Dave & Buster’s Slow Store Reopening May Portend Earnings Miss

Dave & Buster’s Slow Store Reopening May Portend Earnings Miss

(Bloomberg) -- Dave & Buster’s Entertainment Inc. may fall short of analyst estimates when it reports quarterly results next week as the pace of store reopenings has trailed the company’s projections.

The restaurant chain faces a tougher recovery than peers since its business model is geared toward indoor amusement and group gatherings, two things that have been shunned in the face of the pandemic. As of Friday, its website shows 87 of 137 locations have been reopened in the U.S., Puerto Rico and Canada. On the last earnings call in June, management expected to have about 90 to 95 stores open by the end of July, and all stores opened by September, “barring any delays due to Covid-19 resurgence or changes in state or local guidelines.”

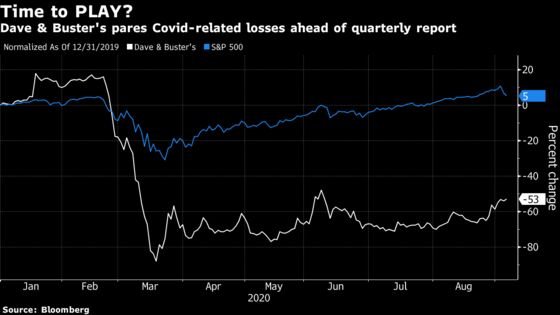

Investors ditched Dave & Buster’s shares as coronavirus took hold in the U.S. in late February, erasing 90% of the company’s market value in a matter of weeks. The tone has shifted more recently with the stock outperforming the broader market since early August. The options market is pricing in a 12% move in the share price following the earnings report on Sept. 10.

“Widespread store closures and disruptions” are likely to result in a shortfall in Dave & Buster’s results, William Blair analyst Sharon Zackfia said in a research note. She expects a comparable sales decline of 82% for the second quarter ended Aug. 2, while Consensus Metrix projects a 75% drop, based on the average of 11 analyst estimates.

Zackfia expects the struggles will continue in the current quarter. Her third-quarter comparable sales estimate of negative 62% is the lowest among analysts surveyed by Consensus Metrix. The average is negative 44%.

Only two of the 12 analysts tracked by Bloomberg have a buy rating on Dave & Buster’s. One of them, Jake Bartlett of Truist Securities, expects investors will look past weakness in the quarterly earnings. “Breakeven guidance and commentary on long-term efficiencies will matter most for the stock,” rather than near-term results, he said in an interview.

Bartlett expects management to reiterate its assertion from June that flat store-level margins could be achieved with a 50% sales decline and a sales drop of 40% could produce breakeven margins for earnings before interest, taxes, depreciation and amortization.

He also sees a positive read-through from Ardent Leisure Group Ltd’s Main Event, which competes with Dave & Buster’s. Last week, Main Event said sales at reopened stores are down just 25% year-over-year in the week ended Aug. 25, compared to an 85% drop for the week ended June 9. Capacity constraints didn’t limit the sales recovery for Main Event, and that’s promising for Dave & Buster’s, Bartlett said.

“What’s more important is what happens in the stores that have reopened,” he said. “The pace of store reopenings is uncertain, but they will reopen. And what we saw from Main Event is encouraging.”

©2020 Bloomberg L.P.