Easiest Job in Bonds Turns Exhausting as China Defaults Soar

Easiest Job in Credit Turns Exhausting as China Defaults Soar

(Bloomberg) -- Until a few years ago, figuring out whether a Chinese company would repay its domestic bonds was simple: the answer was always yes.

These days, it’s not so easy. As default rates in China swell from zero to levels approaching those of a normal credit market, the nation’s fixed-income investors are working a whole lot harder to earn their keep.

Chen Su, a bond portfolio manager at Qingdao Rural Commercial Bank Co., is a case in point. He spent a week on the road assessing the credit risk of a Chinese manufacturer last year, logging more than 1,800 miles as he interviewed the company’s managers and customers in Fujian, inspected production facilities in Anhui, and met with competitors in Suzhou. In the pre-default era, his due diligence effort would have involved little more than a chat with executives.

“Now, the process is much more complex,’’ said Chen, who took about 45 research trips in 2018, up from 20 a few years ago.

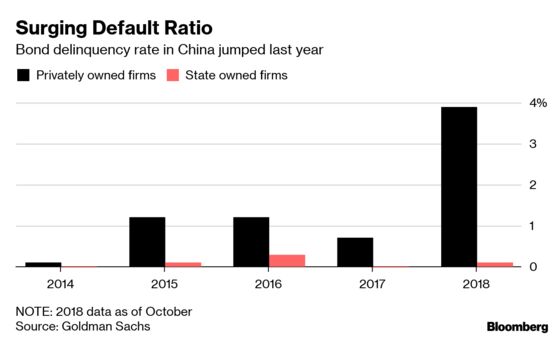

Squeezed by slowing economic growth and waning government appetite for corporate bailouts, Chinese borrowers reneged on a record 119.6 billion yuan ($17.8 billion) of domestic bonds last year and missed payments on another 14.7 billion yuan of notes in the first two months of 2019. While opinions differ on whether the defaults foreshadow a financial crisis or just a healthy shakeout of the nation’s $13 trillion corporate bond market, few dispute the need for investors to pay closer attention to credit risk in China.

That’s easier said than done in a market where reliable information on everything from collateral values to government support is often hard to come by. What follows is a sampling of due diligence advice from veteran Chinese bond managers. Some of their tips will be familiar to global credit investors, but there are also China-specific twists.

Verify Everything

In January, Kangde Xin Composite Material Group Co. jolted Chinese credit markets by missing a bond payment just four months after it reported holding enough cash to repay the debt 15 times over. The episode, which came amid a government investigation into Kangde’s financial reporting, underscored a new mantra for bond investors in China: verify everything.

Zhang Min, a fund manager at ZT Capital who lost sleep this year worrying about misleading financial statements, said he cross-references company results against peers to check whether any numbers look out of place. Mei Yuqing, a fixed-income manager at Ubiquant Investment, uses his own on-the-ground research to assign values to a borrower’s collateral instead of relying on the company’s balance sheet.

“Now we must act as detectives on every possible detail,’’ said Chen Yang, head of fixed-income investment at Shanghai Securities Co. Before buying the bonds of a Chinese coal producer in the remote Xinjiang region last year, Chen spent a week inspecting the company’s inventory, production capacity and supply chain. He also interviewed workers to make sure they were receiving their salaries on time.

Talk to Bankers

Chinese banks still provide most of the credit to Asia’s largest economy, and that makes them an invaluable resource for bond investors.

Chen, the fund manager at Qingdao Rural, said he tries to keep in touch with his portfolio companies’ biggest lenders to make sure they haven’t withdrawn or reduced funding. For buyers of distressed debt in China, the willingness of banks to maintain support for a borrower can mean the difference between a painful default and a profitable investment.

Know the Industry

Bankers comprise just one part of a good due-diligence contact list. Talking to a borrower’s rivals, customers and suppliers can also help investors spot red flags, according to Shi Min, director of credit investment at Beijing Lerui Asset Management.

“Our people need to be experts on the industry,’’ Shi said.

Beware Cross Guarantees

They’re supposed to help smaller Chinese companies gain access to funding by spreading repayment risk among multiple borrowers. But the key assumption behind cross guarantees -- that different borrowers are unlikely to renege on their debt at the same time -- doesn’t always hold water. The risk is that the guarantees end up triggering a default chain reaction.

That worry pummeled the bonds of several companies in China’s eastern Shandong province late last year, prompting the government to step in with liquidity support. Understanding a borrower’s exposure to cross guarantees is now high on the to-do list for many of China’s bond investors.

Consider Government Links

There was a time when bondholders could count on China’s government to bail out borrowers in distress. Not anymore.

As Chinese authorities try to reduce moral hazard, they’re allowing more and more private companies -- and a handful of state-linked firms -- to miss their debt payments.

Read more: The Chinese Bonds Under Repayment Pressure

Some investors, including Chen from Shanghai Securities, have responded by completely discounting the prospect of a bailout.

Others say increased uncertainty about whether Beijing will ride to the rescue can create opportunities. “Assessing government support is part of the skill set we are looking for,’’ said Jean-Charles Sambor, deputy head of emerging market debt at BNP Paribas Asset Management. "At the end of the day, we are paid to identify when credit risk is mis-priced."

To contact Bloomberg News staff for this story: Carrie Hong in Hong Kong at chong61@bloomberg.net;Tongjian Dong in Shanghai at tdong28@bloomberg.net;Xize Kang in Beijing at xkang7@bloomberg.net;Jing Zhao in Beijing at jzhao231@bloomberg.net

To contact the editors responsible for this story: Neha D'silva at ndsilva1@bloomberg.net, Michael Patterson, Lianting Tu

©2019 Bloomberg L.P.

With assistance from Bloomberg