Deutsche Bank Cut Wirecard Ties as Its Fund Managers Went All In

The complicated relationship of Germany’s financial elite with a company that imploded in a scandal last month.

(Bloomberg) -- In late 2018, as Deutsche Bank AG executives mulled the future of their troubled lender, Chairman Paul Achleitner encouraged them to emulate a payments firm that had become a wunderkind of German finance: Wirecard AG.

The two companies were already close. Deutsche Bank was a key lender to Wirecard and its chief executive officer, Markus Braun, who also sat on one of its regional advisory boards. Andreas Loetscher, an Ernst & Young partner who had overseen several audits of Wirecard’s results, had recently joined Deutsche Bank as chief accounting officer. DWS, the bank’s asset-management unit, was a shareholder.

Yet behind the scenes, doubts were growing whether the fintech’s success was for real. Deutsche Bank’s investment bankers argued its accounts were opaque and the stock overvalued, and risk managers sought ways to cut their exposure without rattling markets. Over the course of the following year, Deutsche Bank unwound or hedged most of some $300 million it had agreed to lend to Braun and his firm -- while its asset management arm kept piling in, an analyst upgraded the stock and its bankers helped the firm raise debt.

This story of Deutsche Bank’s ties to Wirecard is based on accounts of people with direct knowledge of the events who spoke on condition of anonymity. It spotlights the complicated relationship of Germany’s financial elite with a company that was belittled at first, then admired and eventually bedeviled when it imploded in a spectacular accounting scandal last month. Now Deutsche Bank is coming full circle, considering a financial lifeline for parts of the firm that only last year approached it about an all-out merger.

A spokesman for Deutsche Bank declined to comment on the lender’s ties to Wirecard.

Wirecard’s Story

Wirecard’s allure for the world of German finance is hard to overstate. Started as a payments provider to gaming and adult entertainment websites, it was the butt of jokes at first on the executive floors of some German lenders. Yet as the country’s financial industry struggled to adapt to tighter regulations and negative interest rates after the 2008 financial crisis, the startup from the suburbs of Munich somehow bucked the trend.

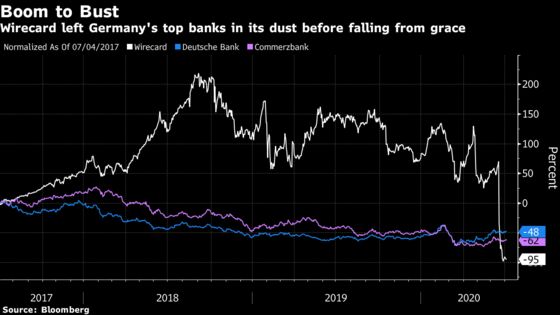

Suddenly here was a young company that seemed to enjoy spectacular growth by applying technology to the plumbing of payments, and shareholders loved it. The company’s market value had exploded since the financial crisis, eclipsing 150-year-old Deutsche Bank. By late 2018, Wirecard replaced Commerzbank AG in Germany’s benchmark DAX Index.

Achleitner, at the meeting in Hamburg in late 2018, asked why Deutsche Bank’s transaction bank wasn’t getting the same attention as Wirecard’s. He was looking to bolster Deutsche Bank’s own payment business after naming Christian Sewing CEO earlier that year -- an executive with extensive experience in corporate banking.

Shortly after that meeting, in January 2019, the Financial Times published the first in a series of articles alleging accounting irregularities at a unit of Wirecard, sending the shares into a tailspin. The payments firm -- and even regulators -- brushed it off as the work of short sellers seeking a quick profit, but the FT stood by its reporting throughout.

At Deutsche Bank, some executives grew alarmed, including Garth Ritchie, the head of investment banking at the time. Ritchie’s skepticism had arisen in part from conversations with hedge-fund clients that had conducted their own research into the firm’s workings, and who had been betting against the stock. His unit oversaw a 150 million-euro loan to Braun that was secured by Wirecard shares, so if the shares fell, the bank could lose a lot of money.

Risk managers led by Stuart Lewis, Deutsche Bank’s chief risk officer, were also worried. The lender had agreed to provide around 120 million euros to Wirecard as part of that firm’s revolving credit facility, but the payments company was expanding very rapidly and Deutsche Bank didn’t fully understand all the factors at play. They reduced their exposure and increased their hedge in the wake of the FT story.

Kirch Lawsuit

Lewis also shared Ritchie’s concern about the margin loan to Braun. The debt was due for renewal at the end of 2019, but some traders wanted to get rid of it before. Yet doing so could send a message to markets that Germany’s largest lender had lost confidence in the company and might push Wirecard over the edge. Deutsche Bank itself would be at risk of another billion-dollar lawsuit like the one with the heirs of of Leo Kirch over the collapse of his media group, which dragged on for more than a decade until 2014.

The allegations in the FT were weighing on Wirecard’s shares, but the company was still more valuable on the stock market than Deutsche Bank. And so, in the spring of last year, its executives were discussing an audacious step that would have given them a way out: a full-fledged merger with Deutsche Bank. They approached the Frankfurt lender, but the bank quickly ended the exploratory talks.

Wirecard did score a victory around that time in efforts to restore market confidence. In April, SoftBank Group Corp., the Japanese telecommunications operator turned tech investor, agreed to put 900 million euros into the German company, giving a boost to the stock. Nooshin Nejati, an equity analyst at Deutsche Bank in Frankfurt, changed her rating on Wirecard to buy from hold the following month and predicted that its shares would soar about 40% to 200 euros within a year.

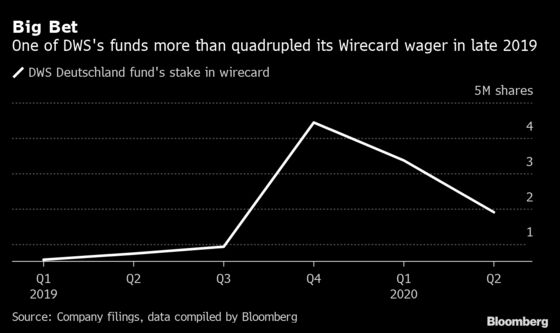

Fund managers at DWS were also bullish on Wirecard. Over the course of the year, the firm increased its holding from less than 2 million shares to over 7 million. The biggest purchase came right after the Wirecard’s share price plunged more than a fifth in the span of a few days following another critical FT report. Stock pickers led by Tim Albrecht went all in.

DWS and Albrecht declined to comment. The investment firm said last month it plans to file a lawsuit against Wirecard and Braun.

Albrecht saw the October selloff as a chance to lock in big gains down the road, he said in a recent newspaper interview. His 4.1 billion-euro DWS Deutschland fund upped its stake by more than 3.5 million shares between September and December 2019, according to data compiled by Bloomberg and company filings. DWS Aktien Strategie Deutschland and DWS ESG Investa both more than doubled their holdings over the same period.

Just as they piled in, executives in Deutsche Bank’s twin towers across the street from DWS made up their mind about Wirecard. Softbank, whose April announcement was seen as a sign of confidence in Wirecard, had since gotten cold feet and was setting up a complex transaction to sell off the investment and avoid putting up money itself.

Deutsche Bank’s investment bankers had been offered, informally, a chance to help on the convertible bond Wirecard was planning to sell as part of the Softbank agreement, but they declined because they didn’t want the risk on their books. They did help Wirecard raise a separate, 500 million-euro bond in September, but that debt was sold on to other investors.

By early November, Deutsche Bank’s risk managers decided that they wouldn’t renew the margin loan to Wirecard CEO Braun. They rolled over part of the debt and set up a repayment plan. Braun eventually got another loan, from Oldenburgische Landesbank, a small regional lender backed by private equity investors including Apollo Global Management, according to people familiar with the matter.

When Wirecard spiraled toward insolvency this spring -- after admitting that more than $2 billion that it had claimed to have in assets probably didn’t exist -- the loan to CEO Braun was no longer on Deutsche Bank’s books. And while the firm is among a group of 15 lenders owed some 1.6 billion euros by Wirecard, its actual exposure is closer to 70 million euros, assuming the credit facility was 90% drawn down. By comparison, Commerzbank, ABN Amro Bank NV and ING Groep NV are each owed more than twice as much, Bloomberg has reported.

But Deutsche Bank remains exposed on other fronts. DWS needs to explain losses from the investment to its clients. Loetscher, Deutsche Bank’s chief accountant, is the target of a criminal complaint for his role in Wirecard’s audits while he was working for E&Y.

“There are many unresolved questions around Wirecard,” said Sebastian Kraemer-Bach, a spokesman for Deutsche Bank in Frankfurt. “We highly appreciate working with Andreas Loetscher,” he said, adding that the presumption of innocence applies. Loetscher declined to comment.

Deutsche Bank is now considering buying Wirecard’s banking operations, which have been ringfenced from the rest of the payments company by BaFin, the German regulator. Options include taking on pieces of Wirecard Bank or the unit in its entirety, people familiar with the matter said, adding that the lender is still debating other ways to help Wirecard Bank and hasn’t made a final decision.

©2020 Bloomberg L.P.