Dick's Sporting Goods Plunges as Analysts Weigh Turnaround

Dick's Sporting Goods Plunges as Analysts Weigh Turnaround

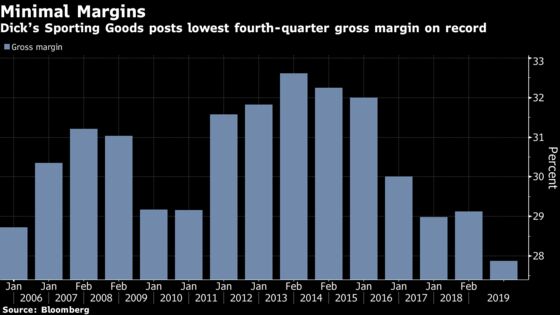

(Bloomberg) -- Dick’s Sporting Goods Inc. sank by the most in 19 months on Tuesday after the retailer’s quarterly gross margin and full-year profitability outlook fell short of Street expectations, and as management decided to remove hunting gear from some stores.

Investment initiatives in more private label products, e-commerce enhancements and distribution centers, have pressured gross margins more than analysts expected. That’s expected to continue, with Dick’s expecting its fiscal 2020 earnings to reflect incremental investment spending in the ballpark of $30 million, or 23 cents per share.

The continued pressure on profitability has analysts questioning the time frame of the company’s turnaround, and fearing that the shares have little chance for upside for now.

The stock is down as much as 12 percent to the lowest intraday since January 24. Sports-related retailing peers Foot Locker Inc., Hibbett Sports Inc., and Sportsman’s Warehouse Holidngs Inc. are all lower in sympathy.

Here’s what analysts were saying ahead of the company’s 10:00 am conference call:

Bloomberg Intelligence, Chen Grazutis

- “Continued pressure on gross margin in 4Q suggests Dick’s has returned to deeper discounting to drive both in-store and e-commerce traffic, raising questions about whether a potential turnaround is imminent or may take longer than projected”

- Shift to more private-brand sales and other initiatives like elimination of small brands should have improved profitability, but instead gross margin missed estimates by about 100 basis points

- “The real concern becomes what has Dick’s had to do in order to get traffic in-store and to its e-commerce sites”

- Management needs to present “a clearer path on how to protect margins in order to gain back investors’ confidence”

Guggenheim, Steven Forbes

- Gross margin miss is “a negative to sentiment”

- Management’s initial 2019 guidance implies 20-40 basis points of EBIT margin erosion and a 1-7% decline in EBIT

- While free cash flow rose 90% in 2018 to $500m, it likely normalizes around $350m this year due to the expected decline in Ebitda; increase in capex; and the potential working capital build associated with strategic investments (e-commerce fulfillment centers)

- Although Dick’s remains well positioned for share gains, “the trajectory of the company’s EBIT margin profile makes it difficult to envision share price out-performance”; rates neutral

Stifel, Jim Duffy

- Store level traffic challenges continue to pressure the model

- Views the SG&A-driven EPS beat as “low quality” given gross margin shortfall and mid- to high-single digit store-level comp. sales decline

- “Against expectations of favorable weather, a solid consumer environment, and product mix benefits, the results and outlook do not change our overall cautious view on the stock”

- “While there is considerable value in the market leadership position and thoughtful investments to extend DKS’s position, we do not see sufficient upside from current levels to recommend shares”; rates hold, price target $34

Baird, Peter Benedict

- In-line EPS, but P&L stabilization “remains elusive” as year EBIT margins are implied “down more,” with the company noting about $30m of business transformation investments

- Maintains neutral, despite shares being “relatively inexpensive’

Consumer Edge Research, David Schick

- “We believe the two-year stack on critical gross margin run rate and investments impacting 2019 guidance are issues that will be part of the investor conversation today”

- Rates equal-weight, price target of $37

RBC Capital Markets, Scot Ciccarelli

- Growing contribution of e-commerce sales into the mix implies that store-level comparable sales fell by about 5.4 percent in the quarter, “despite a fairly robust overall retail environment”

- “Store level comps need to improve or the box will continue to deleverage”

- While some of the 4Q gross margin pressure likely came from the calendar shift, the 4Q decline occurred after 2 straight quarters of margin improvement in the 70-80 bps range

- Rates sector perform, price target of $35

- Dick’s Sporting Goods year EPS forecast $3.15 to $3.35 includes approximately $30 million, or 23 cents per diluted share, of net investments in business transformation initiatives; this may not compare with estimate $3.34 (range $2.80 to $3.60)

--With assistance from Karen Lin.

To contact the reporter on this story: Janet Freund in New York at jfreund11@bloomberg.net

To contact the editors responsible for this story: Catherine Larkin at clarkin4@bloomberg.net, Scott Schnipper

©2019 Bloomberg L.P.