Deal or No Deal? How to Trade the Three Possible Brexit Outcomes

The pound, U.K. stocks and bond yields would all likely plunge if the country leaves the European Union without a deal on Oct. 31.

(Bloomberg) --

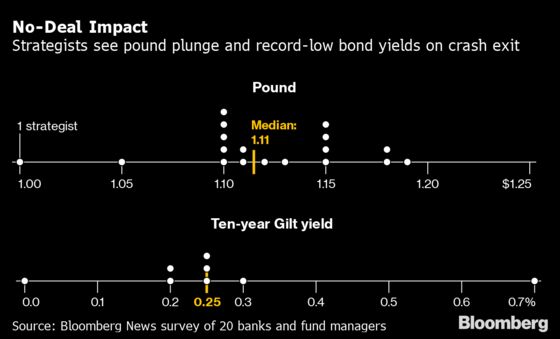

The pound, U.K. stocks and British government bond yields would all likely plunge should the country leave the European Union without a deal on Oct. 31.

Sterling would drop to $1.11 from a current level of around $1.23, according to a Bloomberg News survey of 18 foreign-exchange strategists and investors, while a rush toward the safety of government debt could drive bond yields to record lows. Bloomberg Intelligence forecasts a 13% slide in the fair value of the FTSE 100 index over 12 months in the event of a no-deal Brexit.

“If we know beforehand, then the pound will be selling off in advance and Oct. 31 may not be that big a deal,” Kenneth Broux, a strategist at Societe Generale SA, said in written comments. “If this goes down to the wire on the 30th because of a legal procedure and markets are kept waiting, the one-day or one-week shock will be greater.”

Market participants still don’t see much chance of a no-deal outcome, taking the view that either Parliament or the courts will step in to block Prime Minister Boris Johnson from his vow of delivering Brexit “do or die.” Yet with less than a month until the deadline, the market is left with the possibility of three drastically differing outcomes -- deal, no deal or extension. Here’s a summary of what investors and analysts are saying about them:

No Deal

Should the U.K. leave the EU without a deal, the inverse relationship between the pound and the FTSE 100 index is likely to break down, according to Trevor Greetham, head of multi-asset at Royal London Asset Management. International stocks are seen slumping along with domestically-focused companies and sterling, while the immediate outlook for gilts is unclear.

- Despite its international make-up, the FTSE 100 is still the index most exposed to the U.K. among the key benchmarks tracked by foreign investors, Greetham said in a telephone interview.

- “So if you’re trying to reduce your U.K. exposure as a foreign investor, you would be selling the FTSE at the same time as pulling money out of the pound.”

- A Morgan Stanley simulation forecasts 3%-5% short-term downside for U.K. blue chips in a no-deal divorce.

- The heightened political uncertainty would probably outweigh the positive impact of a weaker currency that enhances the value of overseas earnings.

- The domestic-focused FTSE 250 would drop the most though, taking an 8%-12% hit, economists and strategists including Daniele Antonucci wrote on Sept. 30.

- “A headline like a no-deal Brexit probably does mean that in those first couple of days, there’s a risk-off sentiment globally,” Andrew Millington, head of U.K. equities at Aberdeen Standard Investments, said by phone.

- Even so, with unchanged fundamentals and a central bank that’s likely to be supportive of the economy, stocks would recover over the longer term.

- The “knee-jerk” reaction in the pound to a no-deal would probably see it drop to $1.10-$1.15, said Stephen Gallo, head of European currency strategy at BMO Capital Markets.

- According to Jane Foley, head of currency strategy at Rabobank, such an outcome isn’t priced in to the pound.

- “If we do have a hard Brexit we will see a very strong initial tumble in sterling. Among sterling-based investors, there would be a movement towards gilts and away from equities.”

Deal

According to Goldman Sachs Group Inc., the less-international FTSE 250 index will benefit more than the FTSE 100 if a deal is done, as its members are more exposed to the health of the U.K. economy. The pound would likely make good some of the 6% drop seen against the dollar since the original Brexit deadline of March 29.

- Each percentage point upside move in sterling will translate into a percentage point of outperformance for U.K. domestic stocks versus internationals, Goldman Sachs analysts including Sharon Bell wrote in a Sept. 27 note.

- That suggests a possible 5% gain for domestic shares if a deal is reached, as the pound heads toward $1.30.

- Aberdeen Standard Investments also envisages gains for the FTSE 250, noting that a number of sectors are pricing in a hard Brexit.

- Some bank stocks, for example, are trading below book value, while home-builders too are at depressed valuations, despite the country’s housing shortage.

- ING Groep NV sees a relief rally in sterling to around $1.34 (a 9% gain), according to strategist Petr Krpata. “After a while the focus would turn to the challenges the U.K. would be facing in negotiating the trade deals.”

- According to Commerzbank AG currency strategist Thu Lan Nguyen, the pound’s recovery potential in the case of a deal would be limited to 5-10% due to the fact that the U.K. economy is already weak, and weighed down by soft global growth.

Extension

Another delay to Brexit would undoubtedly be taken better by markets than a no-deal exit, but kicking the can down the road wouldn’t solve the problem. Investors would continue to speculate on the U.K.’s future relationship with the EU, while the prospect of a general election could add to the confusion.

- Any scenario is negative for U.K. stocks, including a delay, which would mean “an extension of uncertainty,” Roland Kaloyan, the head of European equity strategy at Societe Generale SA, said by phone.

- The bank expects an extension to be announced by the end of October, avoiding a no-deal scenario.

- “If we get a deal, then the pound will rise and hurt U.K. exporters. If it’s a no-deal, it’s going to be really bad news for the economy and stocks will also fall.”

- Deutsche Bank AG’s global head of currency research George Saravelos is worried the U.K. market has become too optimistic on a potential Brexit deal being done by the end of October.

- In the event of an extension, “there are plausible and radically different outcomes for the pound.”

- The bank recommends selling sterling versus the dollar.

- But Commerzbank’s Nguyen sees an appreciation of sterling if there’s a Brexit delay, due to relief that a no-deal exit had been avoided.

- “I would however only expect a modest move of around 1%-2% as this is probably the base case for most market participants anyway,” she said.

--With assistance from Ksenia Galouchko, Michael Msika, Jan-Patrick Barnert, Anooja Debnath, Demetrios Pogkas and Michael Hunter.

To contact the reporters on this story: Joe Easton in London at jeaston7@bloomberg.net;Charlotte Ryan in London at cryan147@bloomberg.net

To contact the editors responsible for this story: Beth Mellor at bmellor@bloomberg.net, Paul Jarvis, Paul Dobson

©2019 Bloomberg L.P.