Emerging Asia's Top Bonds Get Fresh Impetus From New Governor

Emerging Asia's Top Bonds Get Fresh Impetus From New Governor

(Bloomberg) -- The new and more dovish Philippine central bank governor could reward the country’s local-currency bond investors with even bigger gains. The securities are already reaping the best profits in global emerging markets after Egypt, Russia, Nigeria and Mexico.

In Asia, Philippine peso bonds have gone to first from worst and Merian Global Investors is staying overweight on prospects Governor Benjamin Diokno will embark on a looser monetary policy amid a benign inflation outlook. AllianceBernstein LP and M&G Investments expect the rally could be supported by cuts in banks’ reserve requirement ratios and the policy rate.

“There is more room for local yields to compress,” said Delphine Arrighi, an emerging-market debt fund manager in London at Merian. “The appointment of former budget secretary Benjamin Diokno as the new BSP governor should also point in that direction.”

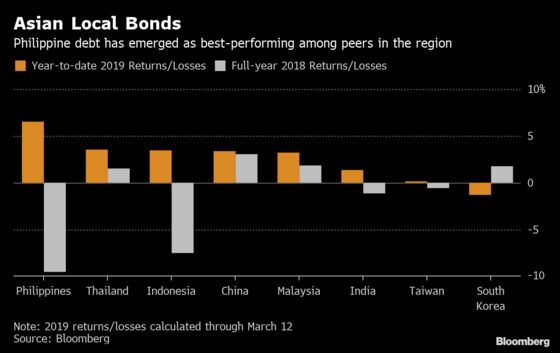

Debt issued from the Southeast Asian nation has returned 6.6 percent this year through March 12, almost double those from Thailand, China and Indonesia. It’s a stark contrast to last year when Philippine notes lost almost 10 percent, the worst among eight emerging local-bond measures in the region tracked by Bloomberg Barclays indexes.

Read what the new governor has said, in his own words

Slowing Inflation

Diokno, who assumed his post on March 7, said on Tuesday the reduction in the reserve ratio could be 100 basis points every quarter for the next four quarters. In an interview with local TV, he said slowing inflation, dovish comments from the Federal Reserve and stable oil prices provide room to cut the policy rate and the reserve ratio.

Consumer-price increases in the Philippines eased to 3.8 percent in February, the slowest pace in a year. Back in October, inflation was at a nine-year high of 6.7 percent.

As inflationary pressure eased, bonds started to turn around. The yield on benchmark Philippine 10-year bonds has dropped 214 basis points to 6.18 percent from a recent peak of 8.32 percent in October, according to data compiled by Bloomberg.

But what’s a boon for bonds is starting to be a bane for the currency, which slid to a six-week low on Wednesday. Both M&G and Merian Global caution the potential for the peso to weaken on lower interest-rate support.

“We are, however, less positive on the currency that could suffer from expectations of looser monetary policy in the coming months,” Merian Global’s Arrighi said.

Traders will watch monetary policy statements to gauge whether the perception that the new governor has a “more pro-growth, dovish bias” is justified, said Claudia Calich, a fund manager in London at M&G, which said in December it bought Philippine bonds. The securities aren’t likely to deliver the same pace of outperformance though, as inflation is unlikely to fall much further, she said.

Click to read how stocks in the Philippines perform during elections

HSBC Holdings Plc is predicting a reduction of 300 basis points in the reserve ratio and 50 basis points in the policy rate this year, Noelan Arbis, an economist in Hong Kong, wrote in a March 11 report. A 100 basis-point drop in the reserve ratio will likely precede the first rate cut, which could come in the second quarter, he said.

“Easy” gains in Philippine bonds have been made after the recent slide in inflation, said Brad Gibson, AllianceBernstein’s head of Asia-Pacific fixed income portfolio management in Hong Kong. He has cut exposure to the notes after the initial target of below 6.5 percent for the 10-year yield was met, he said.

But yields at 6 percent is still “worth grabbing,” he added.

To contact the reporter on this story: Lilian Karunungan in Singapore at lkarunungan@bloomberg.net

To contact the editors responsible for this story: Tomoko Yamazaki at tyamazaki@bloomberg.net, Karl Lester M. Yap

©2019 Bloomberg L.P.