Dean Has Got Milk But Few Growth Prospects as It Hunts for Buyer

Dean Has Got Milk But Few Growth Prospects as It Hunts for Buyer

(Bloomberg) -- If Dean Foods Co. is serious about finding a buyer, it’s going to be a hard sell.

A fierce battle is playing out between Dean’s branded milk, such as DairyPure and TruMoo, and house brands sold by giant retailers like Walmart Inc.

That’s driven shares of the biggest U.S. milk producer to less than half of book value, its bonds to about 50 cents on the dollar, and its managers to consider selling all or part of the company.

Analysts have been skeptical that Chief Executive Officer Ralph Scozzafava can engineer a turnaround or find a viable buyer for Dean, given the falling demand for milk, the company’s rising costs and debts that total more than $900 million. Investors may not get much encouragement Tuesday when Dean is expected to report its fifth straight quarterly loss.

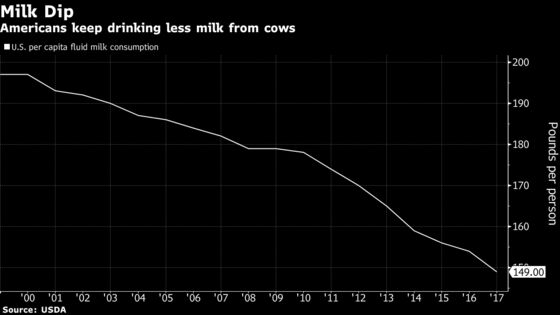

Dean makes money by being a low-cost supplier, and “they lost their way on that path, so much so that Walmart felt they could build a plant and be at a lower cost,” said Matt Gould, an analyst at Dairy & Food Market Analyst Inc. Meanwhile, changing diets have made milk less popular, and Dean is losing sales to retailers that sell their own milk as a loss leader.

The company said in February it hired advisers from Evercore Inc. and law firm Gibson Dunn & Crutcher to review its options, such as divesting units or forming a joint venture.

Dean is also working with operational adviser Alvarez & Marsal, according to people with knowledge of the situation, who asked not to be named discussing a private matter. Lawyers who specialize in restructuring negotiations have also held preliminary discussions with Dean’s debtholders in attempts to organize a formal group for talks with the company, the people said.

Representatives for Dallas-based Dean and at Alvarez & Marsal didn’t respond to requests for comment.

Remote Prospects

Analysts at JPMorgan Chase & Co. and beverage industry executives interviewed by research firm Third Bridge have expressed skepticism that a takeover is imminent. The executives surveyed by Third Bridge cited plant closures that increased Dean’s costs and reduced production volumes.

“Management has expressed interest in a sale, but they are primarily focused on turning around their business, so selling the assets seems secondary to them at the moment,” said Brian Sanders, an analyst at CreditRiskMonitor. “We also haven’t seen any major players express interest.”

Over the years, Dean Foods amassed a collection of small, regional processors whose facilities are now aging. The company has dozens of plants around the country, mostly making milk and ice cream for brands such as Friendly’s and Steve’s. Some of them would be valuable to regional players, like plants in Idaho and Florida, where milk consumption is expanding along with population growth, according to Gould.

But in other regions, the company’s assets are less attractive; some plants in the Midwest might have to shutter as milk demand declines and the industry continues to consolidate, Gould said. In California, some of the real estate could be worth more than the facilities themselves, he said. Dean received and rejected at least a half-dozen offers to buy some plants or an ice-cream business that includes Friendly’s, the Wall Street Journal reported.

More pressure comes from producers of milk with extended shelf life that’s sold in unrefrigerated cardboard cartons. This allows milk to be shipped nationally, forcing Dean to compete against other regions, Gould said. Analysts also cite competition from alternatives derived from rice, almonds and other plants.

Dean reported $887 million of debt as of year-end, including $700 million of senior unsecured bonds due in 2023. In February the company completed a debt refinancing to gain more time and flexibility. It also eliminated its dividend.

Scozzafava has said the company wants to step up its role as a supplier to the private-label business, but that may not ease Dean’s identity problem, Matthew Mason of consulting firm Conway MacKenzie said in an interview.

“They need to find a way to differentiate themselves, whether it’s dairy or other types of products,” Mason said. “When they’re competing for shelf space, what makes the consumer pick Dean’s product?”

There is hope for milk. It’s undervalued, said Tom Bailey, executive director of dairy at Rabobank. People are still drinking it, and there are areas of growth. Sales of Fairlife’s high-protein, ultrafiltered milk products have soared, as has Lactaid; the problem is that Dean doesn’t have a similar product, and its current financial squeeze makes it tough to reinvest in research and development, Bailey said.

It’s just a matter of time before the right product mix comes back, “and we see a recalibration of the value of milk,” Bailey said. “We’re waiting for a new milk, and what’s in decline is the old version.”

--With assistance from Eliza Ronalds-Hannon.

To contact the reporters on this story: Lydia Mulvany in Chicago at lmulvany2@bloomberg.net;Katherine Doherty in New York at kdoherty23@bloomberg.net

To contact the editors responsible for this story: Rick Green at rgreen18@bloomberg.net, ;James Attwood at jattwood3@bloomberg.net, Boris Korby

©2019 Bloomberg L.P.