the reporter on this story: Ben Bartenstein in New York at bbartenstei3@bloomberg.net

To contact the editors responsible for this story: Rita Nazareth at rnazareth@bloomberg.net, Alec D.B. McCabe, Philip Sanders

©2018 Bloomberg L.P.