Drilling Some Discipline Into the Shale Frackers

Drilling Some Discipline Into the Shale Frackers

(Bloomberg Opinion) -- In business, one company’s discipline is another’s pain. Oilfield services stocks have been struggling since summer. Schlumberger Ltd., the biggest, is at its lowest level in more than eight years; below even where it got to in the panic of early 2016, when oil dipped below $30 a barrel.

Bottlenecks in the Permian basin have taken some of the heat out of America’s number one oil prospect. But logistics aren’t the only potential headwind here. And the earnings season just getting underway for exploration and production companies — the contractors’ clients — will show just how strong it is.

The frackers need a makeover. The E&P sector trades at the same level as two years ago despite oil prices having risen by almost a third. There has been a brutal de-rating in that time, with the sector’s enterprise value-to-Ebitda multiple dropping from almost 10 times to less than six. The message from investors: Don’t squander the cash.

In a recent report, analysts at Tudor, Pickering, Holt & Co., a boutique energy bank, noted investors were switching up the metrics they use to track E&P performance. Previously, the favored ones were enterprise value-to-Ebitda and net asset value, or NAV, essentially a modified discounted cash flow figure. These days, according to TPH, investors are more interested in price/earnings multiples, free cash flow and return on capital employed. The shift from NAV towards earnings or cash-based metrics, in particular, suggests a shift from a start-up like phase — grabbing land and burning cash — to a (hopefully) more mature, self-funding model.

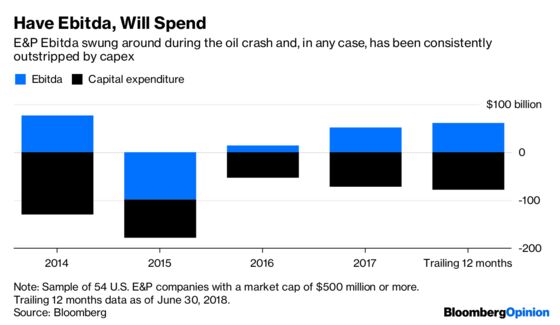

The problem with Ebitda multiples and NAVs was that they largely missed a critical element of the E&P business: reinvestment of cash flow. For example, Ebitda — or Ebitdax if you throw in exploration expense — is often treated as a proxy for cash from operations. This is problematic in itself for E&P companies as a crash in oil prices, such as the one experienced, can generate large, non-cash charges on the profit and loss statement. Moreover, even without that, Ebitda doesn’t tell you how much cash the company is retaining. Here are recent aggregate numbers for 54 E&P companies sampled from the Bloomberg Terminal.

Shale’s treadmill of spending every dollar earned (plus some more if capital markets obliged) has been fantastic for U.S. oil and gas production, but less so for returns. Shale’s vaunted experience curve is a factor here, says Matt Portillo, a managing director at TPH. As companies have shifted from basin to basin, learning by doing and driving down costs per barrel, so the sunk capital in older positions has become a drag on returns.

Fixing that means easing up on the land-grab and showing investors there’s some actual profits to be made and distributed. There have been tentative signs of this already, with some E&P companies instituting buybacks or even dividends. Leverage has been coming down, and the sector has just about covered organic capex — stripping out acquisitions — from operating cash flow for three quarters in a row, according to Sanford C. Bernstein. Just as important, some firms have begun to shift executive pay toward returns-based incentives rather than just grow-at-all-costs benchmarks (there is still a lot to do on this front, though).

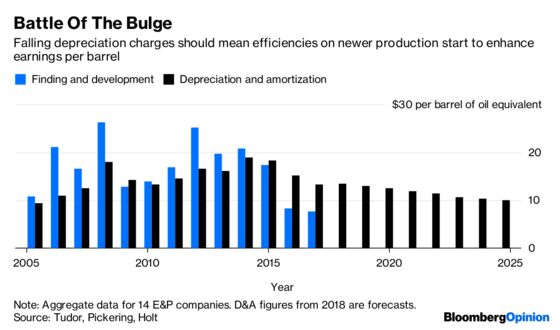

Continuing to do so should enhance free cash flow and returns. Moreover, as the legacy of the earlier land-grab and drilling frenzy fades, so depreciation charges should moderate, bringing them closer to finding and development costs and making earnings multiples more meaningful.

Investors have made their displeasure felt when E&P companies show signs of not getting with the program. A series of capex budget increases on second-quarter earnings calls did not go over well, with Occidental Petroleum Corp.’s early August sell-off a prime example.

So it’s pretty clear what sort of message E&P bosses ought to be delivering (especially as oil prices have cooled off somewhat). Tight reins on spending and an emphasis on free cash flow aren’t great for oilfield services firms looking for a rebound; Halliburton Co., in particular, could use some signs of a less-thrifty 2019. But on the earnings calls just now getting underway, discipline should be a crowd-pleaser.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2018 Bloomberg L.P.