Deposits In Jan Dhan Accounts Up 118% Over 21 Months

PMJDY deposits increased nearly eight-fold from September 2014 to May 2016.

The average deposit per account under Pradhan Mantri Jan Dhan Yojana (PMJDY)—a financial inclusion programme launched by Prime Minister Narendra Modi in August 2014– increased 118 percent from Rs 795 in September 2014 to Rs 1,735 in May 2016, according to IndiaSpend analysis of government data.

PMJDY accounts quadrupled (increased by 308 percent), from 53 million in September 2014 to 219 million in May 2016, while the proportion of accounts with no money in them–zero-balance accounts, as they are called–declined from 76 percent in 2014 to 25.7 percent in 2016.

This indicates that more Indians are being included in the formal financial system, and they are willing to keep their earnings in Jan Dhan accounts, along with payments coming in directly to those accounts from the Mahatma Gandhi National Rural Employment Guarantee Act (MGNREGA) and subsidy for liquefied petroleum gas (LPG).

PMJDY deposits increased nearly eight-fold (790 percent), from Rs 4,273 crore in September 2014 to Rs 38,048 crore in May 2016.

However, the average deposit in accounts apart from those with no money (zero-balance accounts) declined 32 percent– from Rs 3,427 to Rs 2,333 over the same period– showing that new account holders are putting in less money into their bank accounts than they did.

One of the basic things said against financial inclusion is that when the poor open bank accounts, the large majority of these accounts are actually zero-balance accounts and there are no transactions.In camp mode (when depositors were being signed up), banks had tables, a few people, chairs and forms; there was no arrangement for collection of cash, deposit of cash, taking care of cash; so basically accounts were opened in zero-balance mode.Dr Alok Pande, Director PMJDY

Dr Pande said people were proud to have an identity.

We persuaded banks to issue passbooks. You will not believe the dramatic impact; from about 79 percent zero-balance accounts in November (2014), zero-balance accounts dropped to 45 percent (August, 2015). One of the major things that created the push was that people love to see their own photograph, name, address in a passbook.Dr Pande

Direct benefit transfers from the government are coming through these (Jan Dhan) accounts. So, zero-balance accounts have come down automatically as money is put in these accounts.The average balance in non-zero-balance accounts has come down as people withdraw money from it and are still not used to the banking habit. Jan Dhan shows that the challenge for the system is to create this business of banking habit.Madan Sabnavis, Chief Economist, CARE Ratings.

In China, the amount of money that goes through the formal sector (banking) is around 70% and the informal sector (moneylenders) is 30%. The case is exactly opposite in India with only 30% going through the formal sector and 70% through the informal sector. Jan Dhan accounts will channelise these transactions through formal accounts or the banking system, which will help banks to provide the right products to the right person, leading to better financial inclusion.Soumya Kanti Ghosh, chief economic advisor, State Bank of India,

As subsidy payments through bank accounts rise, fewer accounts will be unused

Zero-balance accounts will decline as subsidy payments increase, said Ghosh.

In 2015-16, the government transferred Rs 61,824 crore ($10 billion) to 310 million beneficiaries of 59 central schemes, such as National Social Assistance Programme, Post Matric Scholarship For Scheduled Tribe, Fellowship Schemes of All India Council for Technical Education and Janani Suraksha Yojana.

India created financial history opening 18 million bank accounts in a week (between August 23 and 29 August, 2014), setting a Guinness World Record.

Zero-Balance accounts 76% to 25%

Lakshadweep Has Maximum Average Bank Deposits

The island territory of Lakshadweep has the maximum average deposit per account, Rs 8,824, and the maximum average deposit per non-zero-balance account—Rs 12,540.

Mizoram has the least average deposit per account, Rs 646, and the least average deposit per non-zero-balance account—Rs 998.

Jammu and Kashmir had the largest proportion of zero-balance accounts, 41.5 percent, on May 25, 2016, followed by Chhattisgarh (38 percent), Nagaland (36.4 percent), Andaman and Nicobar Islands (35.3 percent) and Mizoram (35.2 percent).

Chandigarh has the least zero-balance accounts, 13.9 percent, followed by Himachal Pradesh (14.6 percent), Tripura (15 percent), Goa (16.3 percent) and Punjab (17.5 percent).

Financial Inclusion accelerates under PMJDY

About 40 percent of India’s population is now outside the purview of formal banking.

Only 145 million households (58.7 percent) of 247 million in the country had access to banking services, according to Census 2011; 91 million rural households used the banking system, as did 53 million urban households.

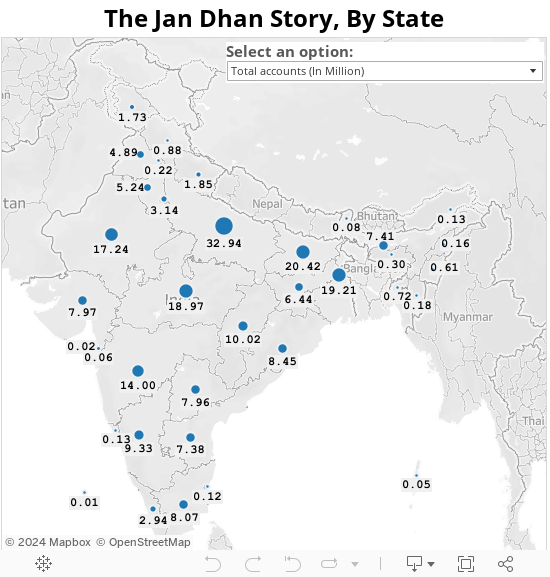

As many as 219.3 million PMJDY accounts were opened as on May 25, 2016; 134.7 million are rural and 84.6 million are urban accounts.

(Published in an arrangement with IndiaSpend)