This Fracker Finds It Easier to Buy Itself

This Fracker Finds It Easier to Buy Itself

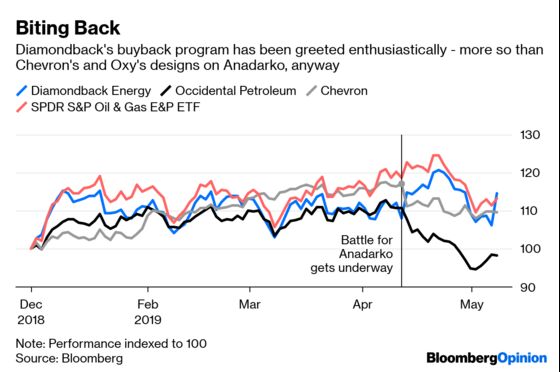

(Bloomberg Opinion) -- What with the drama of the takeover battle for Anadarko Petroleum Corp., just buying back stock in the shale patch can seem humdrum. Judging from the reaction to Diamondback Energy Inc.’s new $2 billion repurchase program, though, investors don’t necessarily see it that way.

Diamondback is absorbing its own big deal, the takeover of Energen Corp., which closed in November. First-quarter results, released Tuesday evening, suggest it is progressing well, with Diamondback beating the consensus earnings forecast and meeting expectations on production despite capital expenditure coming in a bit lower than anticipated.

On the topic du jour for activists in the sector – namely, overhead – Diamondback is exemplary. SG&A expense averaged $1.21 per barrel of oil equivalent over the past four quarters, less than half the average for large-cap E&P companies (see this). It was just $1.14 in the first quarter.

The other big topic, not just for activists, is M&A, with the shadow of Anadarko looming large. Diamondback’s own stock jumped when Chevron Corp.’s offer was announced, and management fended off several questions on Wednesday morning’s call trying to ascertain whether Diamondback would be open to a big deal of its own. They may have had Scott Sheffield in mind; the recently reinstated CEO of Pioneer Natural Resources Co. touched off a rout in his company’s stock Tuesday morning when he said he hadn’t “come back to sell the company.”

At a time when investors are demanding better returns and see companies such as Occidental Petroleum Corp. stretching to pay big premiums to consolidate the Permian basin, the last thing they want to hear is a CEO declaring their company off limits (Sheffield walked back his statement in an interview with Bloomberg News later that day).

So for Diamondback, reticence on M&A can be its own reward. Backing it up, however, is that new buyback program. The great thing about this is (a) it’s a lot easier to buy your own company, and (b) it sends the right signal about where any excess cash will go.

Based on Diamondback’s guidance, including anticipated proceeds from announced disposals, free cash flow after dividends should cover about $1.5 billion of potential buybacks through the end of 2020, assuming a $55 oil price. However, using consensus Ebitda estimates, there is potential for more. Net debt was 1.7 times Ebitda at the end of March, and guidance would put that at around 1.2 times by year end (absent buybacks). Taking it to 1.4 times and holding it there would imply capacity for more like $3.1 billion of buybacks through the end of next year, equivalent to almost 18 percent of Diamondback’s current market cap.

In reality, consensus forecasts for any oil company aren’t to be taken as gospel. Moreover, even if that math were to pan out, Diamondback would likely divert some of it to more acreage and drilling. Still, when asked about the interplay of oil prices and free cash flow on the earnings call, Diamondback said there wouldn’t be “a wild swing up” in the rig count if oil prices increased, but it might swing down if oil fell sharply. It’s not the most dramatic speech you’ll hear in shale land right now, but it is the right one.

To contact the editor responsible for this story: Mark Gongloff at mgongloff1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Liam Denning is a Bloomberg Opinion columnist covering energy, mining and commodities. He previously was editor of the Wall Street Journal's Heard on the Street column and wrote for the Financial Times' Lex column. He was also an investment banker.

©2019 Bloomberg L.P.