E-Commerce Stocks Face Lofty Hopes After Pandemic-Fueled Demand

E-Commerce Stocks Face Lofty Hopes After Pandemic-Fueled Demand

(Bloomberg) -- E-commerce stocks have been among Wall Street’s standout performers during the pandemic, but the group’s massive share-price gains could be at risk if their results fail to live up to elevated expectations, analysts said.

Online retail has seen a surge in demand as the coronavirus shut down brick-and-mortar rivals. As a result, many stocks have doubled, tripled or seen even larger gains since March, when shelter-in-place orders were issued across the U.S. Often, the rally far eclipses the degree to which analysts have been raising their expectations for sales growth.

“Many e-commerce companies are now priced for perfection, and while they have this fundamental tailwind, the moves have been based more on momentum than fundamentals,” said Brian Yarbrough, a consumer analyst at Edward Jones, in a phone interview. “People have piled into names that are seen as COVID safety plays, and the advances have been awfully fast and awfully big. I’m not sure how many will be able to justify the moves; you’d have to see very outstanding results for further upside.”

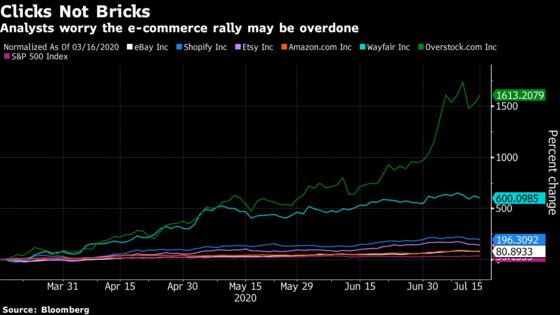

Among specific stocks, eBay Inc. is up 120% since a March low, while Shopify Inc. has climbed 195% and Etsy Inc. has more than tripled. Amazon.com Inc. is up about 80% from its own March low, a rally that has added roughly $660 billion to the company’s market capitalization -- a gain that is by itself larger than all but five components of the S&P 500.

Other names have seen even more pronounced moves, with Wayfair Inc. up more than 800% and Overstock.com’s rally topping 1,500%.

For 2020, all have vastly outperformed the S&P 500, as well as retail overall.

There’s no dispute that the pandemic has been good for online sales. Bloomberg Intelligence calculated that the penetration of digital U.S. retail sales “could double by 2024,” a trend accelerated by coronavirus-related store closings. Citi also expects online retail will continue to gain share. While total U.S. retail sales “are expected to be only 1% above 2019 levels” in 2022, “e-commerce is expected to increase 43%” while brick-and-mortar retail falls 4%, the firm wrote, citing eMarketer forecasts.

Despite that rosy outlook, Citi also cautioned about the rallies in names like Wayfair. Last month, it wrote companies that “benefitted from the shelter in place orders” are the group “that makes us most nervous.” Citi’s biggest question is: “will COVID-19 cause a large enough secular shift in demand to justify the multiple expansion?”

Wayfair is scheduled to report second-quarter results in early August. Currently, Wall Street is expecting revenue of $3.87 billion for the home-goods retailer in the quarter, which would translate to year-over-year growth of about 65%. While the consensus has risen nearly 40% over the past three months, according to data compiled by Bloomberg, the ratcheting up of expectations has not kept up with the stock. The average analyst price target for Wayfair is about $186, or 13% below its share price.

The average targets for Etsy and eBay are also below the share price. For Amazon, the degree to which the share price exceeds the average target is near a multi-year high.

©2020 Bloomberg L.P.