(Bloomberg Opinion) -- The European Union’s aspiration to be a pacesetter in the global fight against the climate crisis is laudable. Even better, the bloc’s leaders want to bake financial innovation into their plans, giving their member countries (and companies and the region’s financial industry) a leg up in the rush to fund infrastructure projects that may literally save the planet.

But no matter how commendable those intentions are, the architects of the European Green Deal should resist any temptation to let governments keep the borrowing they’ll need to finance those initiatives off their books.

The ambitious plan to make the 27-nation group carbon neutral by 2050 will cost a ton of money. Curbing more of the emissions from cars, trucks and factories, improving air quality and crafting a more environmentally friendly agriculture industry is expensive. But long-dated money has never been cheaper.

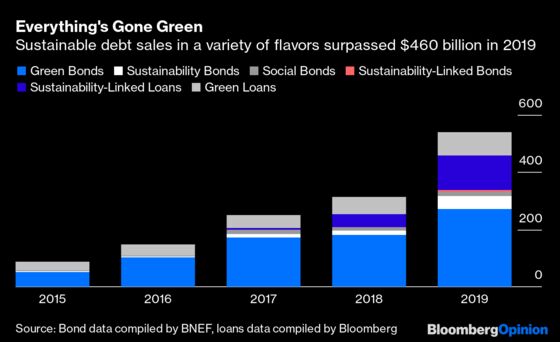

Moreover, demand for sustainable debt is growing. Investors are clamoring for green investments to sate their newly found appetite for climate-friendly securities, as customers ask for environmental, social and governance concerns to be included in portfolio construction. France has been at the forefront of European sovereigns selling green bonds. Last year, the Netherlands became the first AAA-rated country to issue debt specifically to finance environmentally friendly projects. The German government plans to join the party in the second half of this year with the explicit intention of establishing, “a liquid, green interest-rate reference for the euro area.”

So Thierry Breton, the European commissioner for the internal market, was right to point out last month that the bond market offers a cheap way to finance the EU’s objectives, especially with the European Central Bank having restarted its bond-buying program and standing ready as a buyer of first resort. His prodding for people to think creatively is also welcome; his marching orders at the Commission include coming up with a long-term industrial strategy for the bloc, which will test his powers of imagination. But Breton’s suggestion that the EU could exclude debt raised for green projects from deficit calculations goes a step too far.

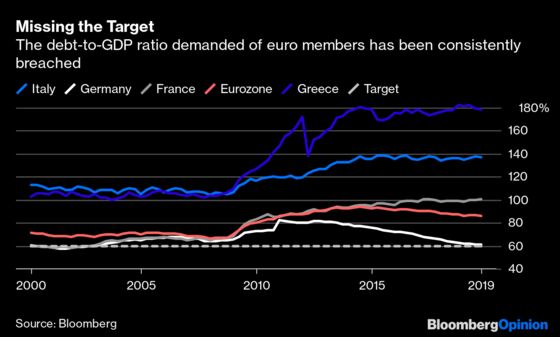

It’s easy to see the attractiveness of giving green bonds an exemption on government balance sheets. The target of limiting the ratio of debt to gross domestic product at 60% or lower has proven to be impossible for almost all of the euro participants who are supposed to adhere to it. Only Germany has recently fallen back into compliance with the goal.

So accounting trickery that moves the monetary goalposts to conceal the cost of combating the climate emergency may be politically expedient and fiscally attractive. That doesn’t make it excusable. Imagine the uproar if companies were allowed to borrow money for green projects without accounting for that increased debt on their balance sheets. The same strictures must apply to governments, otherwise Europe’s sovereign debt crisis could be reignited with a vengeance.

Breton’s comment to the Euractiv news service that green borrowing “could be de-consolidated” may not gain any traction. As well as being late to the green bond bonanza, Germany remains skeptical about expanding the mission statement of the EU and its various agencies to include saving the planet. But the notion that debt raised to do good should get special treatment serves to highlight the limits that even the most creative thinking needs to observe.

Enormous strides have been made in recent years to take the risk of global warming seriously, with environmentalists winning over the minds as well as the hearts of many climate skeptics by corralling science and data in support of their claims. Any attempt to hide the true cost of greening the economy will rapidly backfire. Better to make the argument that, as expensive as it is, combating climate change is something nations can’t afford not do to.

To contact the editor responsible for this story: Melissa Pozsgay at mpozsgay@bloomberg.net

This column does not necessarily reflect the opinion of Bloomberg LP and its owners.

Mark Gilbert is a Bloomberg Opinion columnist covering asset management. He previously was the London bureau chief for Bloomberg News. He is also the author of "Complicit: How Greed and Collusion Made the Credit Crisis Unstoppable."

©2020 Bloomberg L.P.