Dealmakers See Slower 2019 as Stocks, Politics Drag on M&A

With 10 days left of 2018, the fourth quarter -- traditionally the strongest in a year -- is on track to be the worst since 2013.

(Bloomberg) -- Dealmakers are bracing for a slower 2019, predicting that stormy equity markets, intensifying political uncertainty and weakening economic conditions could cool a five-year boom in transactions.

With 10 days left of 2018, the fourth quarter -- traditionally the strongest in a year -- is on track to be the worst since 2013, with just $776.7 billion of deals announced, according to data compiled by Bloomberg. The euphoria over U.S. tax reform that drove many companies to do deals earlier in the year gave way to nervousness about a rise in protectionist policies and worsening conditions in the credit markets in the second half, when volumes fell 20 percent.

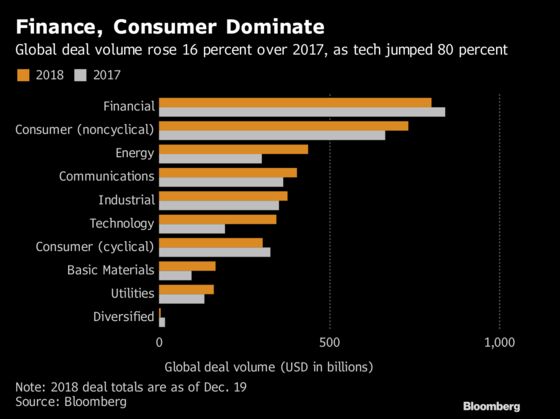

Still, companies around the world struck $3.7 trillion of transactions through Dec. 19, the data show, making it the third-biggest year on record, behind 2007 and 2015. Bankers remain optimistic that technological disruption, the quest for earnings growth and companies’ need to keep simplifying their businesses will fuel deal activity in 2019, albeit at a lower volume than this year.

Nielsen Holdings Plc, Papa John’s International Inc. and Mellanox Technologies Ltd. were pegged as the most likely takeover candidates in the U.S. next year in a Bloomberg News survey of traders that focus on mergers, analysts and fund managers.

So what’s keeping dealmakers up at night?

“There are two areas where it’s fair to be concerned -- continued market volatility and continued regulatory uncertainty could affect M&A levels,” said Robert Kindler, global head of mergers and acquisitions at Morgan Stanley, which closed more transactions than any other U.S bank this year.

The benchmark S&P 500 has lost almost 15 percent since September and is hovering near the first bear market in a decade. Makan Delrahim, the head of the U.S. Justice Department’s antitrust division, acknowledged this year that significant mergers are taking longer to review, requiring an average of 10.8 months to resolve in 2017, up from 7.1 months in 2013. Delrahim has vowed to resolve investigations within six months.

“Volatility in the equity markets is probably the biggest factor that’s put the brakes on a bit,” said Dusty Philip, co-head of global M&A at Goldman Sachs Group Inc. “What we’ve seen is a lot of companies decide to push transactions to next year.’’

Antitrust holdups aren’t just a concern in the U.S. “There remains a nervousness about the very large deals, which tend to involve regulatory approvals from multiple countries,” said Chris Ventresca, global co-head of M&A at JPMorgan Chase & Co.

The machinations of Brexit are top of mind for many dealmakers concerned that the second-biggest M&A market in the world could be affected by what kind of a deal the U.K. eventually strikes with the European Union.

“An adverse outcome from the current Brexit negotiations could negatively impact M&A activity in 2019,” said Gary Posternack, global head of M&A at Barclays Bank Plc. “A slowing European economy or even continued uncertainty about the future UK/EU relationship could have ripple effects globally,” he said.

As British Prime Minister Theresa May wrangled with her government over a Brexit package this month, dealmaking volumes in the U.K. dropped to just $7.7 billion -- the worst December since 2012.

The concerns aren’t limited to the U.K. “Geopolitical uncertainty is the biggest risk,” said Luca Ferrari, co-head of Europe, Middle East and Africa M&A at Bank of America Corp. The outcome of elections in Italy and Sweden, French President Emmanuel Macron’s declining popularity and German Chancellor Angela Merkel’s diminished position contributed to making the second half the worst since 2007, he said.

The state of the financing markets is another factor that could weigh on dealmaking next year. While interest rates remain at historic low levels, levered deals that rely on loan investors for funding could be hurt by the recent declines in loans and high-yield bond markets. Morgan Stanley’s Kindler said he’s expecting a downturn in private equity and go-private transactions next year because of “disruption in the high-yield market”.

Investors soured on risky corporate loans toward the end of the year amid a more dovish stance on rake hikes from the Federal Reserve and concerns about global growth. That has driven leveraged loan prices down to levels not seen in more than two years and is forcing banks to keep some of the unwanted debt on their balance sheets.

On the other hand, private equity companies have more cash on hand than ever before and are ready to take advantage as prices fall with the declining markets.

“We are talking to select clients about take-private’s that have been off the table for years,” said JPMorgan’s Ventresca. “But with multiple compression and the availability of relatively low cost debt, there is an improved chance of executing them in 2019.”

The theme of companies divesting assets to simplify their businesses is expected to be another focus for deals next year, according to Ventresca. JPMorgan’s pipeline of deals is stronger right than it was a year ago, he said.

Technology deal volumes, which jumped more than 80 percent this year to $345.1 billion, are likely to remain strong as companies continue to address technological disruption and boost their technology platforms, dealmakers said. And activists are again expected to be a big driver of M&A.

Most importantly, companies are going to have to do deals to grow earnings, meaning transaction numbers should stay steady even as volumes retreat next year, said Kindler.

“If you look at the broader macro conditions, they’re still accommodative of M&A,” said Larry Hamdan, head of Americas M&A at Barclays. “The economy is expanding, we still have economic growth and interest rates remain low by long-term historical standard.”

--With assistance from David McLaughlin, Davide Scigliuzzo and Sally Bakewell.

To contact the reporters on this story: Nabila Ahmed in New York at nahmed54@bloomberg.net;Ruth David in London at rdavid9@bloomberg.net;Ed Hammond in New York at ehammond12@bloomberg.net

To contact the editors responsible for this story: Elizabeth Fournier at efournier5@bloomberg.net, Michael Hytha

©2018 Bloomberg L.P.