Oil Nears Point That Could Trigger a Wall Street Sell-Off

Is a historic crash in crude oil about to repeat itself?

(Bloomberg) -- As computer screens flash red for energy markets from Houston to Singapore, oil traders are urgently asking themselves one question: is a historic crash about to repeat itself?

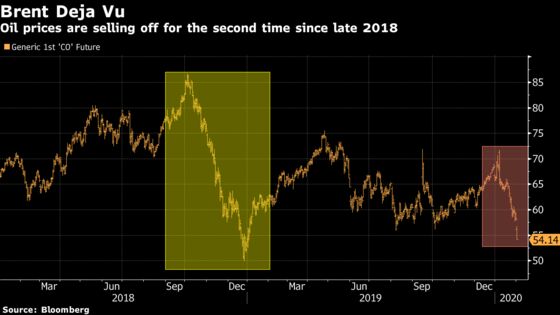

The meltdown caused by the Chinese coronavirus outbreak is increasingly reminiscent of a plunge that happened just over a year ago. In October 2018, a sell-off across commodity markets left Wall Street banks racing to cover insurance policies, such as options contracts, that they had written to oil producers, sparking a new wave of selling that ultimately caused prices to tumble by more than 40% over two months to $49.93 a barrel.

Brent crude, the global oil benchmark, has fallen by as much as 25% to a one-year low of $53.85 a barrel. The danger zone for a similar financial sell-off starts around $50 a barrel for Brent, according to Greg Newman, head of Onyx Capital Group, an oil market-maker based in London.

“If this is to happen then, yes, the option sellers will scramble to sell futures to cover their positions,” he said.

Though oil prices so far haven’t been driven by Wall Street selling, but rather by the collapse in Chinese oil demand, traders are alert to the potential for a vicious selling cycle. It’s what’s known on Wall Street as “negative gamma” event -- the Greek letter labeling a gauge of how sensitive options contracts are to price moves in the underlying asset.

When an oil producer, such as a U.S. shale company or the Mexican government, wants to lock in, or hedge, the price of the commodity, it buys insurance from a Wall Street bank. The insurance, in the form of an option contract, gives the holder the right to sell crude at a predetermined price and time. In simplistic terms, the banks manage their own exposure to the options they have written by selling futures. The closer the price of oil falls to the insured level, the more futures Wall Street has to sell.

In the past, similar situations have generated a dramatic sell-off: as prices drop beyond a certain level, banks frenetically sell futures to manage their options exposure. That drives down prices and brings more options into the danger zone, forcing even more selling from Wall Street, which pushes prices even lower.

Even OPEC is on alert for a potential vicious “negative gamma” event. As the cartel weighs how to respond to the drop in prices, the potential of a financially driven sell-off is one factor it’s considering, according to one OPEC delegate, who asked not to be named because the deliberations are private.

OPEC officials gathered in Vienna on Tuesday to review the oil market after Brent and West Texas Intermediate prices plunged to the one-year low. The gathering, which is expected to conclude on Wednesday, would be a key input for OPEC ministers to decide whether to call an emergency meeting.

For all the risk as oil prices drop, there are a number of specific differences between the current sell-off and what happened in late 2018, traders say. Banks sold options at a wider range of prices, limiting the chance the slump triggers a sudden sell-off. For example, the insurance that the Mexican government has bought from Wall Street is at a lower price than the hedges that many U.S. shale producers, like Occidental Petroleum Corp., have acquired. Moreover, Petrobras, the Brazilian state-run oil company, which hedged millions of barrels of oil in 2018, hasn’t done so this time.

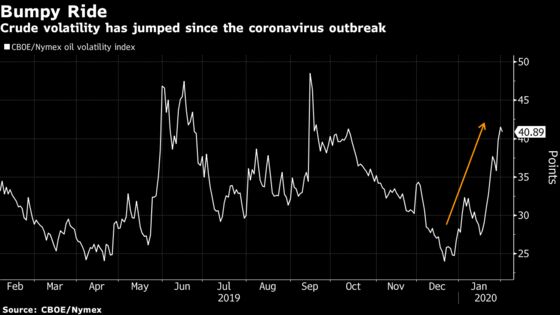

Still, the options market is starting to price some trouble: nowhere is the risk of sharp moves clearer than in crude volatility. A gauge of WTI volatility closed at its highest level in more than four months on Monday.

Although options traders are baking in expectations of bigger price moves, there are again some contrasts to late 2018. Put skews -- the premium paid for bearish put options over bullish call options -- have remained stable in recent days. In 2018, those gauges jumped to their most bearish in at least 5 years as banks raced to cover their hedges.

The price of WTI has fallen below the strike of over 200,000 barrels of producer puts during the past two weeks, Standard Chartered Plc analysts said in a note on Tuesday, adding that half the volume was in the $51-$54/bbl range for WTI. “We think $50 a barrel might prove a robust floor for WTI as gamma hedging effects are likely to be substantially less powerful.”

The market, nonetheless, is contending with imperfect information. The details of some of the largest hedging programs, such as the Mexican one, are secret, leaving everyone, from OPEC officials to Wall Street traders, guessing where the price trigger for a sell-off may lay.

“If there are large producer hedge programs and the price converges to the level of the strike at which hedges were placed, the providers of the put option will in turn manage their exposure by selling futures,” said BNP Paribas oil analyst Harry Tchilinguirian.

To contact the reporters on this story: Javier Blas in London at jblas3@bloomberg.net;Catherine Ngai in New York at cngai16@bloomberg.net;Alex Longley in London at alongley@bloomberg.net

To contact the editors responsible for this story: David Marino at dmarino4@bloomberg.net, Mike Jeffers

©2020 Bloomberg L.P.