Deutsche Bank’s Funding Costs Show Its Struggle to End Vicious Circle

Deutsche Bank’s Funding Costs Show Its Struggle to End Vicious Circle

(Bloomberg) -- Deutsche Bank AG is paying some of the highest rates among large banks to raise debt this year, highlighting a key obstacle in the lender’s turnaround effort.

Germany’s biggest bank this week sold $1.25 billion of three-year dollar bonds that pay 255 basis points over benchmark interest rates, according to a person familiar with the matter who asked not to be named. That’s almost twice what other European lenders have paid in recent months. Only Denmark’s Danske Bank A/S, which is grappling with a money laundering scandal, and Italy’s UniCredit SpA have paid similar or greater amounts.

A spokesman for Deutsche Bank declined to comment on the dollar bond sale.

Deutsche Bank is among dozens of lenders paying up to issue bonds that can absorb losses in a crisis in order to meet global regulations designed to end taxpayer-funded bailouts. Investors are demanding higher returns to lend money to Deutsche Bank as the firm grapples with a prolonged decline in revenue. Options under discussion if performance worsens include a government-brokered merger with domestic rival Commerzbank AG.

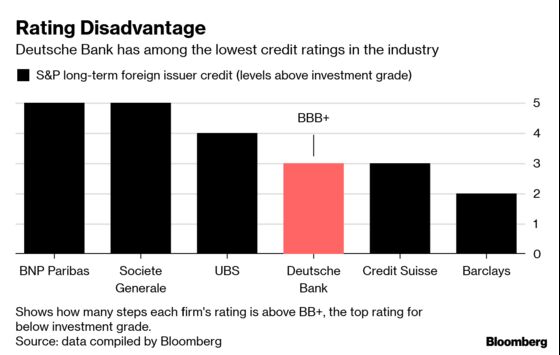

Finance chief James von Moltke said last year that the bank was caught in a “vicious circle” of declining revenue, sticky expenses, a lowered credit rating and rising funding costs. While the firm cut expenses last year, revenue and the price of funding remain a concern.

“A key priority for us now is lowering our funding costs and improving our credit ratings,” Deutsche Bank’s von Moltke said during a call with fixed-income investors last week. “We must not compromise on the strength of our capital, funding, or liquidity, but we have to prove that we can generate long-term, sustainable profitability.”

Deutsche Bank treasurer Dixit Joshi said said last week that it’ll issue as much as 11 billion euros ($12.4 billion) of the so-called senior non-preferred bonds this year. It reached a third of the target last week, selling about $4 billion of the notes in euros and sterling. It paid investors 230 basis points over benchmark interest rates for a seven-year euro bond, according to data compiled by Bloomberg. By comparison, French bank BNP Paribas SA last month offered 50 basis points less for equally-ranked notes that mature one year later.

Deutsche Bank is predominantly issuing short-term debt, which is less expensive than bonds due in more than five years, as it tries to rein in financing costs, said Jakub Lichwa, a credit strategist at Royal Bank of Canada in London. That’s a calculated risk because the bank will have to return to capital markets sooner while facing “the possibility of being locked out,” he said.

“Investors should not lose sight of the fact that Deutsche Bank’s overall risk is increasing, as longer term liabilities are rolled into shorter obligations,” Lichwa said.

Deutsche Bank’s offer to dollar investors of 255 basis points -- following initial talk of about 275 basis points -- compares with Nordic giant Nordea Bank Abp’s 108 basis-point deal in August. Danske Bank paid 260 basis points for senior debt in January when new money-laundering allegations were surfacing. The most expensive sale of senior non-preferred notes was executed by UniCredit SpA in November. Italy’s biggest bank paid 494 basis points in a private deal with Pacific Investment Management Co. at the height of the nation’s budget dispute with European Union officials.

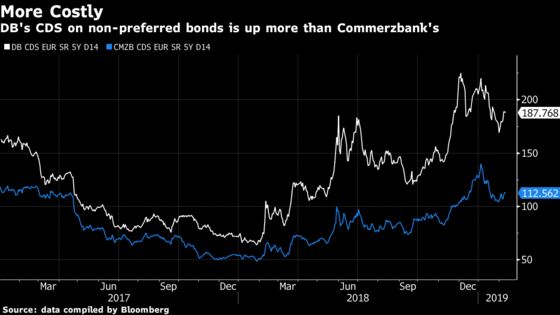

Deutsche Bank’s troubles are also reflected in the cost of insuring its debt against default. While credit-default swap contracts insuring against losses for five years have dropped from a two-year high, they’re still more expensive than that of peers like Commerzbank AG. Deutsche Bank said last week that credit-default swaps on safer senior bonds, known as preferred senior, will be available to be traded soon, and should be significantly cheaper.

--With assistance from Brian Smith and David Scheer.

To contact the reporters on this story: Steven Arons in Frankfurt at sarons@bloomberg.net;Thomas Beardsworth in London at tbeardsworth@bloomberg.net;Katie Linsell in London at klinsell@bloomberg.net;Yalman Onaran in New York at yonaran@bloomberg.net

To contact the editors responsible for this story: Dale Crofts at dcrofts@bloomberg.net, Christian Baumgaertel, Shelley Robinson

©2019 Bloomberg L.P.