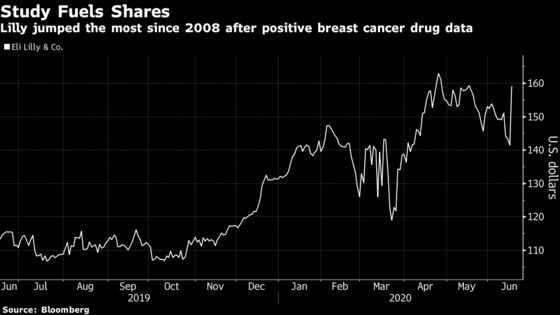

Lilly Jumps Most Since 2008 as Data Shock After Pfizer Flop

Lilly Jumps Most Since 2008 as Data Shock After Pfizer Flop

(Bloomberg) -- Eli Lilly & Co. surged the most since 2008 after a positive study for its drug combination in patients with a type of breast cancer was heralded by analysts as a surprising and transformational event for the company, especially in the wake of Pfizer Inc.’s failure earlier this month.

The positive results from the trial -- dubbed “monarchE” -- showcased the effectiveness of Lilly’s Verzenio in combination with standard adjuvant endocrine therapy and support management’s claims that the medicine is differentiated from competitors, Guggenheim analyst Seamus Fernandez wrote in a note to clients.

“The early success of ‘monarchE’ likely is a transformational event” for Lilly, Fernandez wrote while upgrading shares to a buy. JPMorgan analyst Chris Schott touted the “encouraging/surprising” results and said the opportunity for Lilly from the study represents $2 billion in annual sales over time.

Shares of the Indianapolis-based drug developer jumped 13% at 9:53 a.m. in New York, the largest one-day climb since October 2008. The drug maker had shed 13% of its value from an April peak through Monday’s close, but is now up 40% in the past year.

Read more: Pfizer Ibrance Failure Draws Analyst Ire as ‘Missed Opportunity’

Here’s what analysts have to say about the update:

Guggenheim, Seamus Fernandez

“It remains possible that other adjuvant studies” from competitors Novartis AG and Pfizer succeed, “but the early success of ‘monarchE’ likely is a transformational event for Lilly as the company advances toward other key catalysts.”

Cautious feedback from specialists in the wake of Pfizer’s “recently failed ‘Pallas’ study makes the interim success of Lilly’s ‘monarchE’ study an even more significant surprise.”

Upgrades to buy from neutral and sets price target to $182.

JPMorgan, Chris Schott

Data win is a “significant positive for Lilly shares, positioning Verzenio as the first CDK 4/6 to show disease-free survival and coming on the heels of the Ibrance ‘Pallas’ futility stoppage earlier this month in a broader population.”

“We expect Verzenio will be first to market in this setting with Pfizer’s ‘Penelope’ study expected to report out later this year and Novartis data expected in 2022.”

“It is unclear [if] dosing differences between Verzenio and Ibrance will play a greater role in adjuvant as compared to the metastatic setting.”

Rates shares overweight.

Cantor Fitzgerald, Louise Chen

“The positive results today underscore a significant opportunity for growth for Verzenio, given that it is now currently the only CDK4/6 inhibitor to show positive Phase 3 data in the adjuvant breast cancer setting.”

Lilly has “previously noted that, if successful, the ‘monarchE’ data could increase Verzenio’s addressable patient population by ~50%; if the positive adjuvant data also shifts physicians’ preferences to Verzenio as the preferred CDK4/6 inhibitor, we think the peak sales potential for Verzenio could reach” $7.5 billion and beyond.

Rates shares overweight with a price target of $185.

Barclays, Carter Gould

Lilly’s “Verzenio win in adjuvant adds new dimension” to the company’s narrative as it “completes a high-profile (and unexpected) shift in the CDK4/6 landscape.”

“The net impact of this is that it opens up a multi-billion opportunity” for Verzenio with “a meaningful head start vs competitors that was largely not in Street models to any meaningful extent a few months prior.”

Reiterates overweight rating and $160 price target.

©2020 Bloomberg L.P.