(Bloomberg Opinion) -- Dan Loeb wants to split up Sony Corp. to enhance its value. The company isn’t the only household name in Japanese electronics that might benefit from the treatment.

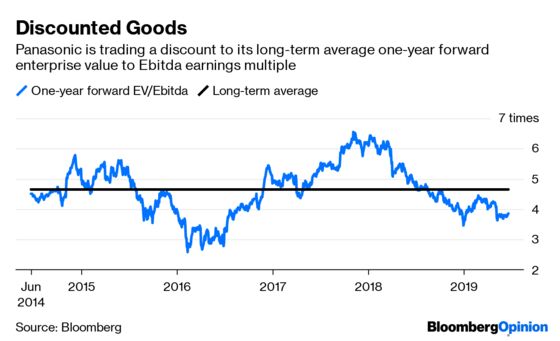

Panasonic Corp. shares have dropped more than 40% over the past 12 months after a partnership with Tesla Inc. disappointed; the company forecast earnings will decline; and a restructuring plan put forward last month failed to convince investors. The firm is trading on a multiple of 3.8 times enterprise value to Ebitda, compared with a five-year average of 4.6 times.

Loeb’s Third Point LLC has called for a spinoff of Sony’s semiconductor business, aiming to reduce the stock’s so-called conglomerate discount – the situation where a company is valued at less than the sum of the different businesses it owns. It’s an analysis that could equally be applied to Panasonic.

Last month, the Osaka-based company released a mid-term plan that will increase its number of divisions to seven from four. Panasonic aims to shift its focus away from the automotive business, which is struggling under the shadow cast by the difficulties in its relationship with Tesla. The electronics maker also announced a series of partnerships and alliances, and estimated restructuring costs of about 90 billion yen ($840 million), according to Goldman Sachs Group Inc.

Analysts say Panasonic still doesn’t have a coherent strategy, and investors clearly want more change. So could a breakup be the solution?

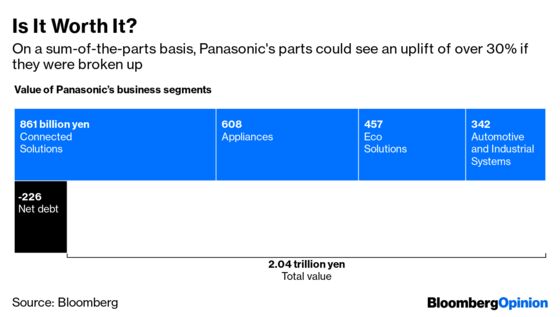

The answer from a sum-of-the-parts analysis is a clear: maybe. If Panasonic listed all its business segments separately and they traded at the mid-point of their peer-group ranges of between 4 times and 9 times enterprise value to Ebitda, then the combined value would be 2% higher than the company’s current market capitalization of about $20 billion. At the high end of the ranges, Panasonic could increase its value by as much as 32%. At the low end, though, there’s a similar amount of downside.

This uncertainty is precisely where a breakup proposal may make sense for Panasonic, though. Pulling apart its various businesses – grouped broadly under appliances, automotive and industrial systems, connected solutions and eco solutions – would enable investors to put their money where they see value and growth prospects, without being encumbered by laggard businesses.

For instance, sales for the connected solutions segment rose 6.9% in the 2019 fiscal year, helped by the Tokyo Olympics in 2020 and growing demand from businesses to help automate tasks. Itochu Techno-Solutions Corp., which competes in a similar business, is trading on a forward price-earnings ratio of 23 times.

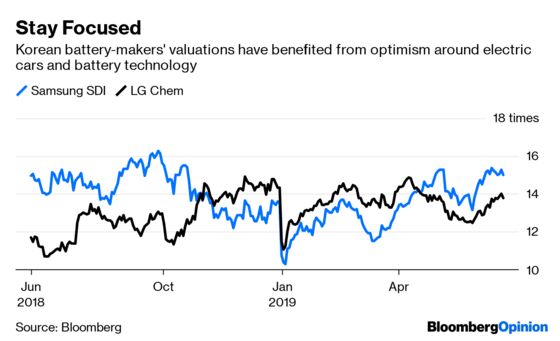

Panasonic thought the automotive business would drive its profitability over the past three years. Even here, running the unit separately could create more value. Panasonic has teamed up with Toyota Motor Corp. and already has partners other than Tesla. With demand for electric cars and the pace of adoption being reassessed, the company could take time to leverage its technology advantage. In the process, the segment’s rising fixed costs won’t weigh down other more profitable businesses. In fact, investors might give a standalone battery business a higher valuation, as they’ve done with South Korean battery-makers Samsung SDI Co. and LG Chem Ltd.

Analysts at Credit Suisse AG downgraded the stock on Friday, noting that they see “no signs of a rebound in earnings in the near term,” and that it was unclear how the company and its profit would look after the restructuring. Earnings at the auto business, where the analysts earlier saw potential for sales growth, is unlikely to improve over the medium term, they said.

There are additional reasons why a breakup should be considered. For one, the government is incentivizing spinoffs with tax breaks. Meanwhile, domestic institutional investors are becoming more activist: The rejection rate for takeover defense measures has risen over the past six years to 80.5% from 40%, according to Goldman Sachs. That’s close to the 85% rate for foreign investors.

Panasonic has some thinking to do. Loeb, meanwhile, might just have a new target.

--With assistance from Elaine He.

Sum-of-the-parts analysis for Panasonic is based on FY2019 operating profit for each segment and used the following assumptions: 1. Average enterprise value to earnings before interest, taxes, depreciation and amortization for peer group of each segment.2. A range of two times above and below average multiple.

Includes exchange-rate effects.

To contact the editor responsible for this story: Matthew Brooker at mbrooker1@bloomberg.net

This column does not necessarily reflect the opinion of the editorial board or Bloomberg LP and its owners.

Anjani Trivedi is a Bloomberg Opinion columnist covering industrial companies in Asia. She previously worked for the Wall Street Journal.

©2019 Bloomberg L.P.