Dash for Cash On as Corporate Titans Draw Down Credit Lines

Dash for Cash Is On as Corporate Titans Draw Down Credit Lines

(Bloomberg) -- Under duress from a viral pandemic and plummeting oil prices, corporate America is facing its most severe test since the 2008 crisis. A swath of the nation’s biggest names is maxing out credit lines, grabbing cash before it can disappear.

Behind the scenes, some CEOs and their finance chiefs are calling bankers this week to ask for liquidity. And throughout the day Wednesday, word leaked out on company after company pulling from existing facilities.

First it was long-embattled Boeing Co. drawing down a $13.8 billion term loan, then it was travel-and-leisure empires Hilton Worldwide Holdings Inc. and Wynn Resorts Ltd. leaning harder on credit facilities totaling more than $2.5 billion. Private-equity titans Blackstone Group Inc. and Carlyle Group Inc. advised some of the businesses they control to consider similar measures to prevent potential shortfalls.

The rush for cash -- while not enough to stress a banking system that’s been holding excess reserves for years -- underscores how quickly sentiment is souring in an economy that seemed healthy until just weeks ago when coronavirus went global, disrupting supply chains and throttling consumer demand. For now, it’s the borrowers on the front line of crises. But inside banks, executives say they’re trying to anticipate which other industries will start pulling next.

“It will be even scarier if companies in other sectors start tapping credit lines,” said Chris Whalen, an investment banker and former debt rater who’s now chairman of Whalen Global Advisors in New York. Already, “these draw-downs show that there’s huge turmoil in a big part of the corporate market.”

CEO Calls

One senior banker said he’s had more calls with chief executive officers than ever before -- and they’re from companies across the entire spectrum. Many are trying to map out how to navigate the current turmoil, he said. On the other hand, some also are seeking opportunities to snap up distressed rivals or exploring the possibility of buying their own stock cheaply.

But across Wall Street, there are clear signs that the tumult, including the abrupt end of an 11-year bull market in stocks, was creating a sudden demand for liquidity. Treasury bonds, typically a haven asset that gains amid market turmoil, slumped as some investors sold them to boost their cash on hand.

Companies are turning to bank loans because their preferred source of cash -- the corporate bond market -- has all but ground to a halt. Investors have been withdrawing money from funds that buy such debt. And even companies that could access the market are being scared away by its wild swings.

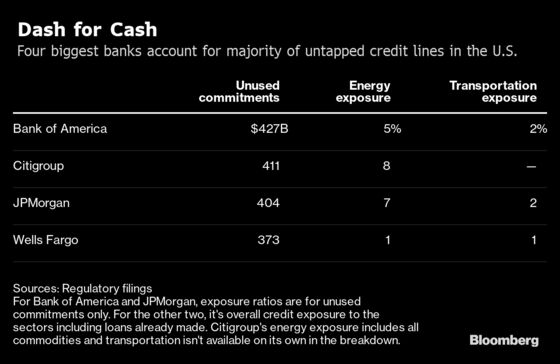

U.S. banks had a total of $2.5 trillion of credit commitments to companies that weren’t used at the end of 2019, according to the latest data from the Federal Deposit Insurance Corp. Regulatory filings show about 64% of those commitments had been made by the nation’s four biggest banks: JPMorgan Chase & Co., Bank of America Corp., Citigroup Inc. and Wells Fargo & Co.

There could be some cash hoarding by U.S. banks anticipating the demand from more clients in coming weeks and months, said Laura Ellen Kodres, a former International Monetary Fund official. But the global financial system is in much better shape than in 2008 and central banks have tools to provide dollar funding overseas if needed, she said.

One place to watch for strain on banks is deposits: Stressed companies may withdraw money, prompting lenders to rely more on other forms of short-term funding, Credit Suisse Group AG analysts Zoltan Pozsar and James Sweeney wrote in a report last week. The Federal Reserve needs to expand funding to the repo market to meet those risks, they said.

Yet the selloff in markets may have the opposite effect, as many investors park their idle cash, said Greg Hertrich, head of U.S. bank strategies at Nomura Securities International. In past routs and panics, banks have been flooded with cash, he said, especially with low interest rates reducing opportunities elsewhere.

“There will be lots more liquidity in the banking world,” Hertrich said.

‘Window Washer’

For now, it wouldn’t be a surprise to see companies accelerating their use of credit lines, according to JMP Securities LLC analyst Devin Ryan. “We’ve seen it before,” he said. Banks are better-positioned than they were a decade ago, but “a stressed backdrop will separate good underwriters from the pack.”

The problem for both banks and their customers is that everyone is in uncharted territory -- a deadly pandemic in a globalized world. So it’s hard to predict how severe the slowdown may get, or how much strain it will put on lending and other financing markets.

“If right now everything stops going down magically, we are OK,” said Jim Bianco, president and founder of Bianco Research and a Bloomberg Opinion contributor. “But we have no idea where we are. No one can model this, no one knows where this will end.”

To those who predict there’s nothing to worry about -- or that companies are overreacting -- he recalled the old joke about the window washer falling from the 10th floor: “When he passes the third floor, he says ‘so far so good.’”

--With assistance from David Papadopoulos, Gillian Tan, Heather Perlberg and Paula Seligson.

To contact the reporters on this story: Sridhar Natarajan in New York at snatarajan15@bloomberg.net;Yalman Onaran in New York at yonaran@bloomberg.net

To contact the editors responsible for this story: Alan Goldstein at agoldstein5@bloomberg.net, Daniel Taub, Steve Dickson

©2020 Bloomberg L.P.