Deluge of Debt Is Making Corporate America Riskier for Investors

Deluge of Debt Is Making Corporate America Riskier for Investors

(Bloomberg) -- Blue-chip U.S. companies are borrowing money at a record pace to make up for their plunging sales. That process is making corporate bonds riskier for investors.

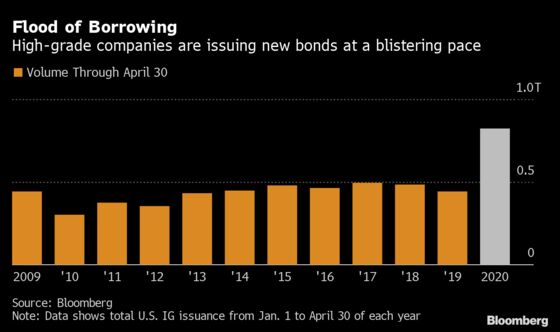

Boeing Co., the plane maker, sold $25 billion of bonds on Thursday, the largest offering of the year. Coca-Cola Co. issued $6.5 billion of notes this week. Offerings like these made April the busiest month on record for investment-grade corporate bond sales, totaling more than $300 billion, according to data compiled by Bloomberg.

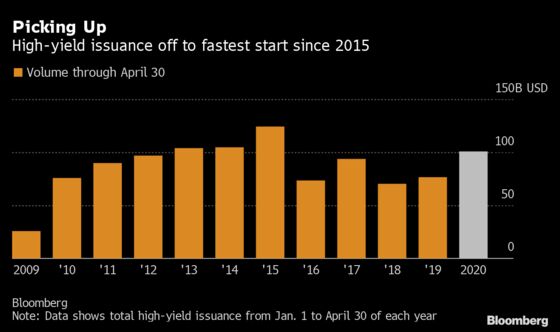

Junk-rated companies including Gap Inc. the clothing retailer, and Six Flags Entertainment Corp., the amusement park operator also borrowed in April, lifting total high-yield bond issuance by about 20% to more than $110 billion this year through the end of last month, according to Bloomberg data. An unusually high volume of junk-bond sales represents new borrowing instead of refinancing existing debt, according to a report last week from credit strategists at JPMorgan Chase & Co.

Read more in this week’s Credit Brief: A Flood of Debt; CLOs Take a Hit

By some measures, lending to corporations is becoming riskier. Companies are boosting their debt levels as their earnings fall, leaving them with fewer resources to pay interest on their growing debt burdens. That may be why investment-grade corporate bonds have gained just 1.4% this year through Thursday, lagging Treasuries’ 8.9% gains.

As the global Covid-19 pandemic spreads, the U.S. economy shrank at an annualized 4.8% pace in the first three months of the year, a contraction may intensify in the second quarter. To keep credit flowing amid the trouble, the Federal Reserve announced plans to buy company debt. That’s pushed down yields on investment-grade corporate bonds to an average of 2.67%, close to all-time lows. Even some junk-rated companies are getting cheaper financing.

“Fed support may ease a short-term liquidity crunch but it doesn’t cure credit risk,” said Bill O’Neill, senior portfolio manager at Income Research + Management. His firm is considering how to deal with bonds sold by energy, finance, and property companies that he worries might not survive the onslaught.

Companies are borrowing more to fill the gaps in their earnings. Morgan Stanley estimates that U.S. investment-grade issuance this year will total around $1.4 trillion, potentially topping 2017’s record of $1.41 trillion. Barclays estimates that corporations outside the financial sector will need to borrow $125 billion to $175 billion in additional debt just to cover negative free cash flow from the pandemic, according to an April 17 report.

The ratio of companies’ debt levels compared with a measure of their earnings, known as the net leverage ratio, is set to increase to around 3 times, according to Barclays estimates, a post-2008 financial crisis high. That rising relationship reflects the growing risk to money managers buying investment-grade bonds.

“You have to admit the world has changed from four months ago and therefore your portfolio probably can’t look the same,” said Kurt Halvorson, an investment-grade portfolio manager at Western Asset Management Company, which has $448 billion under management. “If there’s a business or a company we own that we think is at risk long term, then yes, we would sell our position there.”

Some investors aren’t worried about increasing debt levels, which may be temporary. Companies are building up more liquidity, which gives them more options in the future, said John McClain, a money manager at Diamond Hill Capital Management.

“One of the reasons we’re attracted to investment grade is because some of these businesses do have a number of ways to win and ways to survive,” McClain said. “You can cut capex, dividends, buybacks and acquisitions. These are very simple levers than can plug up a lot of the cash flow need.”

McClain favors companies that were in a strong position before the pandemic, and sees longer-term opportunities in the energy sector companies that survive the crisis, as demand rebounds in 18 to 24 months.

The swath of new investment-grade deals have so far been met with strong demand, and companies rarely lose access to the U.S. bond markets even in a crisis, Morgan Stanley analysts led by Felician Stratmann wrote in an April 24 report. Since 1995, there have only been 14 weeks where companies have sold less than $1 billion of bonds, excluding the last two weeks of the year and major holidays, they wrote. That represents less than 1% of history.

But an “unprecedented pace of issuance will leave a mark on U.S. corporate fundamentals,” they wrote. Companies will likely end up with higher debt loads, with borrowers in the consumer and industrial sectors among the hardest hit.

Many investors are proceeding carefully.

“Even though the Fed is buying, for us it really comes down to whether these companies are good investments given the valuations that there are today,” said Arvind Narayanan, senior portfolio manager on Vanguard’s active investment-grade credit strategies.

©2020 Bloomberg L.P.