Eleven Shades of Red Is as Provocative as It Gets: Taking Stock

Eleven Shades of Red Is as Provocative as It Gets: Taking Stock

(Bloomberg) -- It might be time to peek through those fingers to see if it’s over yet. All 11 sectors of the S&P fell Wednesday, yet another day where equities were not the preferred asset class -- despite that late session bounce.

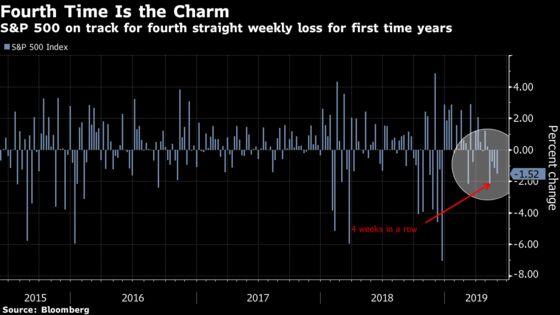

The fact remains that the past two days of losses since coming back from the holiday weekend means this week is on track to fall for the fourth-straight time, the longest streak of weekly losses since June 2016.

It’s tough to look for positives when the S&P 500 broke below its 200-DMA (though thankfully for the bulls, closed above that key technical level) and also below the neckline of the head and shoulders pattern chartists love to draw. The shake-out of risk is real --Bridgewater’s Ray Dalio said its a “risky time” ahead in the U.S.-China trade conflict, while PIMCO’s chief investment officer of U.S. core strategies, Scott Mather, said in an interview on Bloomberg that the credit market risk is at an all-time high.

And for most of the day it was a flight to (or less of an evacuation from) quality. Levered names bore much of the selling before the late day bounce, but the picture remained the same -- value was in vogue (after struggling this past year) and momentum names were sold. This could point some to the fact that the bottom may be firming (now that we are in full correction territory, more than 5% off the late April highs) after a painful few weeks. Sectors that usually benefit from lower rates were being sold, a sign the dynamics are changing -- and in that same vein, banks were among the best performers despite the yield curve’s drubbing.

Get Down and Dirty

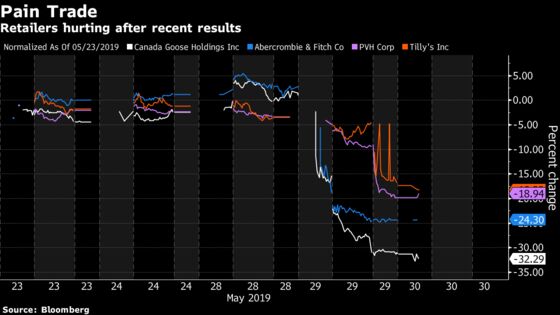

But just because the air has the potential to be clearing at 30,000 feet (and futures are now responding in kind, up 11 handles here in the early going) doesn’t mean the dirty details of trade angst aren’t playing out at ground level. Online apparel distributor Tilly’s and brand holding company PVH Corp. Wednesday after the close perpetuated the struggles we saw with Canada Goose and Abercrombie during the day (both of which recorded losses in excess of a quarter of their market value during regular trading). PVH is indicated to open lower by nearly 11%, and cited “particular softness” with regards to the U.S./China retail for its lowered full year outlook, while Tilly’s is down 14%.

Discount retail will keep the data points coming on the consumer this morning as a series of players like Dollar Tree, Dollar General and and Burlington Stores provide their quarterly assessment. One can definitely see how companies that refer to themselves as “dollar stores” might find it especially awkward during these new trade war times we live in to communicate why many of their products now cost “a buck 25.”

Bloomberg Intelligence analysts Poonam Goyal and Abigail Gilmartin recently wrote that the dollar stores have been accelerating purchases (to get ahead of tariff impacts) of products embroiled in the dispute -- as that 25% tariff could “directly raise the cost on some goods”, which ultimately will be seen by the end customer. 2018’s results at Dollar General included a $27.4 million higher provision related to tariff and transportation-cost pressures, they wrote. It’s not theoretical -- it’s showing up in practice too, as Walmart indicated it too would be raising prices on products due to tariffs just two weeks ago.

But there’s an old sage that reminds us that bad (or good) companies can still be good (or bad) stocks (for the record I’m not implying the above names are either). And that must be acknowledged when evaluating these companies as they report. Buckingham in a note ahead of DLTR’s results said that the stock has “significantly de-risked” ahead of results. Keybanc analysts wrote that both DG and DLTR can still be ideal for investors looking for growth and defensiveness (while in the same breath lowering estimates on tariff impacts).

Burlington and DG’s results just hit the tape with the former cutting its full year comparable sales forecast and the latter, despite beating on sales and comps, is just maintaining its financial forecast for the year. J. Jill is another example where it’s all about expectations for the stock rather than the company. The clothier’s shares fell more than 12% in sympathy with the retail selloff Wednesday, ahead of its results this morning that thus far appear to have missed.

Sectors in Focus

- Retailer Express is one of the few brands trading higher this morning after results from PVH and TLYS disappointed -- following GOOS and ANF yesterday

- Rare earths (including lithium miners LTHM, SQM, ALB and others like FCX, TECK, TRQ CN, TKO CN, NDM CN, GMO) will remain a focus as the overhang from China’s perceived threats remains

- E&Ps as WTI crude rebounds slightly from its latest slip attributed to global economic worries

- CRM companies (IQ, OTEX, MDSO, ORCL, BOX )after VEEV results surprised to the upside; SVB Leerink analysts noted strength across the entire business

- Recent volatile IPO names (UBER, LYFT, SWAV, TW, AVTR) ahead of UBER’s first results as a public company due after the close. Some preliminary numbers had been released ahead of their IPO, but analysts will look for forecasts on profitability and revenue, though it’s uncertain if any will be provided. Beyond Meat soared again yesterday (among the few names that rose) and is also looking higher in the pre-market.

Notes From the Sell Side

Verizon Communications was lowered to neutral at UBS, which wrote that while wireless fundamentals should remain supportive, the division was unlikely to see an acceleration in growth off current levels. “With valuation back in-line with historical levels and more difficult comps ahead, we see a more balanced risk-reward skew,” wrote analyst John Hodulik. He kept his $59 price target, a level that implies upside of about 1.4% from Verizon’s Wednesday close. “Verizon is well-positioned as a defensive investment with [low single digit] core growth and sustainable yield,” he wrote. Shares of the Dow component are down about 0.8% pre-market.

Citigroup was upgraded to buy at Goldman Sachs, with the firm seeing upside potential in the company’s return on average tangible common shareholders’ equity (ROTCE). Goldman sees “a realistic path” to a 13% ROTCE in 2020, a path “which is not contingent on either higher interest rates or strengthening global growth trends.” Per analyst Richard Ramsden, the market is looking for a 12% pace. “The market is overly pessimistic on C’s revenue growth inflection, targeted expense savings, and outlook for credit costs given the improvement in the risk profile of their international loan book,” he wrote, lifting his price target to $77 from $71. Citi is up about 1.1% on light pre-market volume.

Hybrid cars may have become something of an afterthought given the growing popularity of fully electric vehicles, but Barclays still sees some gas in the tank, upgrading BorgWarner to overweight, calling it the "best positioned for hybrid growth in the 2020s." Analyst Brian Johnson conceded that “hybrids may be unfashionable,” but said they offer a “real growth opportunity,” and that "the compelling 2020s volume potential deserves a higher multiple." BWA’s technology and product leadership, he wrote, "will allow it to continue innovating and delivering propulsion systems for the automotive landscape in the long-term."

Separately, Barclays cut its price target on Tesla to $150 from $192.

Tick-By-Tick Guide to Today’s Actionable Events

- FSOC meeting

- Bernstein Strategic Decisions conference in NYC (JPM, WFC, MS, HD, AGN, BIIB, TTWO, TXN)

- Cowen annual TMT conference in New York (T, CY)

- HUM investor meeting

- 7:30am -- DLTR earnings

- 8:30am -- April Prelim. Wholesale Inventories

- 8:30am -- 1Q Second Read GDP Annualized; Second Read Personal Consumption; Second Read GDP Price Index; Second Read Core PCE

- 8:30am -- Weekly Initial Jobless Claims, Continuing Claims; April Retail Inventories

- 8:30am -- WM, EVH investor days

- 9:00am -- PVH, DLTR earnings calls

- 9:45am -- Weekly Bloomberg Consumer Comfort

- 10:00am -- DG earnings call

- 10:00am -- April Pending Home Sales

- 12:00pm -- Fed’s Clarida speaks at the Economic Club of New York

- 1:00pm -- TROX investor day

- 4:05pm -- MRVL earnings

- 4:15pm -- COST, GPS, VMW earnings

- 4:25pm -- DELL earnings

- 4:30pm -- VMW earnings call

- 4:45pm -- MRVL earnings call

- 5:00pm -- COST, GPS earnings call

- 5:30pm -- DELL earnings call

--With assistance from Ryan Vlastelica.

To contact the reporter on this story: Brad Olesen in New York at bolesen3@bloomberg.net

To contact the editors responsible for this story: Courtney Dentch at cdentch1@bloomberg.net, Steven Fromm

©2019 Bloomberg L.P.