Emerging-Market Carry Trades Risk More Losses After Decade of Gains Wiped Out

Emerging-Market Carry Trades Risk More Losses After Decade of Gains Wiped Out

(Bloomberg) -- The coronavirus outbreak wiped out a decade’s worth of returns for emerging-market carry trades, and more losses may be just around the corner.

A decline in yields due to central bank stimulus has diminished the attractiveness of many emerging currencies, reducing their allure as carry targets, according to TD Securities Inc. Developing-nation currencies remain vulnerable to further losses due to uneven inflows and elevated volatility, Bank of America Corp. says.

“The environment for carry will likely become more difficult in the months ahead if, as is likely, the dollar rallies amid a decline in real yields among many EM currencies,” said Mitul Kotecha, senior emerging markets strategist at TD Securities in Singapore. “A more selective approach to EM FX would likely work better in the second half, with relative value trades preferable.”

An index that measures returns from borrowing in dollars and investing in eight high-yielding emerging currencies including the Brazilian real and the Indonesian rupiah slumped 16% from the start of the year to touch a more than 10-year low in April, according to data compiled by Bloomberg. The gauge trimmed some losses through May, but the recovery has now stalled, leaving it down 11% for the year.

Carry trades are a bellwether for risk-on sentiment, and the prediction of further losses adds to evidence the global recovery from the virus pandemic will be far from straightforward. The petering out of the rebound in the carry index also reflects the damage to confidence caused by widening fiscal deficits and renewed U.S.-China tensions.

Dollar Debate

The U.S. currency will probably resume its appreciation path in the months ahead, adding another challenge for investors seeking to use it as a funding vehicle for carry trades, TD Securities’s Kotecha said.

“The dollar will begin to react more to relative U.S. growth and asset-market outperformance,” he said. “This will help to push it higher against developed and emerging currencies. In this respect, funding EM currencies utilizing the USD is unlikely to pay off.”

The outlook for carry trades isn’t all doom and gloom.

A number of factors suggest the dollar will face growing headwinds, including its rich valuation and waning support from interest-rate differentials, said Stuart Ritson, a fund manager for emerging-market fixed income at Aviva Investors in Singapore.

“The macro backdrop has the potential to be supportive for EM carry trades as growth rebounds and global policy makers continue to dampen volatility,” he said. “Carry trades don’t necessarily need a weaker U.S. dollar. A period of stability would be sufficient for this strategy to play out but the largest returns would be captured in a dollar downtrend.”

Investors may still find opportunities in carry trades betting on the Mexican peso, Russian ruble and Indonesian rupiah due to their relatively high inflation-adjusted yields, Ritson said.

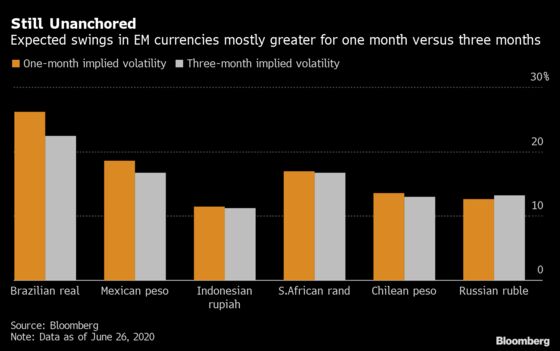

One of the major factors that deters investors from engaging in carry trades is high volatility -- and the situation here also appears discouraging.

Implied volatility is higher for one-month options than three-month contracts for currencies such as the Brazilian real, Mexican peso, and Indonesian rupiah, suggesting markets see inflated near-term risk, according to Bank of America.

“A number of implied volatility curves in EM FX are still inverted, which suggests EM currencies are still unanchored and vulnerable,” said Claudio Piron, co-head of Asia foreign-exchange and rates strategy at Bank of America in Singapore. While the worst of this year’s sell-off in EM carry trades may be behind us, “don’t expect a dramatic rally,” he said.

©2020 Bloomberg L.P.