(Bloomberg Opinion) -- Round and round the DuPont merry-go-round of financial engineering we go.

The chemicals giant agreed on Sunday to sell its nutrition and biosciences division to International Flavors & Fragrances Inc. via a tax-friendly Reverse Morris Trust transaction that values the business at about $26 billion. DuPont de Nemours Inc. will receive a one-time $7.3 billion cash payment and its shareholders will own 55.4% of the combined entity.

This is just the latest in a long line of dealmaking by DuPont chairman Ed Breen, who earned the respect of the investing world for salvaging Tyco International from scandal in part by breaking it up several times. At DuPont, he’s helped orchestrate a complicated merger with rival Dow Chemical and a subsequent three-way split. After some rejiggering of the combined companies’ various assets amid pushback from activist investors, DuPont this year spun off the Dow Inc. commodity-chemical business and the Corteva Inc. agricultural-products company. Breen may not be done tinkering with DuPont’s portfolio after the International Flavors deal; Bloomberg News has reported that DuPont is also evaluating a divestiture of its transportation and industrial-chemicals unit.

The results of all this maneuvering have been just so-so. Dow is up about 9% since the March record date for its separation, lagging the S&P 500 Index and the benchmark’s materials sub-group. Corteva has slumped nearly 6% since its May debut. DuPont itself is down more than 14% so far this year. That’s partly a reflection of the sheer amount of time it took to orchestrate this complicated musical chairs.

The merger with Dow was announced four years ago, and the interim waiting period can create a sort of spin purgatory as investors hold off on rewarding a soon-to-be-simpler company with a valuation lift until all the paperwork is signed. And when a process takes that long, you’re bound to become a victim of bad timing. Dow and Corteva were spun off into a terrible market for chemicals as the U.S.-China trade war and a slowing economic backdrop weighed on demand and profit margins. Moody’s Investors Service this month issued its 2020 outlook for the North American and EMEA chemical sector, calling for an average Ebitda decline of about 5% amid soft commodity prices and weak investment trends. DuPont shares, meanwhile, also have been dragged down by its legal fight with a prior spinoff, Chemours Co., over liabilities linked to PFAS, the so-called forever chemical that was used in the manufacturing of Teflon.

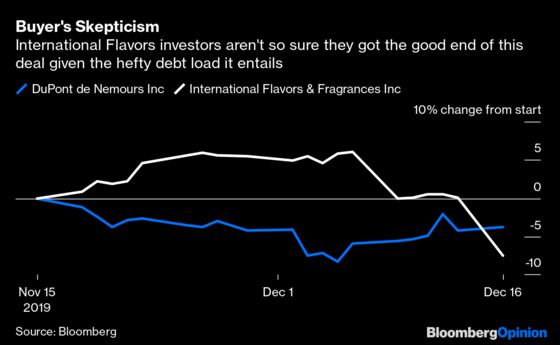

Breakup enthusiasts would tell you the share slump might have been worse if these businesses were still bundled together and one management team was trying to oversee their competing capital requirements and growth profiles. There’s certainly a logic to this latest deal. Nutrition and biosciences is DuPont’s largest division and has one of the more attractive growth profiles, but DuPont clearly wasn’t getting credit for this business in its stock.

The deal with IFF values the DuPont unit at more than 18 times its adjusted Ebitda in the past year, according to data compiled by Bloomberg. That’s well above what the parent company commands. At the same time, there’s a reason the nutrition and biosciences unit commands a higher valuation. The removal of this generally stable business may make it harder for DuPont to prove that its earnings and sales growth can rise above economic volatility.

If DuPont follows through on carving out the transportation and industrial unit as well, that would help limit its exposure to the swings in the automotive industry, which has been a particularly tough market of late. But it’s unclear what the endgame is here. There’s something deeply unsatisfying about a company using yet more breakups to fix a valuation disconnect that its first round of breakups was meant to rectify. Eventually, you run out of assets to sell or spin off.

Tyco eventually merged with Johnson Controls years after Breen had moved on, and the combined company took the latter’s name.

To contact the editor responsible for this story: Beth Williams at bewilliams@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Brooke Sutherland is a Bloomberg Opinion columnist covering deals and industrial companies. She previously wrote an M&A column for Bloomberg News.

©2019 Bloomberg L.P.