Decade-Long High-Grade Bond Binge May Come to an End in 2019

Decade-Long High-Grade Bond Binge May Come to an End in 2019

(Bloomberg) -- It may be the end of an era. If all the pieces that suppressed U.S. investment-grade corporate bond issuance in 2018 remain in place, what has been a decade of heavy bond sales could come to an end in 2019.

Borrowers sold nearly $1.1 trillion of bonds in 2018, just short of 2017’s record $1.2 trillion. Analysts expect some of the main drivers of the decline -- corporate repatriation of cash, borrowing costs rising off of record lows, and broader uncertainty, somewhat offset by strong M&A-related supply -- to persist in the new year, affecting some sectors more than others.

Against a backdrop of volatile equity markets, rising Treasury yields, trade wars and turmoil in Washington, 2018 was the worst year for the U.S. high-grade bond market in a decade. As the market posted negative returns, credit spreads -- the risk premium on investment-grade debt -- widened 59 basis points and the cost to protect against default nearly doubled.

Here are the sectors that surprised and disappointed in 2018, and key trends to look out for in 2019:

Surprises

Health care. This sector was among the few that saw an uptick in supply in 2018 (about a 90 percent increase), mostly driven by strong M&A activity. M&A in this sector produced some of the largest deals of 2018 in investment grade -- $40 billion for CVS Health Corp.’s purchase of Aetna Inc., $20 billion for Cigna Corp.’s acquisition of Express Scripts Holding Co., and $15 billion for Bayer AG’s acquisition of Monsanto Co., to name a few. Analysts at Wells Fargo & Co. expect another active year in M&A in 2019, particularly within pharmaceuticals, but look for total supply across the sector to fall.

Retail. Supply increased about 13 percent in the retail sector in 2018, also partially thanks to M&A. Walmart Inc. printed $16 billion -- the sector’s largest deal of the year -- to fund its acquisition of Flipkart. Wells Fargo analysts predict a 38 percent decline in issuance for this sector in 2019, and expect that most new supply will fund debt refinancing and shareholder returns.

Disappointments

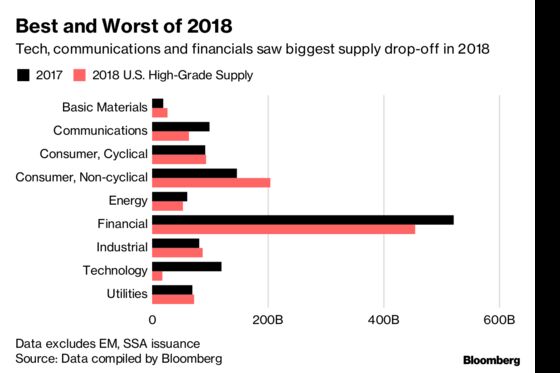

Technology. Tech companies priced about $18 billion of supply in 2018, falling more than $100 billion short of 2017’s number. Strategists at JPMorgan Chase & Co. attribute the decline to tax repatriation, changes in tax laws that left several companies flush with cash. Notably, some of the sector’s biggest players -- Apple Inc., Microsoft Corp., Oracle Corp., Broadcom Corp. and Qualcomm Inc. -- were absent from the primary market in 2018. Look for moderate issuance in this sector in 2019, as companies continue to benefit from repatriation.

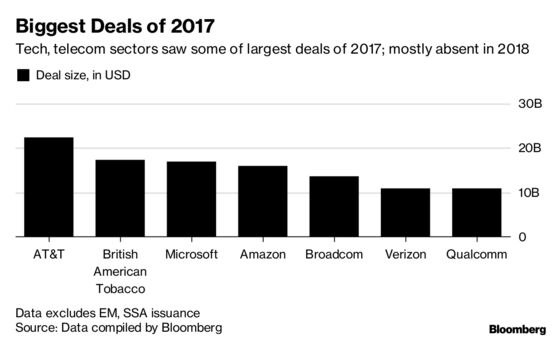

Telecommunications. A few large transactions drove telecom supply in 2017, setting it up to disappoint in 2018 -- and it did. Issuance fell 51 percent in 2018, lacking the $50 billion in supply provided by AT&T Inc. and Verizon Communications Inc.’s M&A-related funding in 2017. CreditSights says that technology, media and telecom (TMT) supply could be a “wildcard” next year, with M&A having the potential to add as much as $50 billion.

Financials. Financial issuance, which accounted for more than 40 percent of total investment-grade supply in 2018, fell about 13 percent, largely driven by a more than $50 billion drop in bank and diversified financial services supply and a $15 billion drop in REIT supply. CreditSights analysts look for an 8 percent decline in financials supply in 2019, and anticipate that refinancing will be a large driver of issuance. Strategists at Wells Fargo expect a 10 percent decline in REIT issuance in the new year.

Looking Ahead

- Strategists at Bank of America Corp., CreditSights, JPMorgan and Wells Fargo look for U.S. high-grade supply to fall in 2019, anywhere between 6.5 percent to 10 percent

- CreditSights expects TMT to bring more supply year-over-year in 2019, while issuance in most other sectors will fall

- JPMorgan, Bank of America expect lower overall supply to be partially driven by less M&A, higher funding costs, repatriation of cash

- JPMorgan lists trade uncertainties, less economic optimism as reasons for lower M&A activity in the new year. “The worst thing for M&A is uncertainty,” Bob Saada, PricewaterhouseCoopers LLP’s head of U.S. deals, said on Bloomberg TV last week

Note: Supply data covers syndicated SEC Registered and 144a USD-denominated, IG-rated bonds sold in the U.S. with a maturity of at least one year; $25par preferred share and SSA/EM deals are not included. Issuance stats are based on information compiled by Bloomberg News.

--With assistance from Allan Lopez and Brian Smith.

To contact the reporter on this story: Natalya Doris in New York at ndoris2@bloomberg.net

To contact the editors responsible for this story: Christopher DeReza at cdereza1@bloomberg.net, Christopher Maloney

©2019 Bloomberg L.P.